The Nifty Bank index fell 0.62 per cent to 32,845 points on Thursday. The Index has dropped 21.47% from its 52-week high of 41,829.60. In the last month alone, the index has dropped 4.09%. Since the beginning of the year, it has declined approximately 2,636 points, falling to 32,845 from 35,481.

Axis Bank slips nearly a third from 52-week high; Brokerages sees 45% potential upside

TL;DR.

Axis Bank acquired Citibank’s consumer banking businesses in India for ₹12,325 crore. Brokerages have turned bullish on Axis Bank following the transaction, predicting a 40 per cent increase in the private sector lender.

The banking stocks are under pressure due to continued selling from the FPIs. Foreign investors own the largest share of the banking stocks. Fears of a recession, US Fed rate hikes, and commodity inflation all contribute to the significant selling pressure from FPIs.

Meanwhile, shares of Axis Bank have dropped more than 7% in the last one month. The stock is down 14.52 per cent in the last one year. It is down 7.8% year to date.

The stock has fallen 27.10% from its 52-week high of ₹866.90, which it reached on October 25, 2021. In the last week's trading session, the stock hit a new 52-week low of ₹621.2 per share.

Further, foreign investors reduce their stake in the bank from 51.4% in Q2FY22 to 46.9% in Q4FY22, according to data from Geojit BNP Paribas.

Financials

The bank's net profit increased by 50% year on year (YoY) to Rs. 4,417.7 crore, up from Rs. 2,941 crore in the same quarter last year.

Net interest income (NII) increased by 17% year on year to ₹8,819 crore. The net interest margin (NIM) for the quarter came in at 3.49 per cent.

| Consolidated Financials ( ₹in Cr) | Mar-22 | Dec-21 | Sep-21 | Jun-21 |

| Total Revenue | 23,000.7 | 22,091.2 | 20,966.6 | 20,285.4 |

| Operating Expenses | 6,951.6 | 6,631.1 | 6,064.6 | 5,176.9 |

| Operating Profit | 2,094.6 | 2,226.9 | 2,020.4 | 2,757.2 |

| Interest | 9,162.3 | 8,795.3 | 8,597.7 | 8,367.4 |

| Profit Before tax | 5,902.7 | 5,301.4 | 4,541.5 | 3,183.9 |

| Tax | 1,468.7 | 1,328.3 | 1,158.7 | 809.4 |

| Net Profit | 4,417.7 | 3,956.9 | 3,387.7 | 2,356.9 |

| Gross NPA ratio(%) | 2.82% | 3.17% | 3.53% | 3.58% |

| Net NPA Ratio (%) | 0.73% | 0.91% | 1.08% | 1.20% |

Gross non-performing assets (GNPAs) for the quarter fell to 2.82 per cent of total advances, compared with 3.17 per cent in the December quarter and 3.7 per cent in the March quarter last year.

Loan growth for the bank came in at 15 per cent YoY (6 per cent QoQ), with retail loans rising 21 per cent YoY (up 9 per cent QoQ) and SMEs up 26 per cent YoY (up 13 per cent QoQ).

Outlook

Axis Bank acquired Citibank’s consumer banking businesses in India for ₹12,325 crore. According to market experts, the Citi transaction will help Axis since it gives access to 2.6 million Citi cards, which have a greater average expenditure than cards from competing Indian banks.

As per Standard & Poor's (S&P), the acquisition will boost Axis Bank's retail market position and diversify its income profile, which is favourable for the bank's long-term profitability.

Brokerages have turned bullish on Axis Bank following the transaction, predicting a 40 per cent increase in the private sector lender.

Ventura securities said, "Post-acquisition of Citi’s consumer business and a stake in Max Life, the bank is now gearing to scale up its business operations by filling the gap in its portfolio given that most of the asset quality issues are now behind it and its provision coverage ratio (FY22 at > 70%) has already been shored up."

Ventura Securities has a 24-month target price of ₹901.1 on Axis Bank, which hints toward an upside of 44 per cent from its latest close.

However, under more favourable conditions, it predicts FY24 AUM of Rs.9,52,204.9 cr in FY24 (CAGR of 15.1% over FY21-24) and NIM margins of 4.0% (+40bps over FY21) and a target price of ₹1,158.6/share, an upside of 84.98% from current levels. It assigns an FY24 target PB of 2.4x.

While, under the bear case scenario, the brokerage firm expects an FY24 AUM of Rs. 8,40,742.8 cr in FY24 (CAGR of 10.5%) and NIM margins of 3.0% (-58bps over FY21) and a target price of ₹582.9/share, a downside of 7.5% from current levels, it assigns an FY24 target PB of 1.2x.

