The auto sector has been in a recovery mode in the last one year on the back of rising consumer demand, easing of chip-shortage issues, price hikes, more launches and a rise in volumes. It is one of the best-performing sectors in 2023 YTD as well as in the past 1 year. Nifty Auto has risen around 10 percent in 2023 YTD and 26 percent in the last one year.

Ashok Leyland vs M&M: Which auto stock is a better long-term investment?

TL;DR.

The auto sector has been in a recovery mode in the last one year on the back of rising consumer demand, easing of chip-shortage issues, etc. Amid this backdrop, let's analyse, between Ashok Leyland (AL) and Mahindra & Mahindra (M&M), which automaker provides better opportunities for the long term?

Amid this backdrop, let's analyse, between Ashok Leyland (AL) and Mahindra & Mahindra (M&M), which automaker provides better opportunities for the long term?

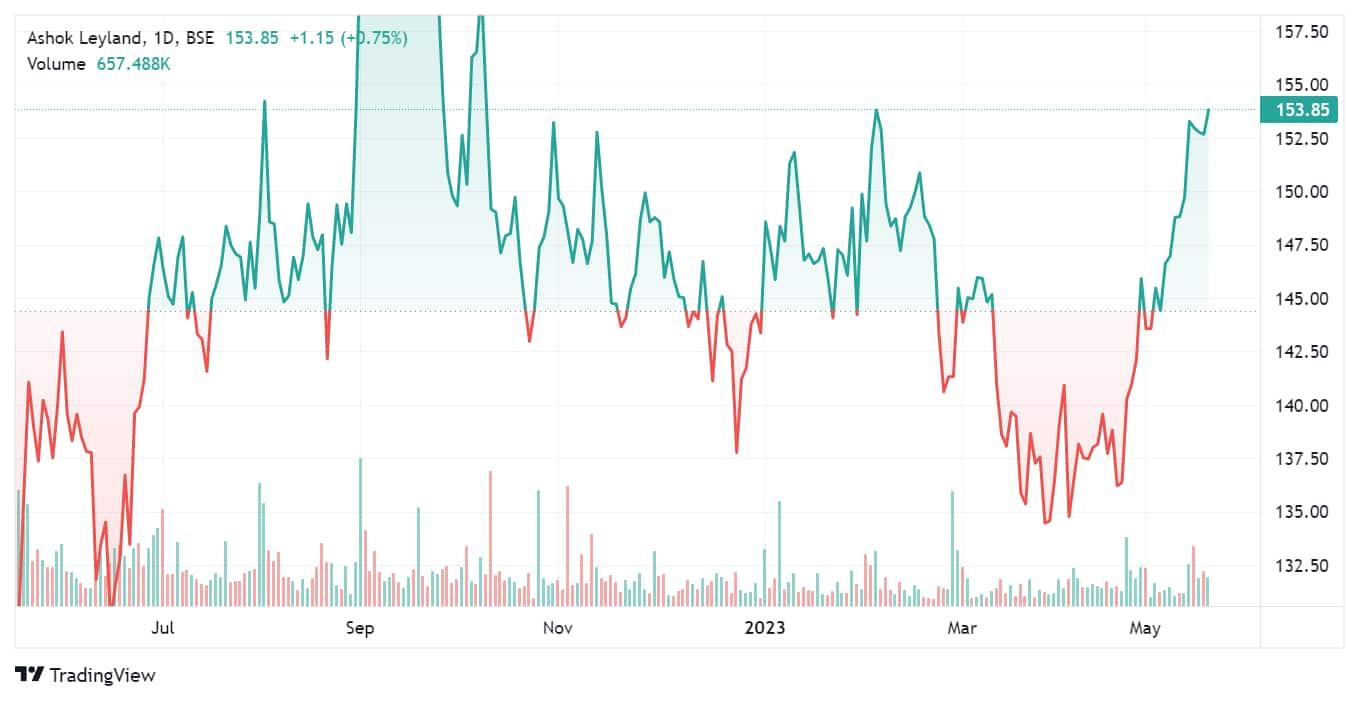

Stock price trend

M&M outperformed Ashok Leyland as well as the market benchmark in the last 1 year. It jumped 39 percent in this period while Ashok Leyland gained around 18 percent. In comparison, Nifty Auto was up 26 percent in the last 1 year.

On the 2023 YTD basis, however, Ashok Leyland is the winner. The stock has advanced over 7 percent whereas M&M is up just around a percent. In the last 1 month as well, Ashok Leyland has risen around 11 percent and M&M has added only 3 percent.

Both these stocks have given positive returns in 3 of the 5 months of the current calendar year.

Ashok Layland has added 5.3 percent in May so far after a 4.8 percent rise in April. But it fell 4.3 percent and 2.7 percent in March and Feb, respectively. It also rose 4.2 percent in Jan.

