Recently Bajaj Finance announced a hike in its fixed deposit interest rates. This top-notch non-banking financial company (NBFC) announced a 7.6 per cent interest rate on its fixed deposits, thus, allowing its investors to make the most of these fixed-income plans.

The hike in deposit rates comes at a time when the Reserve Bank of India (RBI) announced a 90 basis points rise in repo rates in less than two months, thus, prompting many banks to hike their lending rates. Though deposit rates also went up, the rise was minimal compared to the steep increase in the rates charged on various kinds of loans. This is because banks decide on fixed deposit rates post the consideration of factors including fund requirements, the maturity period of existing loans and the existing interest rates.

As opposed to the 90 basis points increase in the interest rates, banks have raised only 20-40 basis points in the deposit rates. This means that there is more scope for an increase in the fixed deposit and other bank deposit rates. The corporate deposit rate has gone much higher since private lending companies always look for funds to dole out to business houses and retail borrowers. However, short-tenured fixed deposits earn more interest followed by long-term deposits.

With more time left for long-term fixed deposits to catch up to higher interest rates, it makes sense for you to wait instead of allowing your current deposits to roll over with immediate effect. The RBI is likely to hike the repo rates further to tame inflation, which means that investors must wait before deciding to reinvest their deposits.

How to decide on your deposits?

In this rising rate regime, investing in steps instead of all at once will help you gain more. You can start with laddering your fixed deposit investments to gain more through interest. Making a fixed deposit ladder means investing in steps, thus, allowing you to manage your fixed income instruments better. Apart from helping citizens earn more returns from their investments, it also helps to retain enough liquidity that can be used as and when required.

Booking a fixed deposit for a long period at a lower rate could cause a lot of losses on maturity. This explains why you must step up your fixed deposits a year apart, thus, laddering up on your deposits. You can infuse a part of your savings in a one-year deposit followed by booking another part in two-year deposits and then parking the rest of the amount in a three-year deposit. This way, you can book fixed deposits at high-interest rates subject to different tenures as announced by the banks. In case a higher rate is announced by the end of this year, one of your fixed deposits will have matured by then, which you can then reinvest in the higher interest rate.

Corporate deposits

Following the recent announcement by Bajaj Finance and other NBFCs, many people are now looking at various company deposit schemes to invest their money. However, you must look beyond just the interest rates. It is important that you check the company profile, the company ratings, its financial statements and the last five years’ performance.

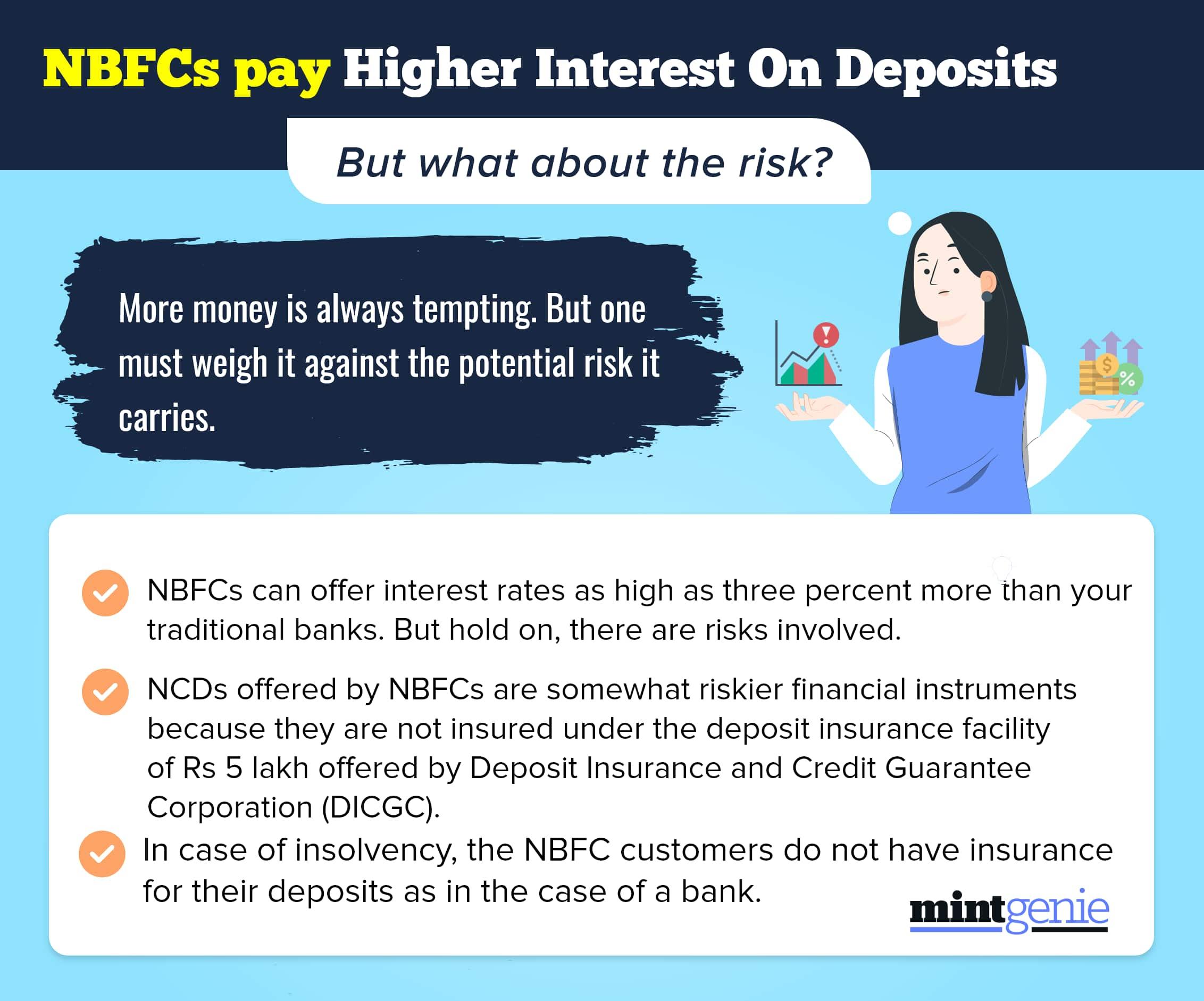

Some companies have started offering high returns on non-convertible debentures (NCDs) that may be highly insecure. The lure of more money has trapped many investors as they are unable to recover their investments if the company defaults or faces liquidation in the future.

Irrespective of the extent of liquidity that NCDs provide, you must be careful before investing in one. How and where you invest your money matters more than just the returns promised.