After a robust growth in the last 1 year in the sector, global brokerage house Jefferies, in a recent report, said that it is positive on Indian autos and finds valuations attractive for most stocks, in the context of a strong earnings cycle.

While the Nifty Auto index has advanced 17 percent in the last 1 year, the sector has witnessed some correction the current calendar year. It has risen only 2 percent in 2023 YTD. The index has gained 5 percent in April so far on the back of strong auto sales numbers and a robust growth outlook but has shed around 4 percent each in March and February 2023. It was up 5.6 percent in January.

"We remain positive on Indian autos, with the sector in a positive demand and margin, and hence earnings cycle. Most stocks are trading near or below their respective last 10-year average PE on our FY24 estimates; we find this attractive in the context of a strong earning cycle," said the brokerage.

Jefferies sees a healthy 11-18 percent volume CAGR for passenger vehicles (PVs), two-wheelers (2Ws) and trucks over FY23-25E, with 2W growth outpacing four-wheelers (4Ws). It further noted that strong top-line growth and better margins should fuel double-digit earnings per share (EPS) CAGR for most OEMs (original equipment manufacturers).

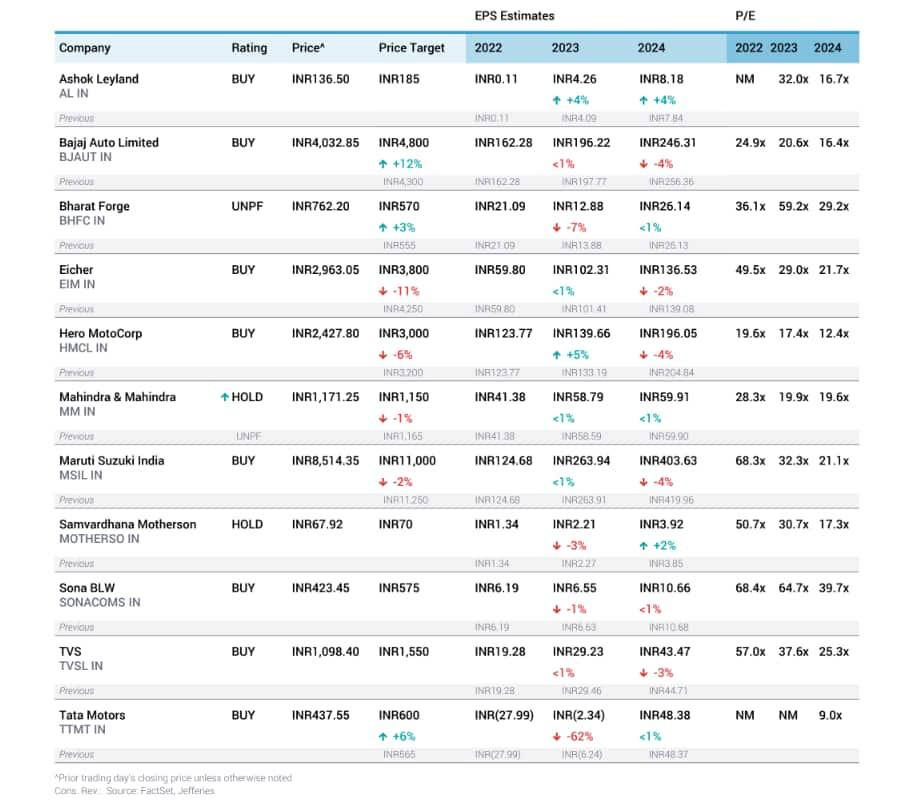

"We have fine-tuned FY24-25E EPS estimates for our coverage within +/-4 percent range," it highlighted.

