After losing over 50 percent of its investor wealth in a little over a year, some recovery is seen in the IT stock Birlasoft going ahead.

Brokerage house Religare Broking has retained its buy call on the stock with a target price of ₹341, implying a potential upside of 24 percent from the current market price of ₹275 (as on February 28, 2022). Near-term challenges remain, however, the firm's long-term outlook may see improvement, noted the brokerage.

The stock has fallen as much as 53 percent from its record high of ₹586, hit in January 2022. Meanwhile, from its 52-week high of ₹501.65, touched on April 11, 2022, the stock has shed over 45 percent.

It recently hit its 52-week low of ₹250, on February 3, 2023.

The stock has fallen 32 percent in the last 1 year, 14 percent in the last 6 months and the same 14 percent in the last 3 months as well.

The scrip shed 9 percent in February 2023 after a 1 percent rise in January of the current calendar year. In 2023 YTD, it is down over 7 percent.

However, from a long-term perspective, Birlasoft has given multi-bagger returns in the last 3 years, rallying as much as 210 percent.

Birlasoft is engaged in providing information technology (IT) services, consulting, and business solutions. The Company provides a range of services, which includes digital and enterprise technologies and services. Its digital services include data analytics, connected products, intelligence automation, connected products, cloud, and blockchain. It serves various industries, which include automotive, banking, manufacturing, capital markets, insurance, media and entertainment, energy and resources, life science and healthcare and utilities.

In the December quarter (Q3FY23) Birlasoft reported a loss of ₹16.36 crore against a profit of ₹115 crore in the July-September (Q2FY23) quarter. Meanwhile, in the December quarter last year, the firm had posted a net profit of ₹114 crore. Its revenue, however, rose 14 percent YoY to ₹1,222 crore from ₹1,072 crore in the year-ago period.

Post the December quarter earnings, Religare noted that the revenue growth was mainly driven by strong demand for technology transformation and cloud services businesses while muted performance was seen in its enterprise solution business which impacted the growth.

The company’s EBITDA was down by 95.5 percent YoY and 95.8 percent QoQ to ₹7.4 crore, due to a rise in other expenses by 59.6 percent YoY and 49.9 percent QoQ, further observed Religare. Also, its EBITDA margin came in at 0.6 percent as it declined by 1,458 bps YoY and 1,419 bps QoQ.

The brokerage further noted that Birlasoft's Revenue/Operating performance and profits were impacted as one of its major clients Invacare has filed for bankruptcy and the company has created a provision for ₹151 crore and further they are not expecting any revenue in the next quarter.

Also, the contract value of deals saw moderation of 26 percent YoY and 16 percent QoQ and stood at $102 million for Q3FY23, it added.

"In the near term, management believes the performance will remain impacted due to bankruptcy filed by one of its clients and macro headwinds. However, going ahead the revenue growth is expected to be driven by improvement in the deal pipeline for cloud and technology business, continued momentum in BFSI and pickup in demand from manufacturing and also an uptick in deals from Europe and America region as well as focus on managing cost will aid in improving operating performance," stated the brokerage.

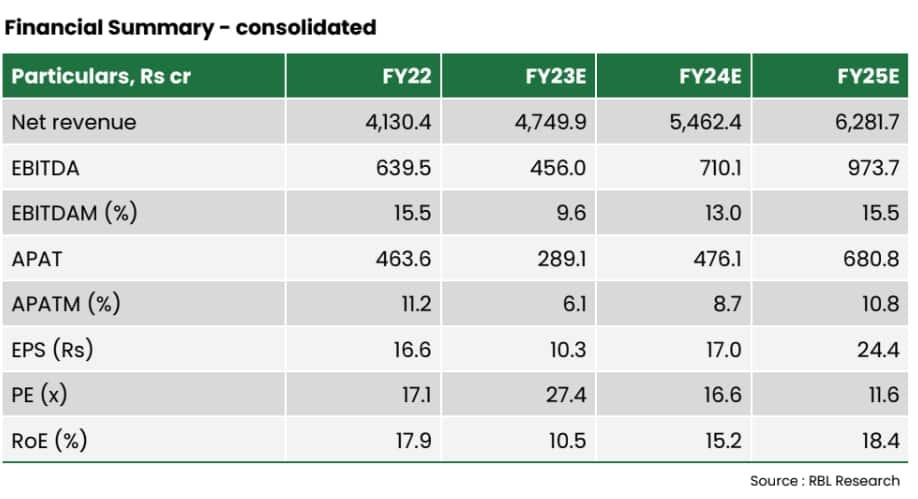

On the financial front, Religare incorporated Q3 provisions made by the company as well as there are near-term challenges, however, the long-term growth outlook may improve. Thus, it revised its target price downwards to ₹341, valuing the company at a 14x PE multiple on an FY25E EPS basis.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.