_1641277474905_1671088947033_1671088947033.jpg&w=3840&q=75)

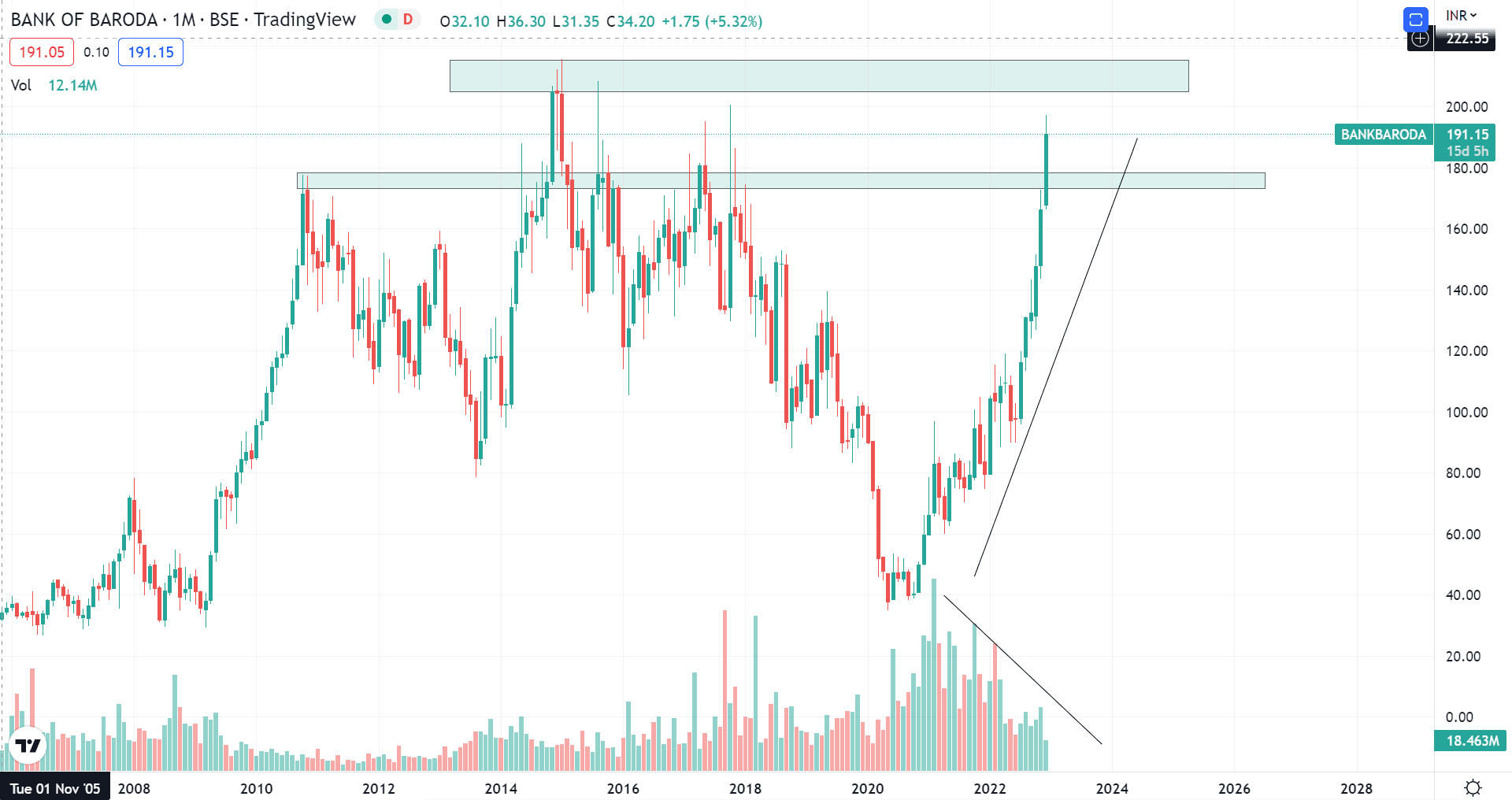

Shares of Bank of Baroda (BoB) have been witnessing a dream run in the recent past.

On May 20, 2020, the BoB stock hit its decade-low level of ₹36.05 when the coronavirus pandemic was ravaging the world. In less than three years, the stock has surged 431.5 percent.

