Shares of Krishna Institute of Medical Sciences (KIMS) have given robust returns to its investors, rising over 50 percent in less than 2 years. The stock has jumped to ₹1,437, currently from its all-time low of ₹938, hit in June 2021, rallying as much as 53 percent in this period.

Despite this recent rally, domestic brokerage house Nuvama sees more potential in the stock. Acquired assets and gains in the base business drive growth, it said. The brokerage has retained its buy call on the stock with a target price of ₹1,832, implying a potential upside of over 27 percent.

"KIMS posted decent Q3FY23 earnings, led by a healthy performance in the non-COVID business. Sunshine Hospitals, which is still in the integration phase, too posted a decent performance. Its performance is expected to improve with the implementation of other clinical programmes besides orthopedics. We remain positive on the company based on its healthy expansion plan and anticipated increase in operating beds going forward, better occupancy, and higher operating margin with a focus on operational efficiency," explained Nuvama.

While the brokerage cut its FY23 estimates for the stock, it has maintained its FY24 earnings estimates.

"We have cut our FY23 earnings estimate by 19 percent as its Q3 earnings fell short of our expectations due to lower-than-expected occupancy at the consolidated level. However, we retain our FY24 earnings estimate," said the brokerage.

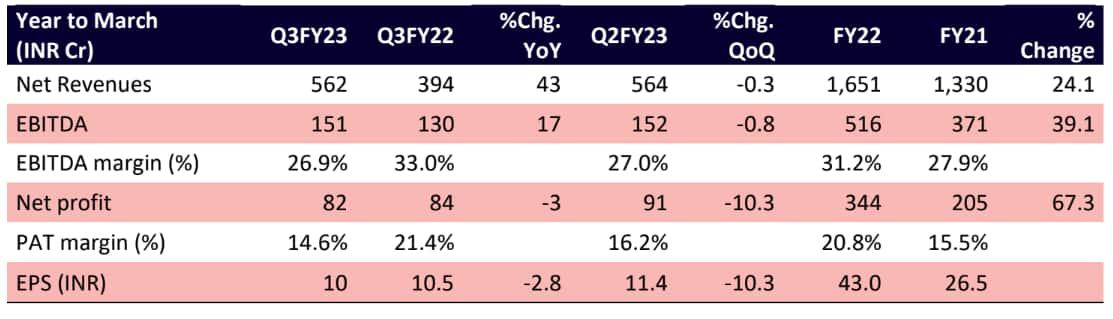

Q3 Earnings

In the December quarter, KIMS reported a 3 percent YoY and 10 percent QoQ decline in its net profit at ₹84 crore on account of an increase in tax expenses and a contraction in EBITDA margin. However, its consolidated revenue advanced 43 percent YoY to ₹562 crore but was down marginally on a QoQ basis. The YoY growth in revenue was on the back of a rise in outpatient (OP)/inpatient (IP) volumes, average revenue per operating bed (ARPOB) in the base business, and the contribution of Kingsway Hospitals, Nagpur.

Its EBITDA rose 16 percent YoY, but fell 1 percent QoQ, to ₹151 crore whereas its EBITDA margin contracted by 610 bps YoY and 15 bps QoQ to 26.9 percent (est. 27.4 percent). ARPOB grew 28 percent YoY and 2 percent QoQ to ₹29,182.

Stock price trend

The stock has risen nearly 10 percent in the last 1 year but is down 7.5 percent in 2023 YTD. It has fallen 5 percent in Feb so far after a 2.5 percent decline in Jan.

From its 52-week high of ₹1,669, hit in November 2022, the stock has shed 14 percent.

Investment Rationale

Strong growth in the base business and acquired assets drive YoY growth: The brokerage noted that the consolidated revenue of the firm, which grew 43 percent YoY to ₹562 crore in Q3FY23, included ₹103 crore from Sunshine Hospitals and ₹37.2 crore from Kingsway Hospitals. The later became a subsidiary in Q2FY23 after KIMS raised its stake to 51 percent with effect from September 1, 2022. Excluding the acquired assets, revenue grew 34 percent YoY, noted Nuvama. However, the occupancy rate fell to 68.2 percent in Q3FY23 versus 82.2 percent in Q3FY22 due to: i) the closure of its Karim Nagar facility, ii) consolidation of Sunshine Hospitals (occupancy: 36.3 percent), and iii) the QoQ impact of the festive season on occupancy, it highlighted.

Nuvama expects a rise in revenue with a ramp-up in occupancy levels at Sunshine Hospitals and Kingsway Hospitals. Revenue contribution from patients paying in cash fell to 55 percent (from 61 percent in Q3FY22), but rose to 25 percent (from 21 percent in Q3FY22) from patients insured, it added.

EBIDTA remains flattish QoQ: Consolidated EBITDA grew 16 percent YoY but fell 1 percent QoQ. EBITDA margin contracted by 610 bps YoY in Q3FY23. It remained flat QoQ at 26.9 percent due to the lower operating efficiency of Kingsway Hospitals, noted Nuvama. Excluding Sunshine Hospitals and Kingsway Hospitals, KIMS reported a 34 bps QoQ expansion in adjusted EBITDA margin to 30.3 percent, said the brokerage. It may see a marginal increase in operating cost in Q4FY23 due to the shifting of a unit of Sunshine Hospitals, Secunderabad to a new building, it forecasted. With the reorganisation and ramp-up of Sunshine Hospitals and Kingsway Hospitals, consolidated EBITDA margin should remain in the 26–27 percent range over FY23–24, predicted the brokerage.

Capacity expansion on track: As per the brokerage, KIMS is expected to incur an annual capex of ₹350–400 crore over the next two-to-three years on various brownfield and greenfield capacity expansions. It is planning a brownfield expansion of around 700 beds over the next three-to-four years and a greenfield expansion of 1,000 beds (excluding the 350–400 bed expansion plan at Chennai which has been put on hold), informed Nuvama. This should expand its total bed capacity by 42 percent over the next three-to-four years. A calibrated capex will be managed via internal accruals, with minimal dependence on debt, noted the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.