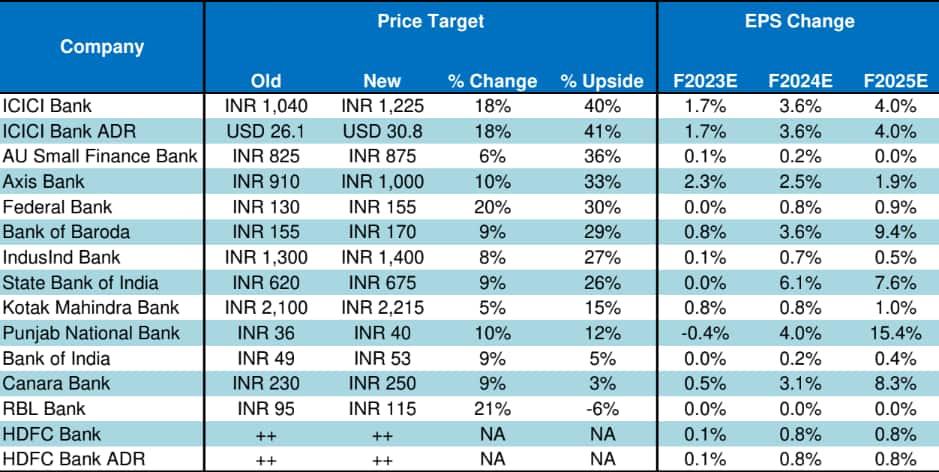

Strong balance sheets, lessening macro concerns, and improving capacity utilization set the stage for a re-rating of Indian banks, a report by global brokerage house Morgan Stanley stated. The brokerage raised estimates and price targets for around 12 lenders and prefers ICICI Bank, Axis Bank, Bank of Baroda, and SBI among them.

The other banks it raised estimates and targets for include AU Small Finance Bank, Federal Bank, IndusInd Bank, Kotak Bank, Punjab National Bank, Canara Bank, and RBL Bank.

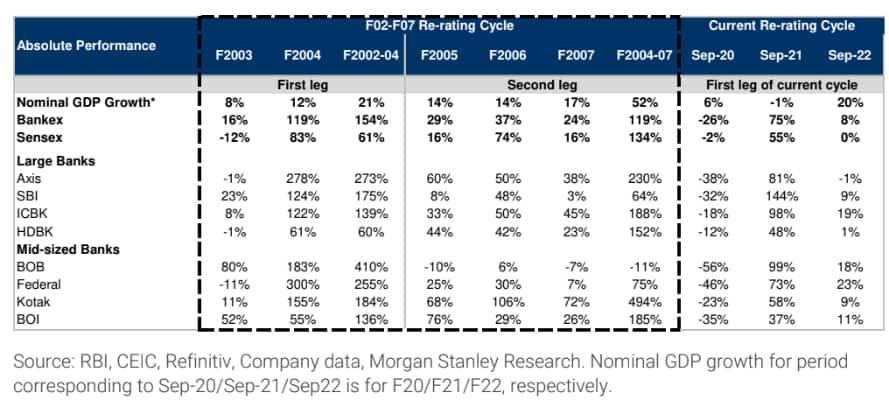

The brokerage explained that bank stock re-rating cycles work in two legs and currently Indian banks appear to be in a transition phase between the two. As per MS, the first leg is usually driven by expectations around better asset quality. As tail risks recede, stocks improve sharply to normalized multiples, which has already occurred over the past two years, noted the brokerage. Meanwhile, the second, more sustained leg is usually driven by loan growth acceleration that sets an earnings upgrade cycle, and we believe catalysts for this are falling into place, it added. Currently, the brokerage feels that the Indian banks are moving towards the second leg of the re-rating cycle.

The brokerage noted that over the past two years, Indian bank stocks have returned to average valuations as the economy improved. The Bankex has risen 73 percent over the past two years, compared to 53 percent rise in the Sensex. Amongst banks, HDFC Bank and Kotak underperformed Bankex, and increased by 33 percent and 39 percent, respectively, during the period.

As per MS, banks that were not pricing in normalized credit costs saw significant outperformance relative to the Sensex. Up-fronted provisioning as well as muted trailing loan growth/low job losses supported asset quality outperformance. It noted that this has been similar to trends seen in a post-slowdown recovery period when value stocks outperformed quality and the current cycle recovery and stock performances have behaved similarly to that seen in FY02-04.