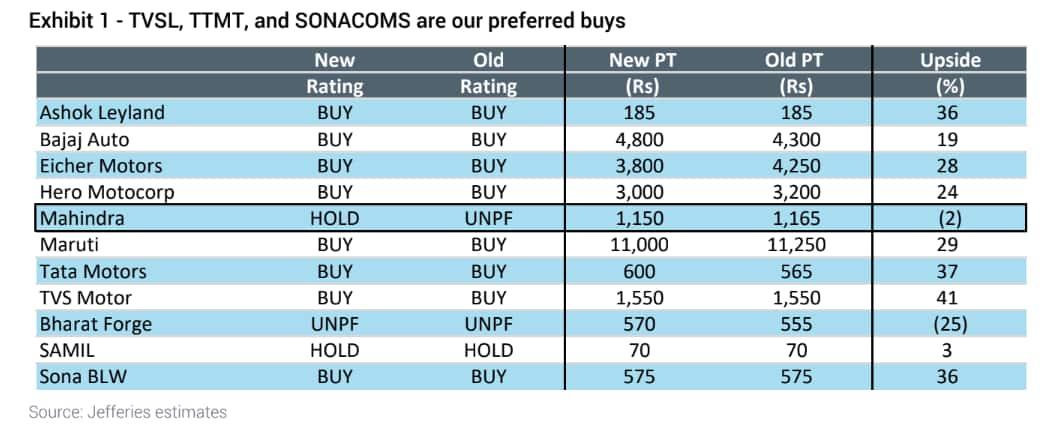

Its preferred ‘buys’ are TVS Motor, Tata Motors and Sona BLW.

"The sharp increase in govt incentives, along with new product launches, has resulted in the share of EVs in 2Ws rising from just 0.4 percent in FY21 to 5 percent in the March quarter; we expect 10 percent by FY25. TVS has risen to the number 2 position in E2Ws (electric two-wheelers) in recent months; with its market share in E2Ws approaching that in internal combustion engine (ICE) scooters, TVS is turning the electrification risk into an opportunity. While EV adoption in PVs is slower (2 percent of the industry in Q4), Tata is leading, with EVs forming 15 percent of its India PV volumes in March, and we believe it will benefit from rising EV adoption," it explained.

It is also positive on Ashok Leyland, Maruti Suzuki, Eicher Motors, Bajaj Auto and Hero Moto Corp.

It has retained an ‘underperform’ call on Bharat Forge, and a ‘hold’ call on Motherson Sumi, while meanwhile upgraded M&M from ‘underperform’ to ‘hold’ post the recent correction in the stock.

"We remain concerned on an imminent downturn in tractors though, which limits us from taking a more positive stance," it cautioned.

2W growth to outpace 4Ws over FY24-25: After suffering its worst downturn in decades, auto demand in India appears poised for continued double-digit growth in FY24-25, said Jefferies. It noted that while 2Ws have lagged in recovery, the abnormal 35 percent fall over FY19-22 created a very favorable base for the segment that is core to personal mobility and it believes 2Ws are ripe for a replacement cycle too.

"We see 2Ws outpacing 4Ws with 18 percent CAGR over FY23-25E (FY23E: +19 percent). While PVs (passenger vehicles) have witnessed some demand moderation in recent months, we see tailwinds from low penetration, aging vehicles-in-use, and reverse shift from shared to personal mobility, driving 11 percent CAGR over FY23-25E (FY23E: +26 percent)," it forecasted.

Trucks, on the other hand, have entered the third year of up-cycle, and the brokerage expects a 12 percent CAGR over FY23-25E (FY23E: +39 percent). Meanwhile, tractors, are at risk of a downturn, and it sees a 15 percent fall in FY24E (FY23E: +12 percent), predicted Jefferies.

Compared to earlier estimates, Jefferies highlighted that it has slightly cut FY24-25E industry volume for PV and 2Ws by up to 3 percent.

Improving margin trajectory: Weak demand and a severe metal price rally weighed on auto OEM margins in the last 2-3 years. Steel (Indian HRC flat) and aluminum prices doubled over mid-2020 to Apr-2022, but then corrected 27-32 percent by Dec-2022, led by weakening China macro and tightening interest rates elsewhere.

"With China showing signs of cyclical recovery, metal prices are likely to have bottomed out; however, we believe the intensity of any potential price increase is unlikely to be similar to 2020-22. We expect 1-4 ppt EBITDA margin expansion for most of our covered auto OEMs over FY23-25E, led by better pricing power amid good demand, and operating leverage benefit," stated the brokerage.

In 2023 YTD, 6 stocks from the Nifty Auto index have delivered positive returns with Tata Motors surging the most, over 19 percent followed by Bajaj Auto, up 18 percent. Meanwhile, Bosch, TVS Sona BLW and Maruti added between 3 and 8 percent in YTD.

However, 9 stocks have been in the red this year so far with Bharat Forge declining the most, down 12 percent followed by Hero Moto, down 9.5 percent. All other auto stocks fell between 3 and 7 percent.