Shares of Bajaj Finance rose over 3 percent to ₹6,253.95 apiece in intra-day deals on Thursday after the company declared strong results for the quarter ended March 2023 (Q4FY23). The company reported a 30 percent rise in its consolidated net profit at ₹3,158 crore in Q4FY23 as against ₹2,419 crore in the corresponding quarter of the previous year.

The net interest income (NII) for the quarter under review also advanced 28 percent to ₹7,771 crore from ₹6,061 crore in the year-ago period. Revenue from operations of the financial services firm came in at ₹11,359.59 crore, up 31.68 percent from ₹8,626.06 crore in the year-ago quarter.

Meanwhile, gross NPA (non performing assets) and net NPA came in at 0.94 percent and 0.34 percent, respectively, as against 1.60 percent and 0.68 percent in the year-ago period.

Most brokerages have remained bullish on the stock after it posted in-line results across all parameters.

"Operational parameters continue to progress well and the management remains confident in BAF’s ability to deliver a healthy AUM growth of 25 percent in FY24, aided by improving customer additions, which is expected to grow at 20 percent YoY. The impact of increasing cost of funds will now be visible on margins and the management also expects a 40-50 bps margin compression in FY24. However, lower opex and benign credit costs will partially offset the pressure on NIMs," said Dnyanada Vaidya, Research Analyst - at Axis Securities.

Let's take a look at what various brokerages have to say post its March quarter earnings:

Motilal Oswal: The brokerage has retained its ‘buy’ call on the stock with a target price of ₹7,080, indicating an upside of 17 percent. "Bajaj Finance’s reported PAT grew 31 percent YoY to ₹3,160 crore (inline) in 4QFY23. The good operational performance was driven by 1) a healthy run-rate in customer additions/new loans disbursed, 2) pristine asset quality driving a 7 bps QoQ moderation in credit costs, and 3) moderation in opex ratios," said the brokerage.

It further pointed out that customer acquisition and the new loan trajectory have been strong. The momentum will only get stronger ahead, with the digital ecosystem – app, web platform and full-stack payment offerings – in place, added MOSL. It believes that the firm should be able to offset the NIM compression in FY24 with lower operating cost ratios and credit costs. MOSL's FY24/FY25 estimates have seen a minor increase to factor in the higher AUM growth guidance. It expects the firm to deliver a PAT CAGR of 24 percent over FY23-FY25 and an RoA/RoE of 4.6 percent/24 percent in FY25.

InCred Equities: The brokerage has an ‘add’ call on the stock with a target price of ₹9,000, indicating an upside of 48.6 percent. BAF is a pure-play retail lending franchise equipped with a diversified funding mix and a strong capital base. The stock is currently trading at ~5.5x BV/24x EPS for FY24F (PEG ratio >1), offering an attractive risk-reward ratio, said the brokerage.

"An elevated mortgage portfolio coupled with competitive pricing will keep the margin trajectory for BAF under check, but a gradual easing of excess liquidity can deliver margin surprise. However, we believe improving operating leverage along with low credit cost remains key to profitability.

We are building in 25 percent CAGR in PAT for FY23-26F with best-in-class RoA of 4.5 percent and RoE of 24.5 percent for FY24F/25F," it forecasted.

HDFC Securities: The brokerage has an ‘add’ call on the stock with a target price of ₹6,780, indicating an upside of 12 percent.

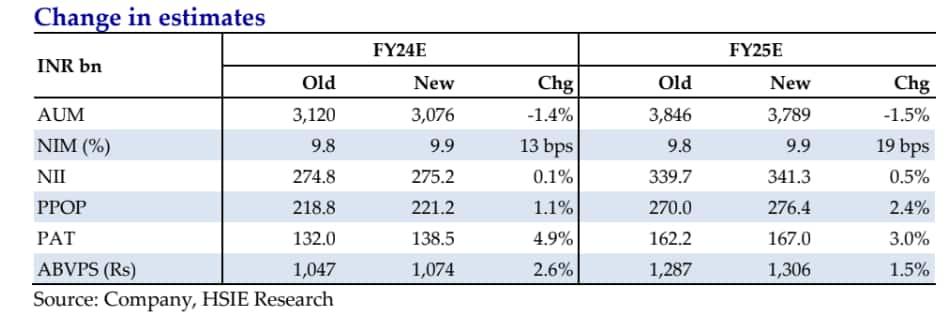

"Bajaj Finance (BAF) delivered yet another strong operating performance with RoA at over 5 percent and earnings growth of 30 percent YoY, despite a rising interest rate environment. Asset quality improved further, credit costs normalised and all businesses were tagged green. With most digital initiatives having already gone live, BAF is poised to deliver steady loan growth consistent with its Long-Range Strategy (LRS) driven by robust customer acquisition, mining of the existing customer franchise and the addition of new loan products. However, increasing scale of operations, concomitant with elevated competitive intensity, is likely to reflect in a slower pace of AUM growth. Further, we are cautious about the quality of earnings from the new-to-franchise (NTF) customers and new businesses. We tweak our FY24/FY25 earnings estimates (+5 percent/+3 percent) to factor in higher-than-expected margins and lower credit costs," it stated.

Sharekhan: The brokerage has reiterated a ‘buy’ on Bajaj Finance with an unchanged price target of ₹7,500, indicating an upside of 24 percent.

The brokerage believes the company is poised to deliver sector-leading ROA/ ROE of 4.7 percent/ 22 percent over FY23-FY25E. It further noted that BAF's diverse product offerings through omnichannel presence along with a focus on new customer addition and ability to cross-sell different products are likely to support AUM growth. Digital transformation and omnichannel strategy are likely to bode well for its growth objectives along with operational efficiencies going ahead and its full impact is yet to be visible, it added.

“The company has exhibited its strong ability to navigate through an economic downcycle, led by a prudent and agile management team and robust risk management framework. The stock offers reasonable risk-reward for long-term investors,” it said.

Kotak Institutional Equities: In a contrarian view, Kotak has retained its ‘reduce’ call on the stock but raised the target price to ₹6,500 (7 percent upside), up from ₹6,150 earlier.

“The current robust demand environment should sustain high growth for Bajaj Finance and other lenders in FY2024E. However, the lagged effect of rate hikes will likely temper margins, which may be partially offset by managing other matrices. The overall business outlook remains strong although rich valuations cap any upside; REDUCE stays with an FV of ₹6,500 (up from ₹6,150)," it said.