"Stocks that were not pricing in credit cost normalization did well and drove the first leg of re-rating: This was helped by strong improvement in India banks' balance sheets over the past five years despite the COVID crisis. With this, we believe bad loan normalization is in the price for most Indian banks," explained the brokerage.

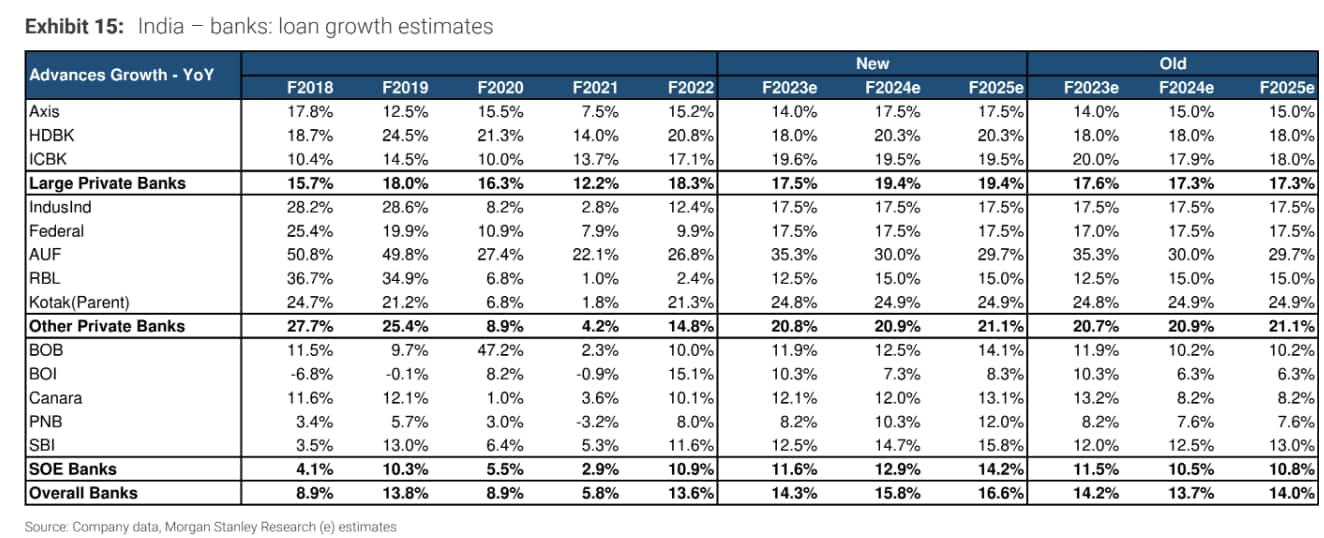

The next leg of re-rating should be driven by loan growth acceleration, said MS. It expects loan growth to accelerate and be sustained, as capex spending accelerates. MS also sees a new leg of investment up-cycle led by improving trends in capacity utilization rates, in addition to corporate sector profitability and de-leveraged banking sector balance sheets.

"This in turn could foster job creation, accelerate income growth, and drive more growth opportunities even in the retail/SME segment. In this report, we raise loan growth estimates by 2ppts to 16 percent for F24 and 3ppts to 17 percent for F25; this, coupled with lower credit costs, drives our earning estimate upgrades (2ppt upgrade in PPoP growth) and higher RoE assumptions," said MS.

The brokerage sees Indian banks' earnings entering a sweet spot - strong core PPoP growth with low credit costs should drive strong improvement in return ratios over the next 2-3 years. It believes banks with higher liquidity and the ability to gain market share are better placed. It also expects margins to expand by 15-25bps over the next few years.

