It seems that the stock of Zomato may see some more pain in days to come as some of the top market experts think the stock of the new-age tech firm may fall further.

Eminent finance professor and Valuation Guru Aswath Damodaran, who had valued Zomato just ahead of its initial public offering at about ₹41 per share, has now updated the value of the stock to ₹35 per share.

"The value per share has dropped from ₹40.79 to ₹35.32 per share, with much of the value change from last year is coming from macroeconomic developments, manifested in a higher cost of capital. For this value to be generated, the company will need to stop paying lip service to contribution margins and adjusted EBITDA, and work on reducing growth in its cost of goods sold," Damodaran wrote on his blog.

He pointed out that on July 21, 2021, he had valued Zomato just ahead of its initial public offering at about ₹41 per share but the market had a very different view, as the stock premiered at ₹74 per share and soared into the stratosphere, peaking at ₹169 per share in late 2021.

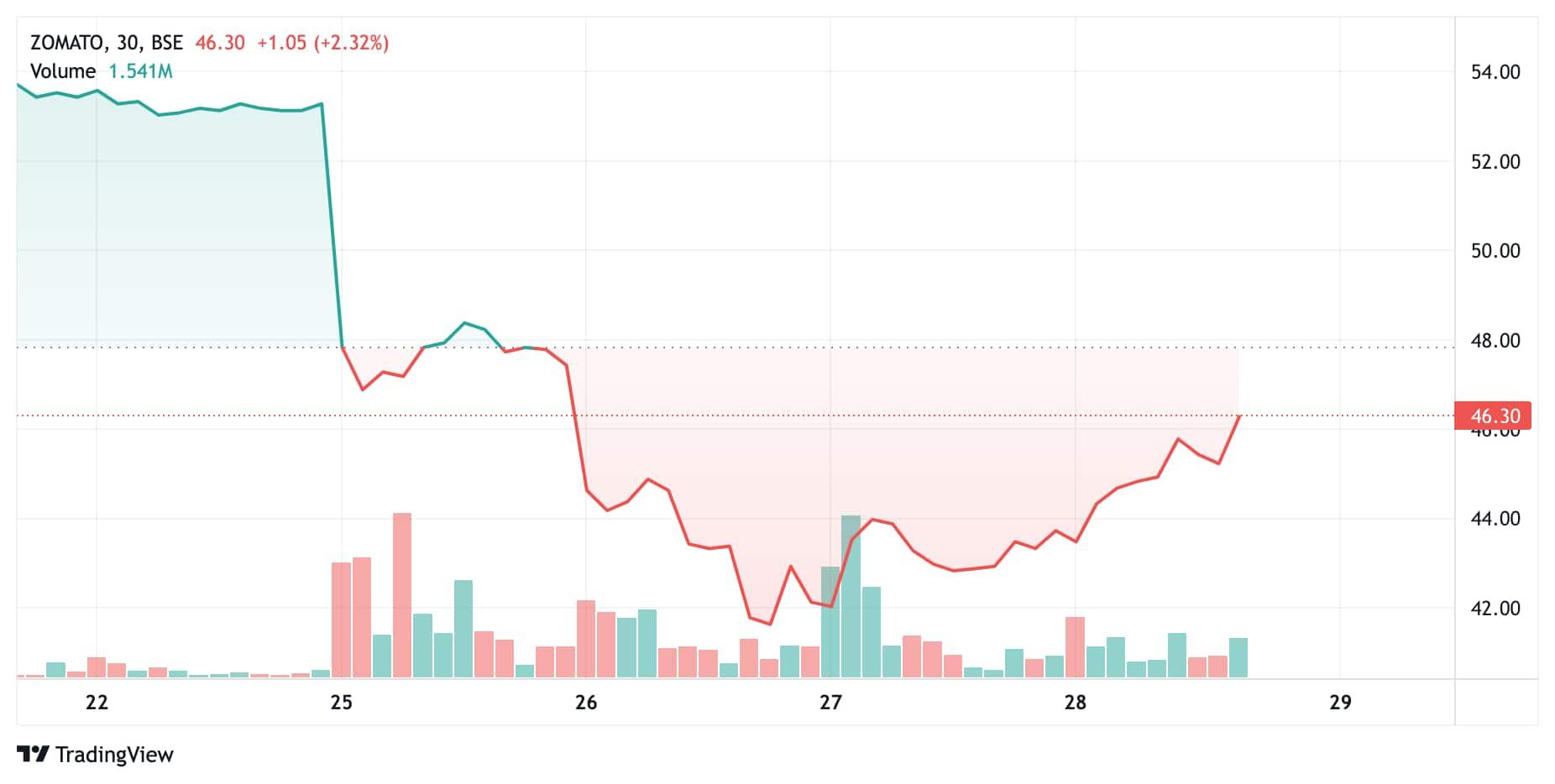

The stock hit an all-time low of ₹40.55 on July 27, 2022.

At the time of Zomato IPO, Damodaran had argued that "investment in Zomato was a joint bet on India (that economic growth would bring more discretionary income to its people), on Indian eating habits (that Indians would eat out at restaurants more than they have in the past) and on the company (that its business model and first move advantages would give it a dominant market share of the food delivery market)."

He said in hindsight, he was both wrong and right.

"Though some have suggested that price dropping to my value is a vindication of my valuation, it seems skewed to celebrate only your successes and not your failures. Even if nothing in my valuation has changed, the value per share of ₹41 per share was as of July 2021, and if it is a fair assessment, the expected intrinsic value per share in July 2022 should be roughly 11.5% higher (i.e., grow at the cost of equity), yielding about ₹46 in July 2022," said Damodaran.

"The company and the market have changed in the year since I last valued it, and to make a fair judgment today, the company will have to be revalued," he added.

He said he valued Zomato in July 2021, the markets (in India and globally) were in the midst of a boom, with an abundant supply of risk capital and optimism about economic growth, pushing up the prices of tech companies, generally, and the youngest, most money-losing tech companies, specifically.

Those circumstances no longer hold, with two big developments in global markets - the return of inflation and the retreat of risk capital.

Disclaimer: The views and recommendations made above are those of the analyst and not of MintGenie.