Aurobindo Pharma has bought Veritaz Healthcare in an all-cash deal worth ₹1.7 billion. This is in line with the pharma major's goal of entering the India formulations business.

Aurobindo Pharma has a sales goal of ₹1 billion in this business by financial year 2025.

Surajit Pal and Shaad Shaikh of Bobcaps Research, in a report dated March 30, 2022, said, “Veritaz services an addressable market worth ₹268 billion and based on 9MFY22 numbers, the acquisition is valued at 1x FY22E sales and 9.8x FY22E EBITDA (annualised)."

Vertiz Healthcare is promoted by the sons of the ARBP promoter and hence the deal is a related-party transaction. In addition, it is a slump sale and has no debt liability or cash benefits.

Some More Details

Incorporated in September 2006, Veritaz is engaged in wholesale marketing and distribution of branded generic formulations in acute therapeutic areas (anti-infectives, PMS), nutraceuticals and toiletries. The company markets 40 brands across sectors and has 180 registered trademarks. Its largest brands are Fepanil (Paracetamol, sales: ₹310 million in FY21) and Merogram (Meropenem injectable, sales: ₹200 million). Veritaz plans to launch products in cardiology/diabetic and orthopaedic/gynaecology segments in the near term. With 900 employees (including 700 representatives) at Veritaz, the acquisition enables ARBP to reach over 70k doctors, 50k retailers and 1,700 stockists in 23 cities.

Analyst View

Pal and Shaikh wrote, “While the acquisition offers opportunities for ARBP to build a presence in India formulations, we note that Veritaz has low-value products in highly competitive segments and reasons for the related-party transaction aren’t very compelling.”

They further said, we expect monetisation of ARBP’s global IPR in India to have back-ended benefits while the addition of employees and brands/promotions related to the deal will raise overhead expenses from FY23. We await better clarity on the strategy and financial planning post acquisition before incorporating Veritaz into our estimates.

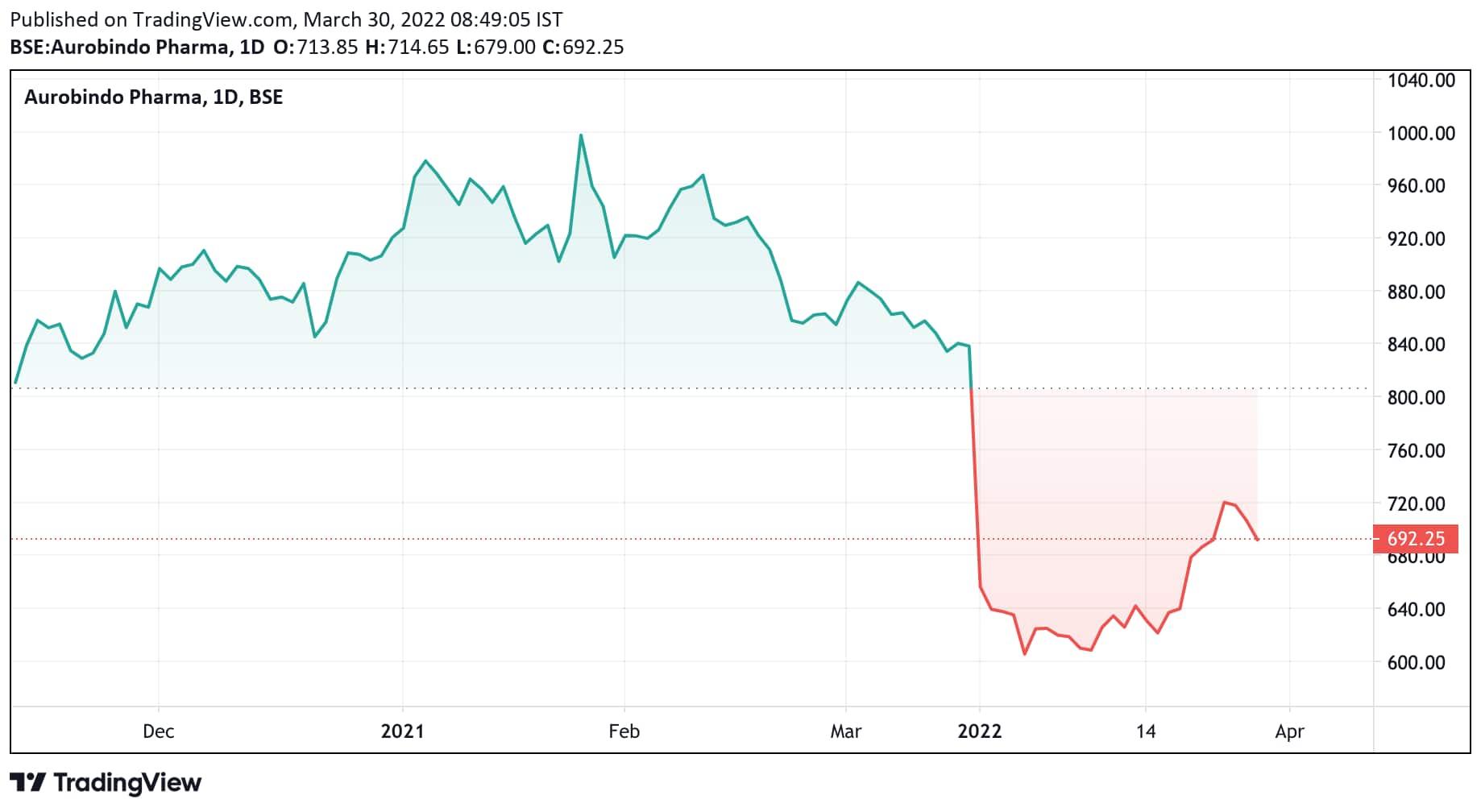

However, the two also said, "Aurobindo Pharma is trading at attractive valuations of 5.8x FY24E EV/EBITDA (9.3x FY24 P/E). We reiterate BUY and maintain our TP at ₹850, based on 7.5x FY24E EV/EBITDA (implied P/E of 12x). Our target multiple reflects a continued 45% discount to other frontline stocks (SUNP, CIPLA, DRRD) due to ARBP’s low branded sales and high US exposure."

An average of 28 analysts polled by MintGenie have a ‘buy’ call on the stock

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.