The year 2022 has been a tough one for the Indian IT sector. The Nifty IT index has lost 27 percent in this calendar year as against a 3 percent rise in benchmarks.

The weak performance of IT stocks this year has been on the back of poor earnings as well as recession concerns. However, global broekrage house Nomura said that it is bullish on select IT stocks.

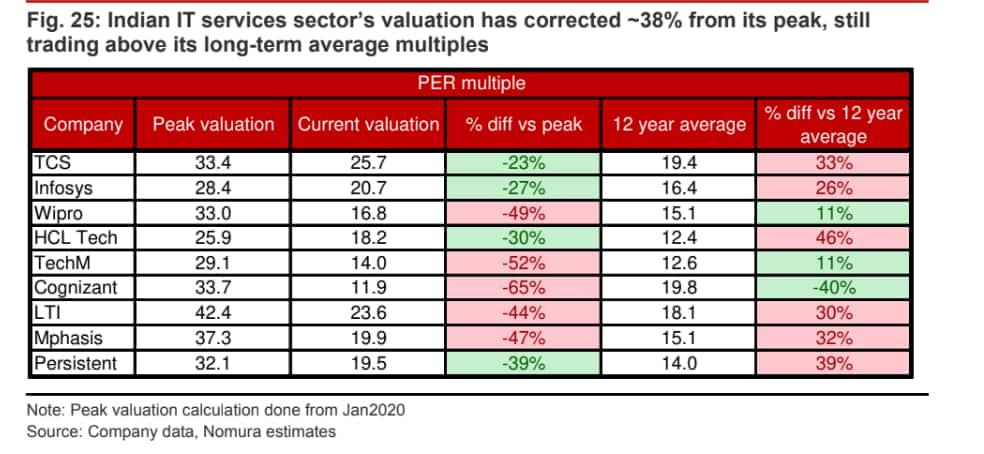

IT sector valuation has moderated significantly and its premium to broader markets has fallen in the past six months, however, it remains elevated when compared with long-term averages, said the brokerage. Going ahead, it believes that there will be a divergence in the operating performance of domestic IT services companies in FY24.

But, it cautioned that while tech adoption continues to rise across industries, we expect a slowdown in the next 12 months compared to the past two years of strong spends.

“Companies with a lower discretionary portfolio (consulting) and exposure to Europe are likely to fare better than the rest. We expect the weakest revenue growth for TCS and the strongest for Infosys in FY24 among large caps,” it noted.

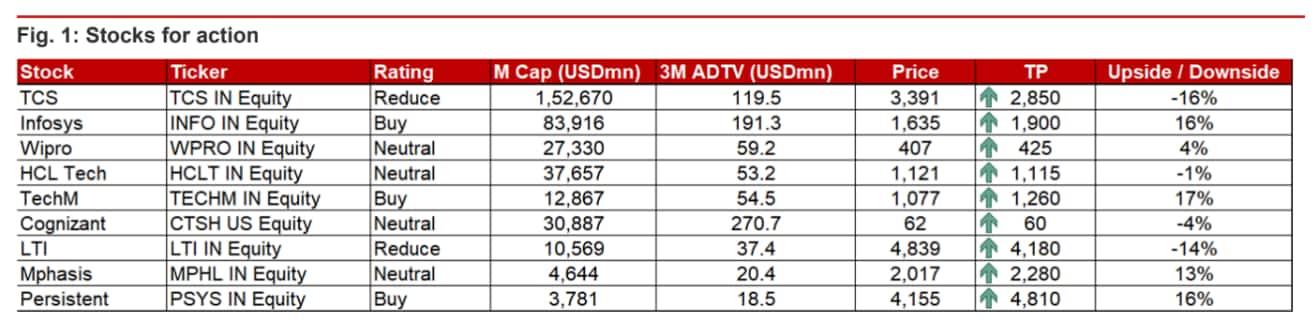

Its top buy picks include Infosys and Persistent Systems whereas its top reduce pick is TCS.

"Our FY24F earnings are higher than consensus estimates for Infosys (Buy) and lower for TCS (Reduce) and Wipro (Neutral) in the large caps space, and higher for Persistent Systems (Buy) in the mid-caps space," it informed.