On the other hand, global brokerage firm Morgan Stanley maintained its "overweight" rating on the back of the lender's robust asset quality, improved balance sheet, and revenue granularity. The brokerage firm has a target price of ₹910 on Axis Bank's shares, an upside of 45 per cent from its current market price.

An average of 42 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

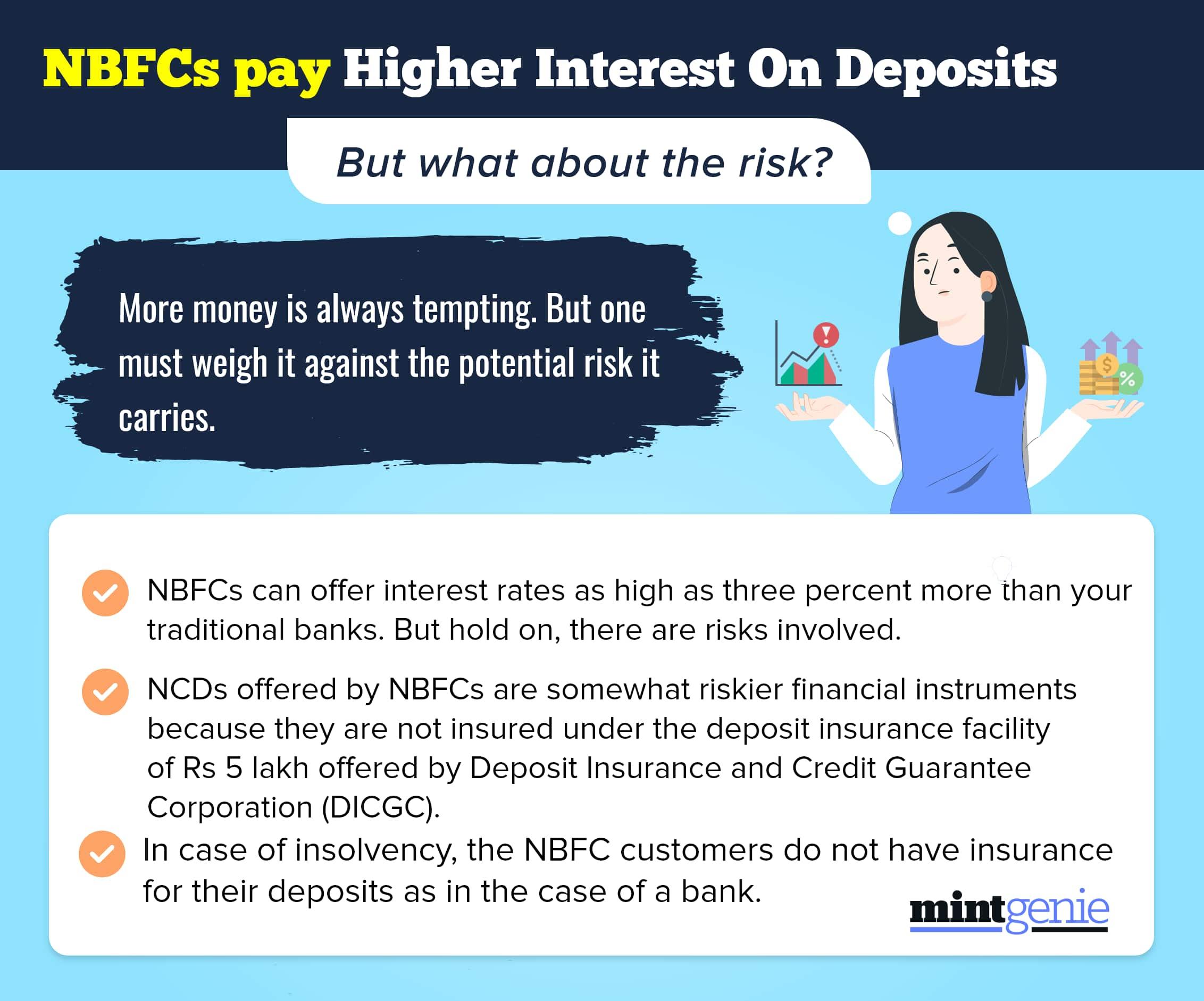

NBFCs pay a higher rate of interest on fixed deposits as compared to regular banks.

First Published: 23 Jun 2022, 03:38 PM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

Looking for an education loan? Here are the best interest rates on education loans

Deepika Chelani