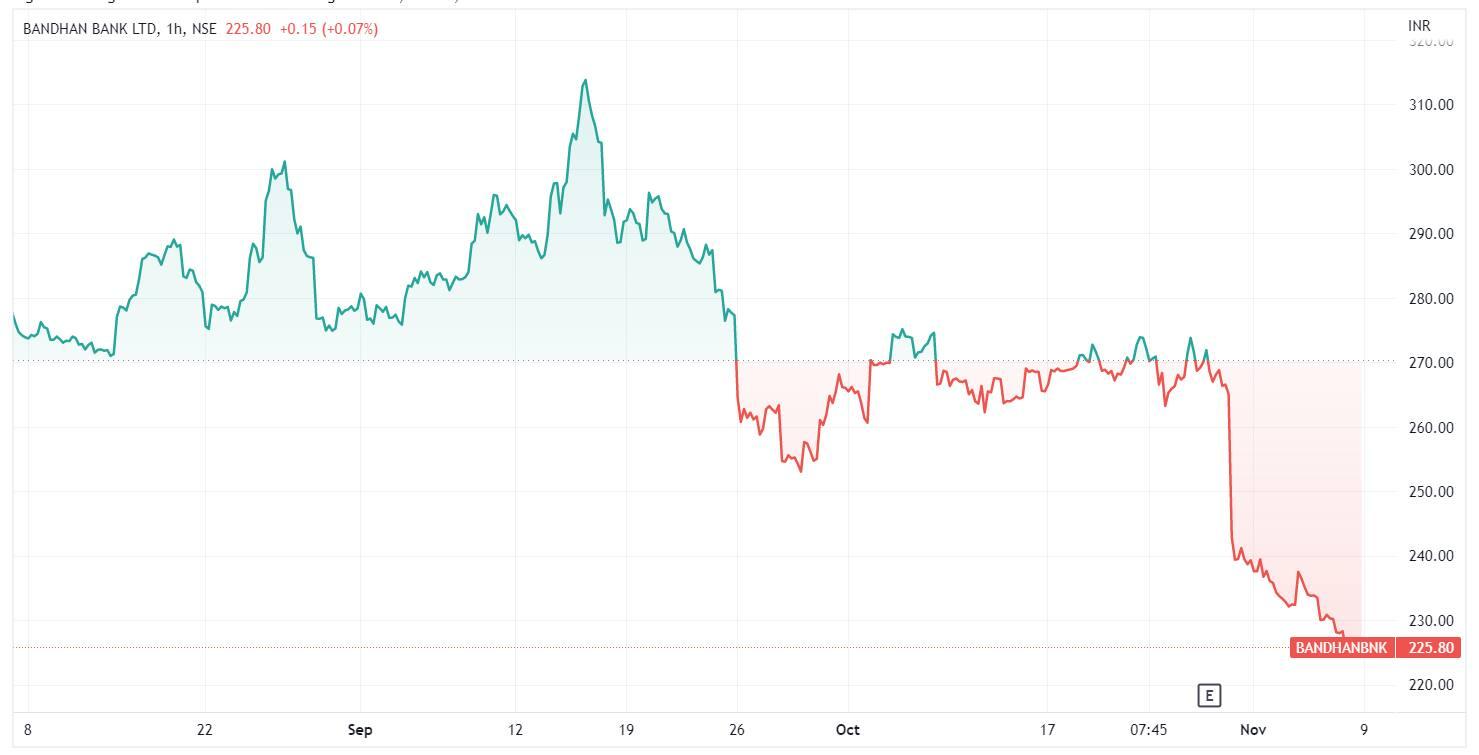

In Monday's intra-day trade, shares of Bandhan Bank dropped 1.07% to hit a fresh 52-week low of ₹224.2. In the last week alone the stock has lost 5.43% of its value. Since releasing the results for the September quarter, the stock has been falling. The stock has declined 16.66% in just eight trading sessions as a result of these results falling short of analysts' expectations.

For the September quarter, the bank reported a standalone net profit of ₹209.3 crore as against a net loss of ₹3,008.6 crore in the same quarter of last year. The provisioning requirement fell to ₹1,279.7 crore for the quarter as against ₹5,613.5 crore in the year-ago quarter. However, sequentially, the provisions were doubled, which led to a fall in the net profit of the bank.

The net interest income (NII) of Bandhan Bank fell 12.8% (QoQ) to ₹2,193 crore. while the net interest margin (NIM) of the bank contracted 100 basis points QoQ to 7.0%, lower than 7.6% in the similar previous period. During the quarter, the bank has written off ₹3,535 crore which is mainly due to micro-credit customers, which impacted the net interest margin. Also, the cost of funds rose 20 basis points (bps) to 5.5%, while the yield fell 40 bps to 12.0%. Operating expenses (OPEX) increased by 9.1% to ₹1,117 crore on the back of a rise in employee spending (up 5.0% QoQ) and other operating expenses (up 15.8%).

Additionally, the non-interest income of the bank fell by 9.2 per cent during the quarter to ₹476.4 crore from ₹524.5 crore a year ago. The capital adequacy ratio of the bank during the quarter stood at 19.4 per cent, and the Tier-I ratio was 18.4%, well above the required levels.

On the asset quality side, the bank showed improvement as the gross non-performing assets (GNPA) as on September 30, 2022, fell to 7.19 per cent of the gross advances as against 10.8 per cent as on September 30, 2021.

Domestic brokerages stayed bullish on the bank and raised their target prices. ICICI Securities has lowered its target price to ₹365 from ₹408 earlier and maintained a "buy" rating on the stock, which has an upside potential of over 63% from the stock's previous closing price.

Factoring in higher credit costs and incremental OPEX, the brokerage has revised earnings downward by 13% and 7% for FY23E and FY24E, respectively. "Disbursements in the EEB segment are normalising post-disruption in Q1FY23. Mortgage lending and commercial banking are gaining traction. " Franchise, post absorbing the interim EEB stress pool, has the potential to deliver more than 20% RoE," said the brokerage.

Strong growth in advances and deposits driven by the retail segment, improving asset quality, a pick-up in economic activities, and ongoing festive/ wedding season auger well for the company's future performance, according to Geojit Financial Services.

The brokerage said that the stock is currently trading at attractive valuations, close to its 52-week low. Hence, the brokerage has upgraded its rating on the stock to "buy" with a revised target price of ₹282/share.

While another brokerage firm, Motilal Oswal, said it remains watchful of asset quality and the high SMA book, which can keep credit costs elevated. The management has raised its credit cost guidance for FY23 to 3% from 2.5% earlier and has also guided at lower-than-trend growth due to tighter underwriting, it said.

The brokerage trimmed its FY23/FY24 earnings estimate by 18%/11% and maintained Neutral rating on the stock with a revised target price of ₹300, based on 2x FY24E BV.

On the stock performance side, the stock generated a negative return of nearly 30% in the past six months and 25% in the last one year and at current levels, the stock was trading 35% below its 52-week high of ₹349.6, set on May 17, 2022.

Meanwhile, Bandhan Financial Holdings, a holding company of Bandhan Bank, has received approval from the RBI for setting up an asset management company to run the mutual fund business. The Bank will start the credit card business on its own during the next financial year, according to the PTI report. .

An average of 26 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.