Revenue growth to be slow, but margins to improve

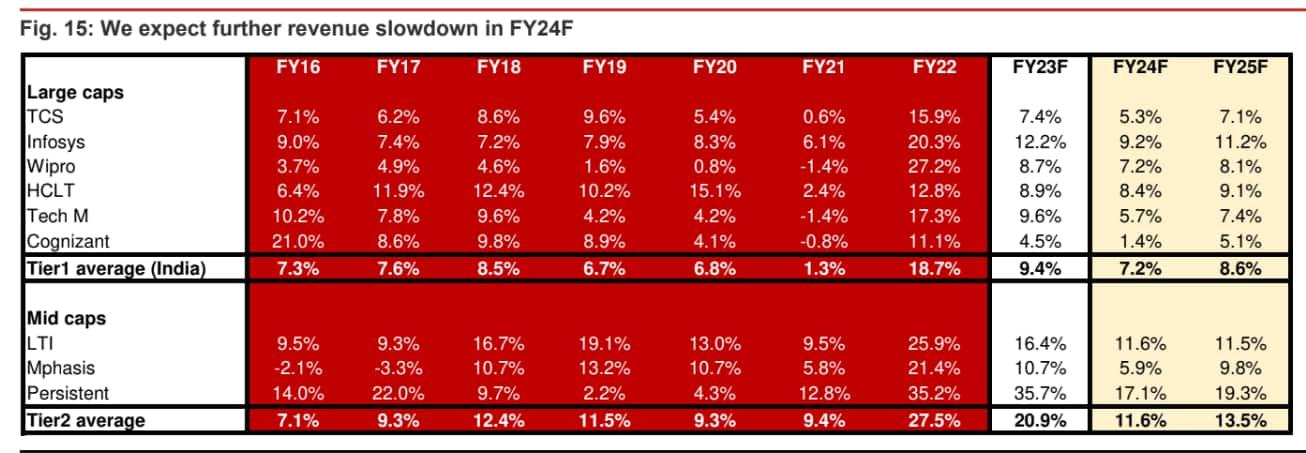

Revenue growth to worsen: The brokerage noted that the CY23E revenue growth outlook for IT companies has continued to worsen since Sept-2022.

"Tech budgets are linked to revenue growth of enterprises, indicating a further slowdown in demand in the coming quarters. In particular, BFSI, manufacturing and technology verticals have seen the most decline in the past three months. For Indian IT services companies, the pain is likely to be more pronounced in interest rate-sensitive sectors like mortgage, capital markets in the BFSI vertical, discretionary retail, and pockets of manufacturing verticals," explained Nomura.

In the very near term, furloughs are likely to weigh on growth for the sector in Q3FY23F, it predicted. Overall, it expects dollar revenue growth to slow down from 12.7 percent in FY23F to 8 percent in FY24F for its coverage universe.

Deal wins to be impacted: The brokerage highlighted that its recent interactions with industry participants including deal advisors suggest a likely impact of the macro slowdown and continued high inflation in the developed markets on the tech budget outlook for most of the industries for 2023.

While cost pressures and changing customer preferences continue to increase tech intensity in enterprises’ businesses and could result in higher offshoring work for Indian IT services in the medium term, IT budgets are likely to be prioritised in areas of automation and cost efficiencies in the near term, it stated.