M&M, on the other hand, is up 2.7 percent in May so far after a 5.8 percent gain in April. It also fell 8.7 percent and 7.9 percent in March and Feb. The stock rose 10.3 percent in Jan.

Meanwhile, in the long term, both these stocks have given multibagger returns. While AL has rallied nearly 255 percent in the past 3 years, M&M has soared 211 percent.

Ashok Leyland stock price trend

About the firms

Ashok Leyland is an Indian multinational automotive manufacturer, headquartered in Chennai. It is owned by the Hinduja Group and was founded in 1948 as Ashok Motors which became Ashok Leyland in the year 1955. It is the second-largest manufacturer of commercial vehicles in India, the third-largest manufacturer of buses in the world, and the tenth-largest manufacturer of trucks.

Meanwhile, M&M is an Indian multinational automotive manufacturing corporation headquartered in Mumbai. It was established in 1945 as Mahindra & Mohammed and was later renamed as Mahindra & Mahindra. Part of the Mahindra Group, M&M is one of the largest vehicle manufacturers by production in India. Its unit Mahindra Tractors is the largest manufacturer of tractors in the world by volume.

Earnings

Both companies have not declared their March quarter results yet.

However, in the December quarter, Ashok Leyland reported a multi-fold jump in its net profit at ₹361 crore aided by robust sales versus ₹6 crore in the year-ago period. Its revenue for the quarter jumped 63 percent to ₹9,030 crore as against ₹5,535 crore in the year-ago period. Ashok Leyland said its domestic Medium and Heavy Commercial Vehicle volume rose to 28,221 units, up 69 percent, over the same period last year. The company's domestic LCV volumes for the third quarter rose to 16,405 units, up 15 percent from 14,233 units a year ago, it added.

"We have been able to achieve growth in market share on a pan-India basis together with significant improvement in net profits. Our team continues to pursue better realisations even as we expand our market share. This, along with our continued focus on optimising input costs, has helped us achieve better financial performance," Ashok Leyland Executive Chairman Dheeraj Hinduja said in a statement.

On the other hand, M&M reported a 13.5 percent rise in its standalone net profit at ₹1,528 crore in Q3 FY2023 versus ₹1,335 crore in the same quarter last year. Its revenue from operations advanced 41 percent to ₹21,654 crore from ₹15,349 crore in the year-ago period. The automaker said that it sold 1,76,094 vehicles in the December quarter, 45 percent higher than the corresponding period last year. The company's tractor sales also rose 14 percent YoY in Q3FY23.

Anish Shah, Managing Director & CEO, M&M Ltd, said, “We have had another robust quarter led by the robust performance of our Auto division. Our farm division also reported healthy growth with increased market share. Our capital allocation actions are continuing to show results and we remain committed to our journey of growth and returns.”

M&M stock price trend

Which is a better stock for the long term?

Vinit Bolinjkar, Head of Research at Ventura Securities, prefers Ashok Leyland over M&M

"We prefer Ashok Leyland as a long-term investment over M&M due to its pure-play CV portfolio and a sizable market share in the domestic CV segment. There is a strong possibility that the upswing in the CV cycle (ongoing for the past two years) could sustain beyond its typical 2-3 years period due to the rising demand from construction, infrastructure, mining and logistics. The recent scrappage policy could further accelerate the volume growth in the coming years. In addition, Ashok Leyland has a formidable presence in the e-mobility (electric bus) domain through its subsidiary Switch Mobility, which has opened a huge opportunity to sell EV buses to state transport departments," he explained.

He further pointed out that, unlike Ashok Leyland, M&M has a presence in various auto segments – PVs, CVs and Tractors. Its PV business is witnessing fierce competition from Hyundai, Maruti Suzuki, Kia, Tata Motors and MG Motors, while its CV business, is dominated by LCVs, where EVs are disrupting the market. Though M&M has a leading market share of 35-40 percent in the tractor market, the Indian tractor market itself is likely to remain flat in FY24 due to a weak rural economy and below-normal monsoon predictions by IMD, Bolinjkar added.

While Saji John, Research analyst at Geojit Financial Services has a positive outlook for both companies due to strong infrastructure-led demand, he believes AL will have an edge over M&M in the medium term.

The expert noted that volume growth in the commercial vehicle space for both AL and M&M was robust in FY23, growing at 49 percent and 41 percent, respectively. Moving forward, M&M's diversified portfolio will aid consistency in volume growth & margins, whereas Ashok Leyland largely depends on cyclical economy demand providing a delta to future growth, he opined.

He further pointed out that in April, CV numbers were softer due to the pre-buying of BS-6 vehicles in March and volume growth is expected to improve in the coming months as inventory is corrected to optimum level. As a result, AL’s profitability should gear up to pre-Covid levels due to better operating leverage & realisation and softening metal prices, he added.