This year till December 14, the stock has jumped 134 percent against an 8 percent gain in the benchmark Sensex.

Should you book profit?

What should you do with this stock after such stellar gains? Analysts and brokerages are of the view that long-term investors should stay invested because the fundamentals of the stock are intact. In the short term, however, one may take some money off the table.

Brokerage firm Nirmal Bang Institutional Equities believes that the stock continues to offer attractive risk-reward despite the strong gains after reporting a strong Q2FY23.

Nirmal Bang has maintained its 'buy' rating on the stock while it raised its target price to ₹225, implying a 17 percent upside.

"The stock is currently trading at 0.9 times and 0.8 times FY24E and FY25E ABVPS (adjusted book value per share) and we think it has the potential to deliver 1 percent RoA (return on assets) and nearly 14 percent RoE (return on equity) over the next two-three years," said Nirmal Bang.

As Mint reported, Bank of Baroda beat Street's estimates in the quarter ending September 30, 2022 (Q2FY23) period with profitability witnessing double-digit growth.

The bank garnered a standalone net profit of ₹3,312.42 crore in Q2FY23 rising by 58.70 percent from a profit of ₹2,087.85 crore posted in Q2 of the previous fiscal.

The bank's provision's declined, while asset quality improved sharply in Q2FY23. Its organic retail loan portfolio witnessed healthy growth with a strong performance in the personal loan book. Deposits and advances also registered robust growth in Q2FY23.

Nirmal Bang highlighted that the bank reported a steady improvement in its return ratios, with RoA and RoE inching up to 1 percent and 14.7 percent, respectively, as on Q2FY23. Moreover, it has been able to gain credit market share in the PSB (public sector banks) space, which now stands at nearly 6.4 percent, said Nirmal Bang.

Nirmal Bang expects the overall credit cost of BoB to moderate to nearly 1.2 percent over FY24-FY25E. It expects the bank’s NIM (net interest margin) to expand by 20bps, driven by the transmission of rate hikes, improving the credit-deposit ratio and change in asset mix.

T brokerage firm said the 90 percent linkage to floating rates also augurs well from a margin standpoint.

"The bank has a well granular and stable liability profile, which translates into a highly competitive Cost of Funds (CoF). Tier-1 capital currently stands at 12.8 percent and the bank has no plans to raise fresh equity capital in the near term. Our key thesis on BOB is premised upon improving financial performance and undemanding valuation," said Nirmal Bang.

It is always considered a good move to book some profit in a stock which has jumped abnormally. For BoB, too, analysts recommend booking some profit at this juncture even as fundamentals indicate a further rise in the stock price in the long term.

Jigar S. Patel, Senior Manager - Equity Research, Anand Rathi Share and Stock Brokers pointed out that ₹210 has been a historical resistance for the stock where one can see some profit booking.

Besides, on the indicator front, monthly MACD is overstretched along with volume dropping as the price increases, which is an anomaly according to volume price analysis.

"One can book a profit between ₹200-210 if already bought. As of now, no fresh longs are advised," said Patel.

Osho Krishan, Sr. Analyst - Technical & Derivative Research, Angel One also believes a minor profit booking is possible at this counter.

"BoB has witnessed a magnificent move in the recent period, and thus, one should not rule out the possibility of profit booking or cooling off the counter," said Krishan.

"The immediate support is placed around the ₹160-odd level, breaching which it may test the bullish gap of the ₹150 level. On the flip side, the intermediate resistance is placed around ₹200 odd level," Krishan said.

Pravesh Gour, a senior technical analyst at Swastika Investmart, pointed out that the counter is flying in a classical uptrend. It has witnessed a breakout of a downward sloping trendline at around ₹160 with a strong volume on the longer timeframe.

"On the daily chart, it has broken out of a long upward-sloping consolidation channel. The overall structure is impressive, as it trades above its all-important moving averages. The momentum indicator RSI (relative strength index) is also positively poised, whereas MACD (moving average convergence divergence) is supporting the current strength," Gour underscored.

"On the higher side, ₹200 is the immediate psychological resistance level; above this, we can expect a move to ₹224+ levels in the near term, while on the downside, ₹160 is the strong support during any correction," said Gour.

According to a MintGenie poll, an average of 32 analysts have a ‘strong buy’ call on the stock.

Disclaimer: The views and recommendations given in this article are those of individual analysts and broking firms. These do not represent the views of MintGenie.