India's one of the top broking firms Axis Securities has turned positive on a mid cap housing finance firm, Aptus Value Housing Finance India, anticipating the company’s bright prospects over the long term.

Axis has initiated coverage on the stock of Aptus Value Housing Finance with a buy call, pegging the target price at ₹400, implying a 24 percent upside from the stock's March 29 closing of ₹322.60.

Why, though?

The company's growth prospects look impressive. It gives home loans to self-employed people belonging to low and middle-income families primarily from semi-urban and rural markets. Aptus operates in niche, less-competitive and under-served markets.

As per Axis, the company has a deep penetration in South India and over the years, it has successfully developed expertise in serving self-employed and new-to-credit customers alongside maintaining robust asset quality.

The brokerage highlighted that deep penetration and a strong customer connection have given the company a pricing power that enables it to generate superior RoAs (return on assets).

"Aptus remains well placed in the high-growth market that exhibits lower competition due to the expertise required to cater to the underserved self-employed customers. The strong operating performance with AUM (assets under management ) growing at 33 percent CAGR (compound annual growth rate) over FY17-21, a larger opportunity facilitating similar growth over the medium term, and best-in-the-industry return profile underpin the company’s premium valuations," said Axis.

"We believe Aptus is well-placed to benefit from the rapidly growing affordable housing market given (a) the under-penetration of the affordable housing finance market, (b) the shortage of housing finance, especially in the economically weaker sections (EWS) and lower-income group (LIG), (c) Deep rural penetration in South India which provides a large addressable market and lower competition; (d) Industry-leading profitability; and (e) Improving asset quality trends."

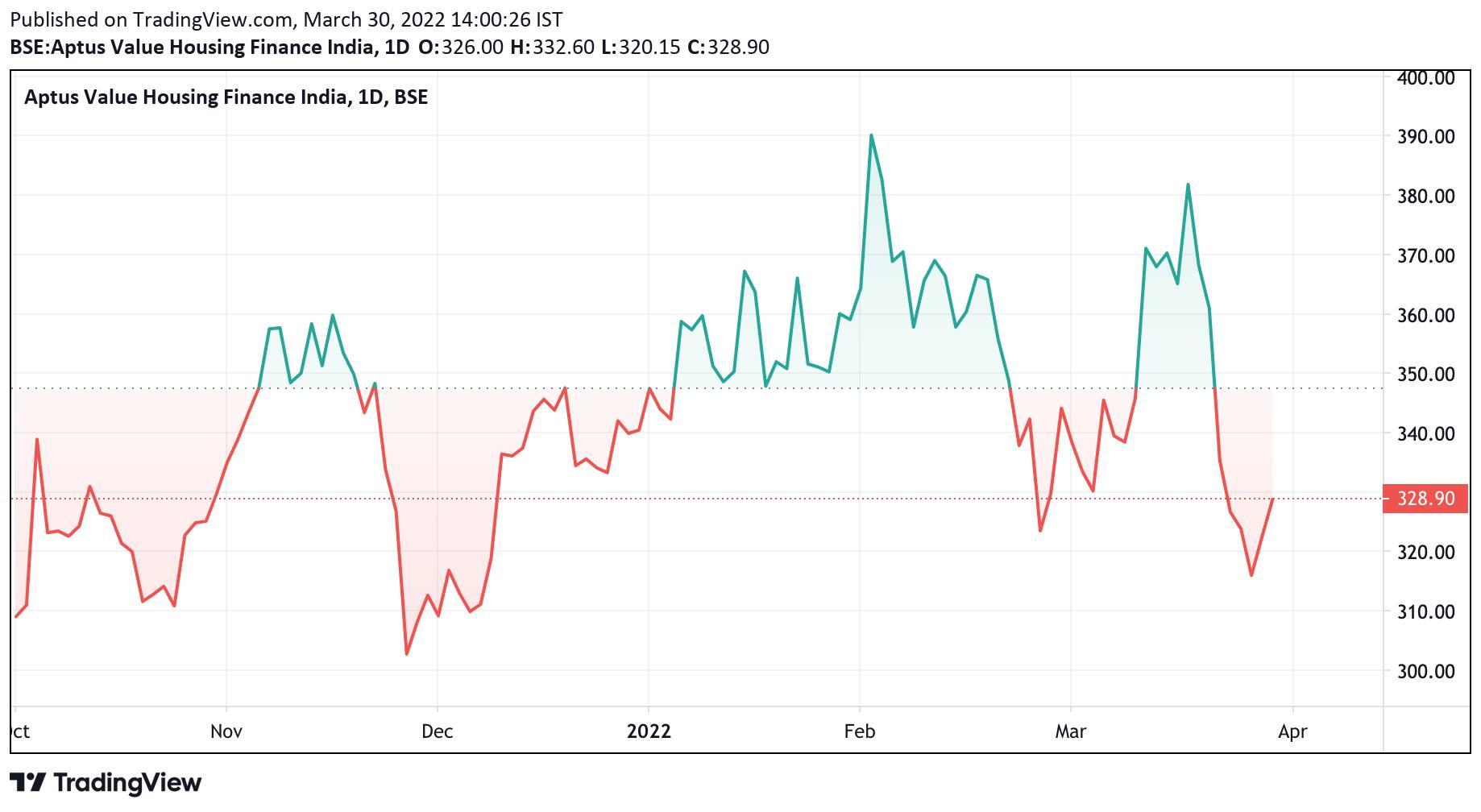

The stock hit a 52-week high of ₹394.95 on February 3, 2022, and has been witnessing selling of late. From the 52-week high, the stock is down 18 percent. It is 5 percent down in the calendar year so far against a half-a-percent loss in the benchmark Sensex.

Clearly, the recent volatility in the market and the concerns over inflation and rate hikes have weighed on the stock. Besides, Axis Securities underscored the company is currently facing near-term headwinds in terms of Covid-led elevated asset quality stress and NIM (net interest margin) compression owing to the rebalancing of the portfolio mix.

However, Axis highlighted that Aptus commands a pricing power, which coupled with its lean cost structure and benign credit cost trends so far have enabled it to report best-in-class RoAs.

"Even as the company shifts its focus from the high-yielding non-home loan book to the core home loan book to comply with regulatory guidelines, subsequent rating upgrades would partially compensate for the yield compression. Easing of asset quality stress would also result in credit costs gravitating to near pre-Covid levels, thereby aiding superior RoAs moving forward. We expect Aptus to continue delivering RoA of more than 6 percent over FY22-24E," said Axis.

Axis believes improving traction in collections, which will result in bucket-wise roll-backs, will help ease the pressure on asset quality in the near term.

"All these factors collectively cement our confidence in the company’s bright prospects over the long term which is reflected in our target multiple of 5.25 times FY24E ABV (adjusted book value).

Adjusted book value measures a company's true value after all assets and liabilities (including off-balance sheet liabilities) are evaluated.

Axis believes the company’s sustained and superior operating performance is paving the way for further rating upgrades.

"Gradually improving asset quality, continued strong operating performance along with the sustainability of superior RoA and RoE (return on equity) would facilitate the re-rating of the stock," said Axis.

Disclaimer: The views and recommendations made above are that of the broking company and not of MintGenie.