Brokerage house Nuvama Institutional Equities believes that automobile demand momentum has exhibited good roadholding while gliding over unexpected turns, such as shortages of semiconductors, high prices for raw materials, and clogged supply chains.

The brokerage also thinks that the sector will keep growing because to a number of factors that are driving up volume, including increased replacement demand, new goods, robust business and economic activity, policy push and ample finance availability.

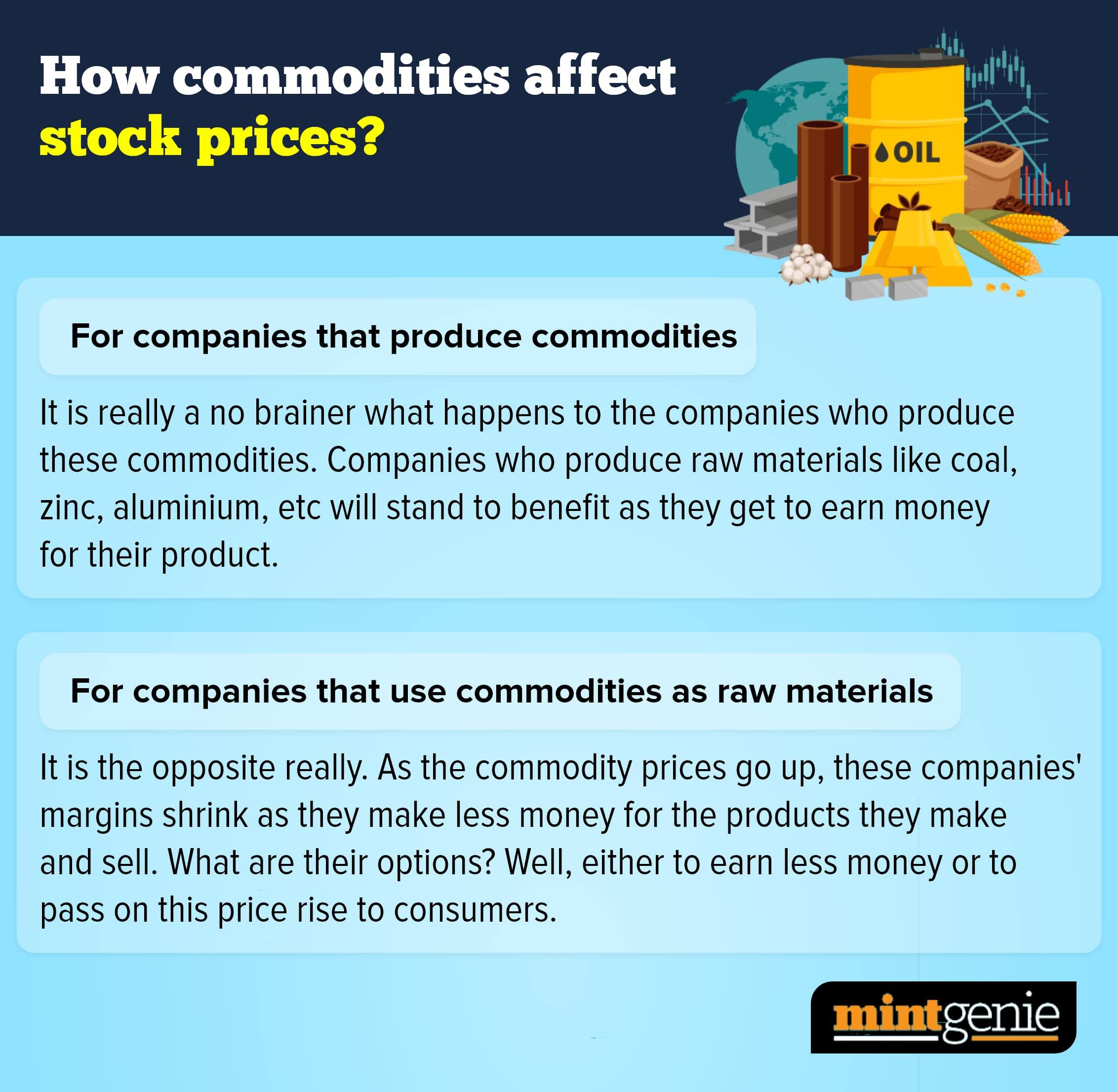

"Rolling resistance for the sector is also low amid falling commodity and metal prices, which shall lift margins and drive double-digit earnings growth in FY24E for companies in our coverage. Electrification is accelerating with incumbent original equipment manufacturer (OEMs)/ ancillaries keenly changing lanes for a smooth transition. We expect FY24E volume growth of 10% for medium and heavy commercial vehicles (MHCVs)/2-wheelers (2Ws) and 6% for passenger vehicles (PVs)," said the brokerage.

Nuvama's preferred picks under its coverage universe are Tata Motors Ltd, Maruti Suzuki India Ltd and Samvardhana Motherson International Ltd. The brokerage firm is bullish about the three stocks and recommended 'buy' rating for them. On the other side, Bharat Forge Ltd is the brokerage's braveheart and it has recommended 'reduce' rating on the stock.

Let's look at the reasons cited by the brokerage for choosing the certain stocks as its top selections and for downgrading the stock.

Tata Motors Ltd

The brokerage's bullish outlook is motivated by expectations of a cyclical upturn in domestic PVs/CVs and at Jaguar Land Rover (JLR); JLR's order book, which would improve the mix in favour of the more profitable Land Rover (LR) brand; a sharpening focus on electric vehicles (EVs) in the domestic business and at JLR; margin expansion coming from growing economies of scale and highly-efficient, cost-cutting measures; and reduced gearing spurred by robust free cash flow (FCF).Over the period of FY23–25E, the brokerage has factored in a revenue/earnings before interest, taxes, depreciation, and amortisation (EBITDA) compound annual growth rate (CAGR) of 12%–27%.

Maruti Suzuki India Ltd

By FY25E, a number of new SUVs would help Maruti Suzuki quickly regain market share, reaching 46%. In the past, despite late entrances, Maruti Suzuki has had a high success rate for its launches and gained sizable market shares in new areas.

"We expect an FY23–25E revenue CAGR of 12% driven by moderate growth in cars and robust growth in SUVs. Meanwhile, focus on emerging powertrains would persist through own efforts and Toyota’s support. All in all, we reckon better net pricing and scale shall boost profitability, driving a PAT CAGR of 25%," said the brokerage.

Samvardhana Motherson International Ltd

Given the company's solid management, the anticipated cyclical rebound in the underlying car categories, and the rising content per vehicle as a result of premiumisation and electrification, the brokerage is optimistic about the company's prospects. Given the company's pending order book and production ramp-up, it is optimistic about Europe and North American PVs and projects a volume CAGR of 6% and 5% for CY22–24E.

"The domestic PV industry is likely to clock a 5% CAGR over FY23–25E. This shall drive a revenue CAGR of 15% over FY23–25E. We also build in a strong EBITDA CAGR of 31% over FY23–25E led by better net pricing and scale," said the brokerage.

Bharat Forge Ltd

The company has established itself as one of the world's biggest players in automotive and industrial forgings, claims the brokerage. The HCV, construction equipment, and oil & gas categories currently face challenges from the weakening European and US economies, which has caused a slowdown in the revenue/EBITDA CAGR to 10%/8% over FY23-25E. Additionally, it produces crankshafts for the US and the Europe (EU), which puts it at risk as we move towards electric and hydrogen-powered engines.