Brokerage house B&K Securities has initiated coverage on internet stock Affle India with a buy call. The brokerage has a target price of ₹1,354 for the stock, indicating an upside of 30 percent in 12 months.

The brokerage said that the two-decade-long journey in the space of mobile-first for Affle has culminated in its deep integration with players across the mobile advertising landscape.

"What started over SMS has transformed into real-time targeted advertising across ~2.8 bn devices. Affle stands today at the forefront of mobile performance marketing. Its tech strength enables user conversion assurance. This leads to its key strength – Monetisation only on users taking definite action on an ad, and not on merely clicks or views. This model is known as CPCU, or cost per converted user model. It places Affle in a position of immense leverage over advertisers, as it guarantees KPIs delivery. The competition at large remains devoid of such an offering," explained the report.

Affle (India) Limited, together with its subsidiaries, provides mobile advertisement services through information technology and software development services for mobiles in India and internationally. It operates through Consumer Platform and Enterprise Platform segments. The company provides reselling services of advertisement space for online publishing companies; and customized mobile app development services. It was incorporated in 1994 and is based in Gurugram, India.

Rationale

The brokerage highlighted that Indian internet stocks should focus on two essential characteristics for a behemoth: Cash cow and positive unit economics.

"Affle (India), a consumer tech company in the form of an ad-tech platform satisfies both. Affle has built its presence in multiple layers of the digital ad ecosystem. It had the foresight of the market evolving to mobile-first a decade ago. This spearheaded the development of monetisation via the cost per converted user (CPCU) model, which proved to be a game changer. Execution prowess sustenance notwithstanding changing environment and regulations," the brokerage pointed out.

It further highlighted that mobile-first digital marketing spending is poised to grow the fastest among media channels, adding that a shift in consumption patterns and preference towards targeted advertising are propellers. Affle is further expanding its use cases via its 2V’s (verticalization and vernacular) and 2O’s (operators and OEMs) strategy, which is positive for the firm.

Also, Affle monetises via the CPCU model, where it charges advertisers only on fulfillment of campaign KPIs which allows control on pricing as there is attribution proof. Superior RoI in re-targeting will ensure business longevity as KPIs are even more stringent there, added the brokerage.

What does Affle India do?

Explaining what Affle does, B&K noted that it offers a platform to help businesses acquire, engage and transact with consumers largely via mobile-first digital marketing. The company uses its historic data analysis and insights about consumers, including their preferences, habits and behaviours. This information is used to help businesses target users better. The real MOAT lies in the ability to remain ahead of the curve in data insights and maintaining CPCU rates despite market volatility, it added.

The brokerage informed that Affle had a mobile-first approach ahead of its peers, and this is evident from its mobile monetisation partnerships undertaken way back in 2009. This was followed by a mobile marketing agency and a mobile marketing platform over the next five years. Eventually, Affle began with its own proprietary platform offering the entire palette within the advertising ecosystem.

By 2017, Affle had its own data management and fraud detection platforms. This laid the groundwork to provide mobile-first, targeted advertisements via its own proprietary stack. As the Jio-led digital revolution took over, Affle significantly shored up its capabilities. This was done by a mix of organic investments and inorganic acquisitions, explained B&K.

Further, Affle has undertaken multiple acquisitions over the last five years. It has largely delivered on its committed strategy, both in terms of type of acquirees and the turnaround of the same. The company has walked the talk on multiple acquisitions like Appnext, MediaSmart and JAMPP, informed the brokerage.

"The acquisition strategy has been to take over strategic fits, which offer either new geography or deeper vertical integration. The company should have differentiated tech capabilities but is facing

challenges to break the glass ceiling. Companies in this sweet spot are available at reasonable valuations. These are then turned around to deliver double-digit margins within 24-30 months. Similar prowess was also seen in earlier acquisitions," it noted.