John believes that in the next 2 years, the CV cycle should perform well, given the observed capex, however, moderation is expected compared to recent years. Currently, the stocks are trading below their historical average, factoring in earnings growth for M&M and AL at a CAGR of 17 percent and 34 percent, respectively, over FY23-25E. Therefore, considering differing business models, AL will have an edge in the medium term, he said.

Aditya Welekar, Senior Research Analyst, Axis Securities, has also picked Ashok Leyland among the two.

Ashok Leyland is the beneficiary of the ongoing CV upcycle. Total CV/MHCV/LCV domestic sales grew by 34 percent/49 percent/27 percent YoY in FY23, led by pent-up demand over the low base of FY22, said the expert. He also informed that as per SIAM data, Ashok Leyland's MHCV (goods carrier) market share improved to 32.3 percent in FY23 from 26.8 percent in FY22, and its total CV market share grew by 240 bps YoY to 18.8 percent in FY23. In FY24, the CV cycle may moderate over the strong growth of 34 percent in FY23 and he expects a high single-digit to low double-digit growth in FY24, supported by the government's continuous focus on infrastructure activities ahead of the general election. Furthermore, the scrappage policy, announced in Mar '21, has come under implementation from Apr '23, likely driving the replacement demand for the CV segment and the recent fall in steel prices will be margin accretive for CVs, he added.

Meanwhile, M&M has more levers in its offering and various products than Ashok Leyland, he pointed out. "The company has done well in the PV segment in the last two years due to the success of new products and market share gains. We expect the growth momentum in the PV segment to continue on M&M's SUV strategy and its focus on improving market share and profitability. M&M also has a key focus on EVs. The success of M&M's' Born EV' models will be critical for medium-term growth prospects. It also has a dominant position in LCV which is expected to grow in mid-single digits in FY24 over a strong base of FY23. However, we expect the tractor segment to remain flat in FY24 owing to the high base of the previous year and concerns around El Nino, resulting in a potentially below-normal monsoon," he explained.

Parul Rao, Research Analyst, SAMCO Securities has also chosen Ashok Leyland.

According to Rao, Ashok Leyland is demonstrating an impressive recovery in margins. "As economic activity gathers pace in India, the commercial vehicle segment is holding its ground and Ashok Leyland is well-placed to reap the benefits. Moreover, the export market also holds strong opportunities for the company. The healthy order pipeline for Switch Mobility gives confidence in its electric buses business. A robust product mix, an uptick in volumes, network expansion, improving market share in the MHCV and LCV segments, new product launches, capex spending, and favorable raw material costs will foster the growth of the company ahead," the expert said.

On the contrary, Suman Bannerjee, CIO, Hedonova, prefers M&M over Ashok Leyland.

As per the expert, Ashok Leyland poses greater risk as a long-term investment compared to Mahindra & Mahindra (M&M) due to its high debt levels, weak interest cover, and negative free cash flow. Ashok Leyland has a significant amount of debt and a heavy debt burden, indicated by its net debt and net debt to EBITDA ratio, he added. In contrast, information about M&M's debt is not provided for a direct comparison, noted Bannerjee.

Furthermore, the expert stated that Ashok Leyland's balance sheet reveals potential liquidity risks, as its liabilities exceed its cash reserves and near-term receivables by a significant amount, on the other hand, specific details about M&M's balance sheet are not available, making a direct comparison challenging. He further pointed out that while Ashok Leyland has shown positive growth in its earnings before interest and taxes (EBIT), it has recorded negative free cash flow over the past three years and negative free cash flow increases the risk associated with debt. Meanwhile, the earnings and cash flow situation of M&M is not specified, so a direct comparison cannot be made, he said.

Overall, Ashok Leyland's heavy debt load and negative free cash flow raise concerns about its financial stability and ability to manage its obligations. The potential risks associated with Ashok Leyland's debt situation suggest that M&M may be a relatively safer long-term investment option. However, conducting a thorough analysis and considering additional factors is essential before making any investment decisions, he advised.

Deepak Jasani, Head of Retail Research, HDFC Securities, is also more positive on M&M.

"Within the automobile sector, both these companies cater to a different set of customers. While M&M is largely into tractors, PV and LCV, Ashok Leyland caters to M&HCV customers. They are not directly comparable, but between the two we are more positive on M&M. The company has a strong backlog of 250k units at the end of Q3FY23. It has launched new vehicles and is gaining market share in the UV segment. Even in the tractors segment it has increased its market share from FY22 levels, though the tractor sales outlook for FY24 remains unclear. It has taken focus strides to achieve a strong position in EVs. It will be rolling out its Born Electric vehicles by 2025, which the management believes would be an inflection point for passenger EVs," he said.

How to choose the right stock

First Published: 19 May 2023, 04:39 PM IST

Topics to follow

Related Stories

markets

Apollo Tyres vs CEAT: Which tyre maker should you pick after stellar Q4 earnings?

A Ksheerasagar