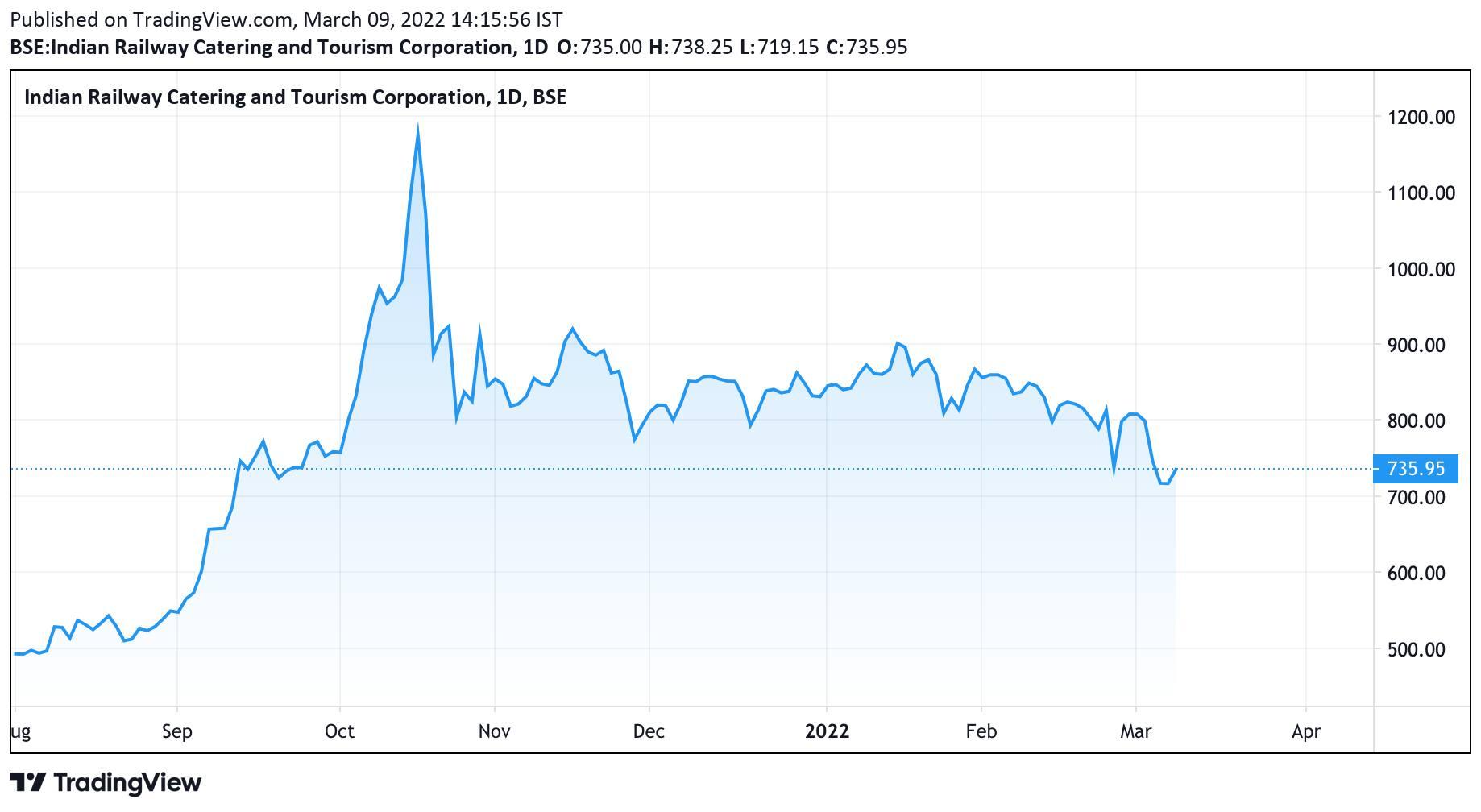

After a bumper listing of over 100 percent and a subsequent 98 percent rally, Indian Railway Catering and Tourism Corporation (IRCTC) seems to have lost its sheen. Amid the recent market weakness, the stock has fallen 78 percent from its 52-week high of ₹1,279, hit in October last year. In comparison, the benchmark Nifty has lost 14 percent from its 52-week high.

The stock, which currently trades around ₹718, has lost around 7 percent in February and 10 percent just in the six sessions of March. In 2022, year-to-date (YTD), it is down 15 percent.

The sharp decline in March comes on the back of the announcement that the Indian Railways have now decided to normalize the Second Seating class (2S) accommodations in all trains back to an unreserved category like in the pre-pandemic period. This announcement is a significant negative for IRCTC as at present 2S class accounts for nearly 38.6 percent (4.8 crore per quarter) of tickets booked in the December quarter of FY22 (Q3FY22).

Market analysts believe that this announcement will lead to further de-rating in the stock. Domestic brokerage house Dolat Research downgraded the stock to 'sell' post this announcement and has a current 12-month target of ₹600, indicating a further 16 percent downside in the stock.

“This event would impact the ticketing segment revenues by nearly 14 percent and 20 percent for FY23E and FY24E, respectively. On overall basis the revenues of the company may get impacted by 6 percent/8 percent for FY23/FY24E while the EPS impact is expected to be about 12 percent/15 percent for FY23/FY24E respectively,” noted the brokerage.

It added that this will not only result in the volume impact right away but it also weakens the prospects for potential new revenue opportunities from unreserved ticketing.

“As current stance suggest Indian Railways is in no hurry to uplift the experience of unreserved consumers and thus would mean no near term potential from monetization through convenience fees on large unreserved ticketing pool,” explained Dolat.

An average of five analysts surveyed by MintGenie have a ‘hold’ rating on the stock. Three analysts recommend strong sell while one each recommend hold and buy for the stock.

Meanwhile, in the December quarter, the railway ticketing firm reported a sharp rise in its net profit, up 167 percent YoY on the back of a low base in the year-ago period. Profit in Q3 FY22 came in at ₹208.81 crore as against ₹78.08 crore in the corresponding period last fiscal.

Also, its revenue from operations rose 141 percent to ₹540.21 crore from ₹224.37 crore posted in the same period last fiscal.

"The outbreak of coronavirus pandemic globally and in India is causing significant disturbance and slowdown of economic activity. However, the business activities of the company are going gradually on track in line with the lifting of restrictions as were imposed by the State and Central governments," said IRCTC post its earnings.