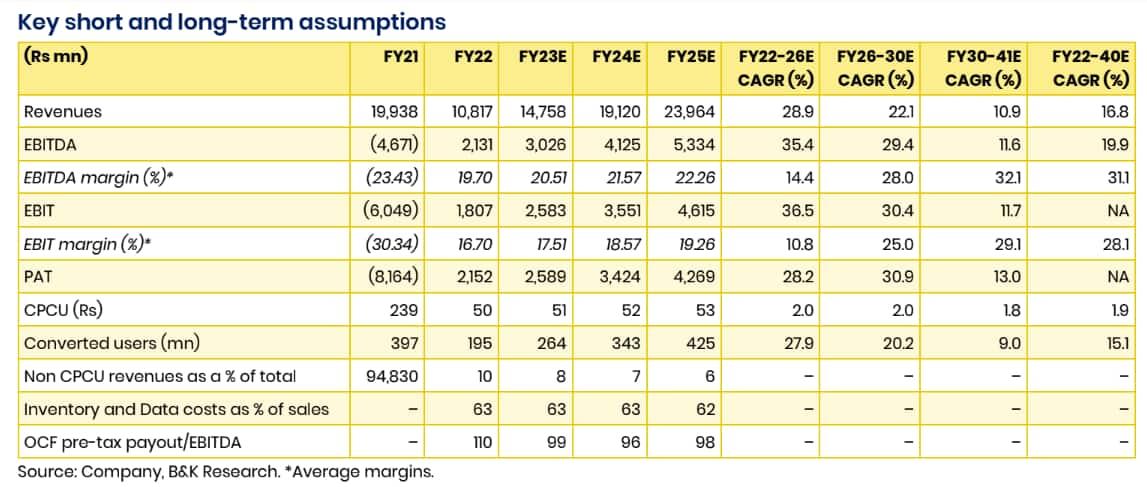

Key assumptions

The company will continue to grow ahead of the growth in overall ad spending buoyed by the market trends and its differentiated offering. The key assumptions by the brokerage are as under:

B&K's FY40E estimates imply Affle market share in India to be only 5.6 percent. This will be even lower for the global market. Affle market share gains are already visible over the past few years as the digital ecosystem has matured, it noted.

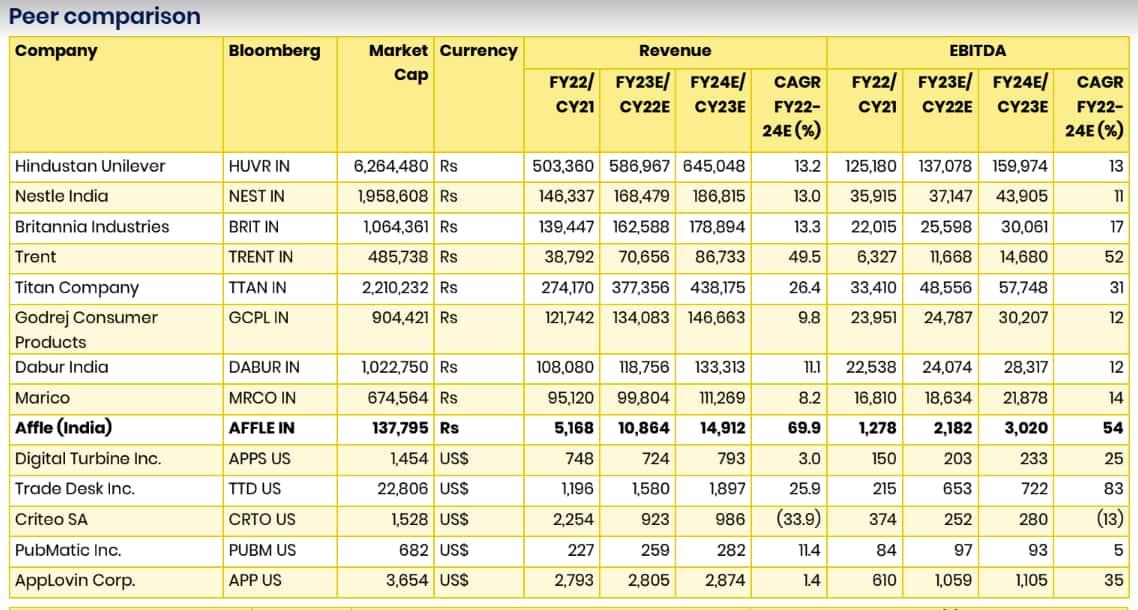

Relative valuation

As per the brokerage, Affle trades at a slight premium to Tradedesk – the global self-serve digital ad delivery behemoth. Amongst the consumer names, Affle trades akin to some behemoths. This is largely a function of higher growth in a consumer-centric space, thus also providing assurance of sustained cash flows. The key risk continues to remain in campaign execution in the wake of evolving regulations, added B&K.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.