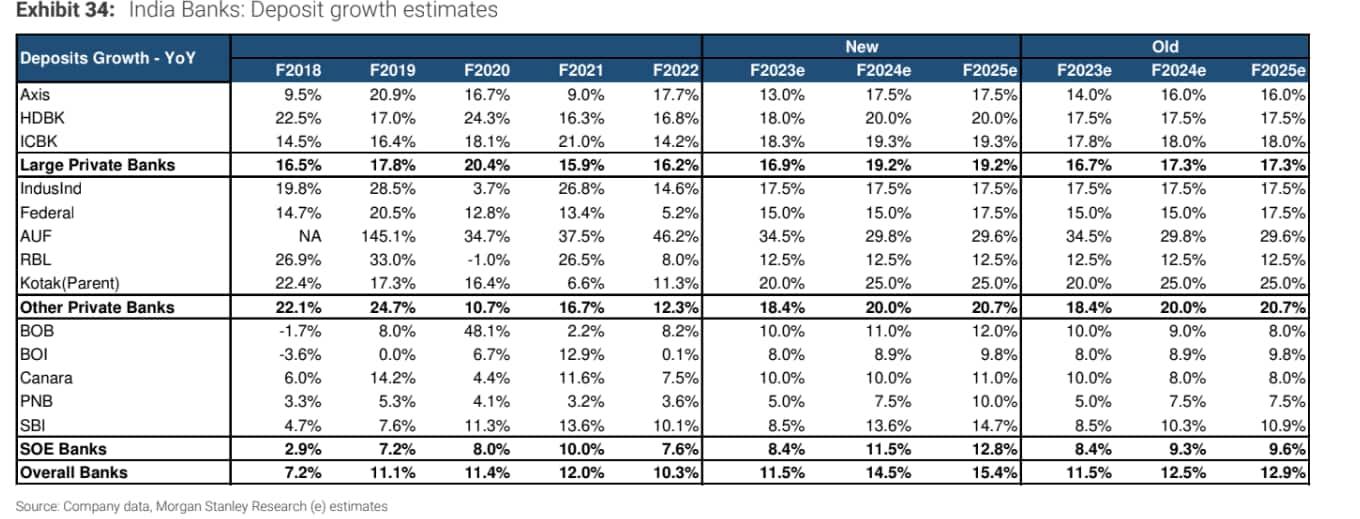

The brokerage believes that access to retail deposits could be key for delivering profitable revenue growth.

"We expect competitive intensity in retail deposits to reach a new high in the upcoming up-cycle. Private banks in aggregate have lagged on retail deposit market share gains, and are turning aggressive. Moreover, LCR regulations and bank mergers would intensify competition. Large banks - both private and public- stand out, in our view, and appear better placed to accelerate loan growth and gain share," the brokerage highlighted.

It raised valuation multiples to reflect improved growth and profitability outlooks over the next few years.

Scan for stocks that are not fully pricing in a growth up-cycle, have access to retail deposits and high liquidity and appear well equipped to accelerate market share gains as the macro outlook improves, it believes ICICI Bank, Axis Bank, Bank of Baroda, and SBI are well placed to capitalize on the upcoming growth cycle. It also remains selective on mid-sized banks, with Federal and AU Bank as its preferred picks.

As per Morgan Stanley, large private banks have seen significant moderation in LCR (liquidity coverage ratio) ratios over the past four quarters as loan growth accelerated. ICICI stands out with 125 percent LCR, compared to 108 percent for HDFC Bank and 117 percent for Axis. That said, it noted that HDFC Bank continues to deliver the lowest deposit outflow rate among large private banks.

"We believe large private banks are well placed to capitalize in upcoming deposit competition challenges. All three large private banks (HDBK, ICBK and Axis) have accelerated their presence in interior India and appear better placed to deliver. They have also improved digital capabilities sharply in recent years, which can help drive better cross-sell ratios," said Morgan Stanley.

Amid mid-sized banks, deposit outflows are highest for IndusInd and RBL Bank, noted MS. Meanwhile, Federal Bank stands out with higher LCR and a relatively lower deposit outflow run-rate at 16 percent (even better than large private banks), it added.

It further stated that AU Small Finance Bank is also at the relatively lower end.

"A few banks are tying up with fintech to better address challenges, which in our view is a good strategy if economics to cross-selling is not hindered. One of the primary hooks for these banks to gain retail deposit market share is by paying up on retail term deposits. Banks that have relatively higher loan yields with strong underwriting capabilities will likely be better placed against this backdrop - AU small finance bank and IndusInd, therefore, are preferred within this group after Federal Bank," explained MS.

Key risks to the rerating, as per MS, could be 1) Weaker-than-expected external demand weighing on growth acceleration, 2) slower than expected acceleration in deposit growth, and 3) greater than expected competitive intensity.