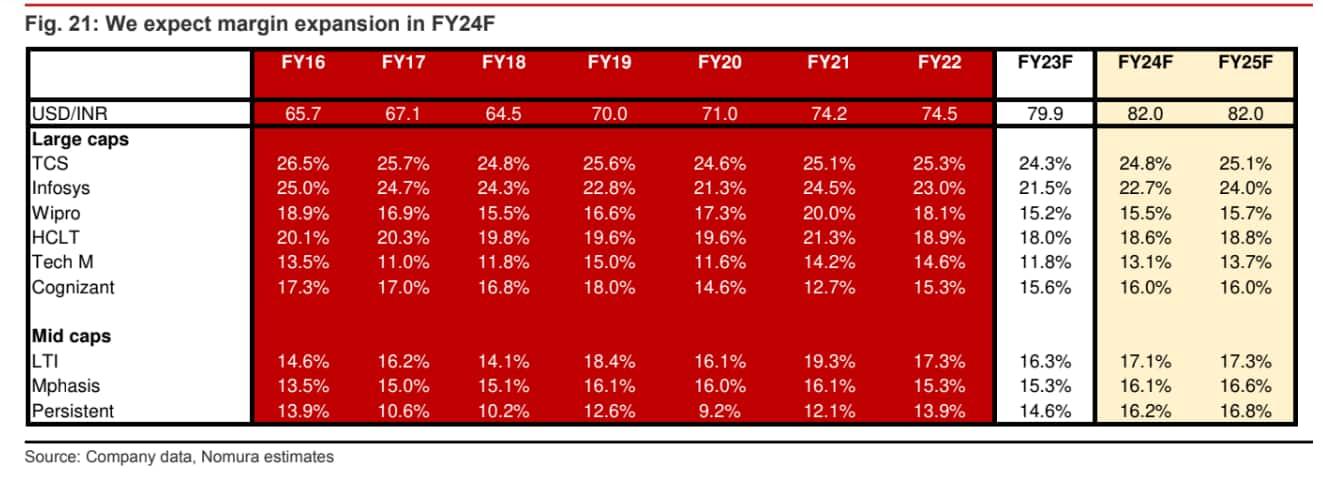

Margin improvement: The brokerage expects an average EBIT margin improvement of 80 bps in FY24F for the stocks under its coverage; the highest 130 bps for Infosys among large caps and 160 bps for Persistent in the mid-cap space.

"Easing supply side issues like softening of attrition are likely to lower the back-filling cost of employees. Improving utilisation, as the recently-hired employees are trained and deployed, would be another tailwind. While price increase is likely to remain positive, we think its pace is likely to slow down in CY23F with more offshoring deals and higher pushback from enterprises given the easing labour market situation and a falling currency," it explained.

Stocks

TCS: The brokerage has maintained a reduce rating on the stock with a target price of ₹2,850, indicating a downside of 12.5 percent. Modest deal wins and high EU exposure to weigh on its revenue growth in FY24F, it said.

Weakening macroeconomic conditions, particularly in the EU, put TCS at a high risk as the region accounts for ~30 percent of its business, it noted. Nomura expects TCS’ yoy revenue growth (in USD terms) to moderate to 5.3 percent in FY24F, from 7.4 percent in FY23F and 15.9 percent in FY22. It also forecasts H1FY23 EBIT margin of 23.6 percent (-200 bps yoy) is likely the trough, as headwinds around salary increments have been taken care of. Key margin levers heading in the near to medium term include improved utilization, lower sub-con costs and moderation of back-filling costs, it added.

Infosys: The brokerage maintains a buy call on the stock and raised its target price to ₹1,900 (from ₹1,650), indicating an upside of 25 percent.

"While Infy’s FY23F growth was front-loaded with 1HFY23F revenue growth at 20 percent yoy in constant currency or cc terms, deal bookings make us confident on the company achieving its guidance of 15-16 percent yoy revenue growth in cc terms in FY23F. Continued participation in deal wins and net new deal wins up 47 percent yoy in 1HFY23F give the company an edge on growth outperformance vs its large-cap peer set," it said.

Nomura expects Infosys to continue to outpace TCS in terms of revenue growth in FY23-24F. It also tweaked FY23-25F EPS by 2-4 percent to factor in our lower revenue and higher margin assumptions, and roll forward our valuation to FY25F (from FY24F). It expects Infy’s EBIT margin to improve by 120 bps yoy to 22.7 percent in FY24F.

Wipro: The brokerage maintains a neutral call on the stock with a target price of ₹425, implying a potential upside of 9 percent.

"While EBIT margins have likely bottomed in 1Q FY23, near term (3Q FY23F), Wipro has the headwind of two-month salary increments and weak seasonality (furloughs), which would likely lead to weak growth and weigh on margin recovery. Improving utilization, lower sub-contracting expenses, selective price increases, continued pyramid optimization (it intends to double fresher hiring in FY23 vs FY22), and flattening attrition is likely the key levers in the near to medium term," Nomura said.

It lowered FY24-25F USD revenue growth by 50-120 bps to 7.2-8.1 percent yoy, leading to 1-5 percent earnings cuts for FY23-25F.

Persistent: The brokerage has a buy call on the stock with a target price of ₹4,810, indicating an upside of 23 percent. Nomura believes Persistent could be one of the few Indian mid-cap IT services companies that could have an improving margin profile y-y in FY23F, and we forecast a 70 bps improvement in EBIT margin to 14.6 percent in FY23F. In the medium term, higher offshoring and continued pyramid optimization could help it improve its margin further in FY24F to 16.2, it added.