Brokerage firm Motilal Oswal Financial Services has a buy call on Brigade Enterprises (BEL) stock with a target price of ₹720, implying a 55 percent upside potential.

The brokerage firm retained its bullish view on the stock after it had an interaction with the management of the company to understand its business outlook.

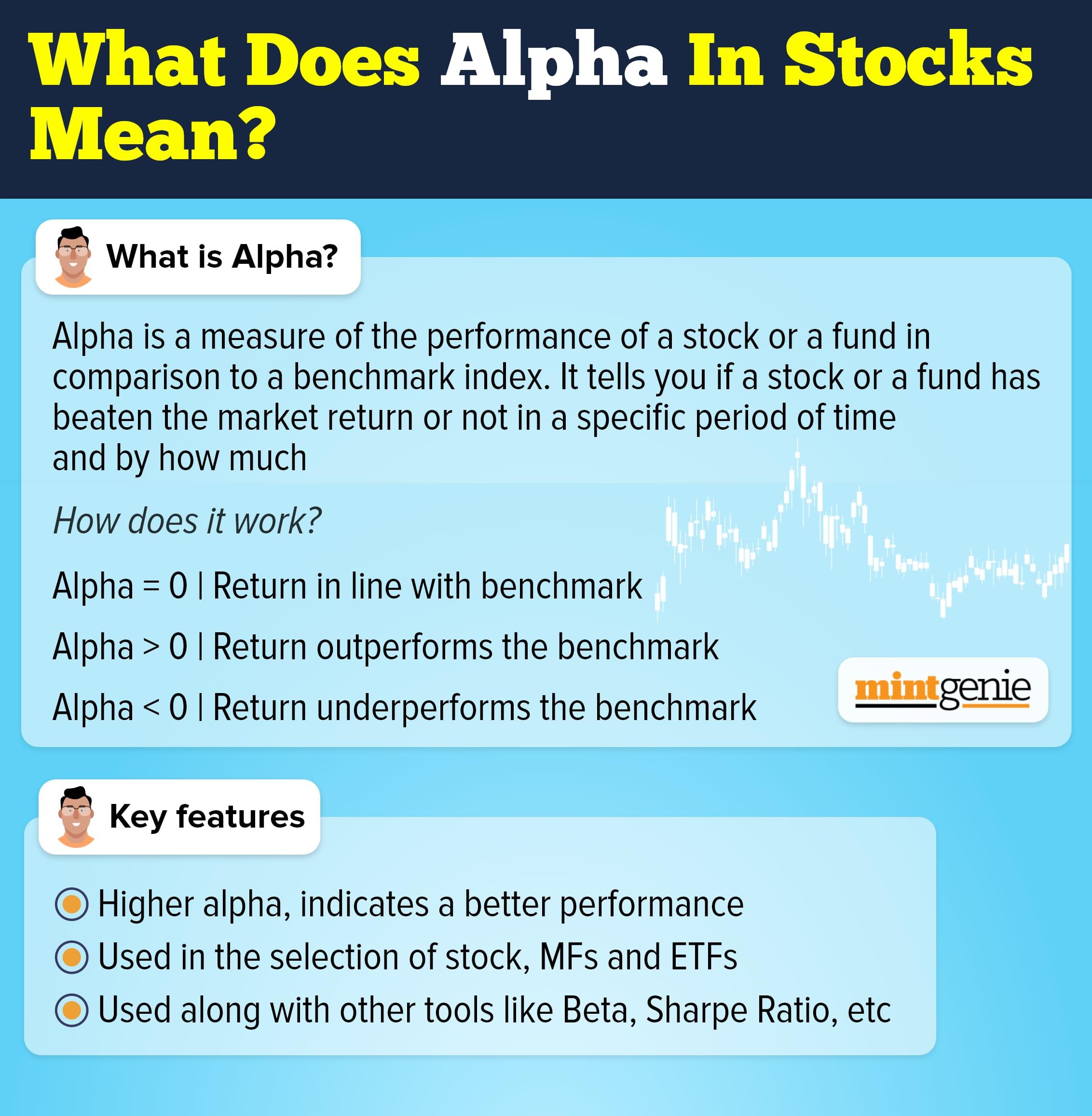

Motilal Oswal highlighted that Brigade Enterprises' demand momentum is intact due to favourable affordability despite a 200bps increase in interest rate.

The company expects to launch 13msf of projects over the next 12 months. Its management reiterated its target to grow sales volumes by 15-20 percent over the next three years, Motilal Oswal said.

Moreover, the company's focus on business development may continue across Bengaluru, Chennai, and Hyderabad and it expects the commercial portfolio to be fully leased by Sep-23, said the brokerage firm.

The stock has underperformed the benchmark Sensex in the last one year but has outperformed its sectoral index BSE Realty.

Investment rationale

Demand momentum intact: The brokerage firm underscored that the company's management indicated a healthy demand scenario. "The demand momentum continues to remain intact as witnessed through steady progress on sustenance sales as well as a strong response to recent launches," it said.

As per the management, affordability continues to remain intact despite 200bps rise in mortgage rates as monthly EMIs at ₹83,000-84,000 (for a mortgage of ₹1 crore) is still below their peak of ₹1 lakh in 2015-16.

Motilal pointed out that the average household income for homebuyers in Bengaluru has doubled to ₹45-50 lakh over the last five years. Hence, affordability is still not a challenge until the interest rate reaches a psychological barrier of double digits.

"The company remains confident of delivering 15-20 percent CAGR in pre-sales volumes over the next three years and is gearing up its launch and project pipeline to meet the target. We expect the company to deliver 17 percent CAGR in pre-sales over FY23-25 to 7msf at a value of ₹4,800 crore," said Motilal Oswal.

Focus on business development to remain intact: As per the brokerage firm, over the last 12 months, the company has added 10msf of residential projects.

"Currently, BEL has nearly 40msf of residential projects under pipeline, of which, 13msf is slated to be launched over the next 12 months. The remaining 27msf of projects under pipeline provides visibility for three-four years," said the brokerage firm.

Motilal added that the management generally prefers a visible pipeline of five-six years, hence, the focus on business development will remain intact, especially in its core markets of Bengaluru and Hyderabad.

Confident of fully leasing its commercial portfolio by Sep’23: Over the last 12 months, the company has leased 1.2msf of space in its operational commercial portfolio. While the leasing traction has been slower than expected, the company expects to lease out its portfolio by Sep’23 fully, said Motilal Oswal.

The brokerage firm expects the rental income to record a 15 percent CAGR to ₹800 crore by FY25.

"Brigade Twin tower (1.2msf) is expected to be delivered over the next 18 months and will take the rental income to ₹1000 crore and EBITDA to ₹750 crore. However, its contribution is not considered for a valuation right now. Additionally, it is evaluating one more commercial project (2.0msf) along with mixed-use development in Chennai TVS land (0.3msf), which provides growth visibility in the rental portfolio even beyond FY25," said Motilal Oswal.

Re-rating in valuation possible: Motilal Oswal said it derived a value of ₹6000 crore for its commercial business ( ₹550 crore EBITDA valued at 8.5 percent cap rate) and ₹2,500 crore for its hospitality business ( ₹150 crore EBITDA at 17.5 times EV/EBITDA).

"At its current valuation, it implies ₹3500-4000 crore for its residential business, which would be equal to NAV of its existing residential project pipeline, indicating zero growth value," said Motilal Oswal.

"A pick-up in business development activity by BEL will lead to re-rating in valuation for its residential segment," said the brokerage firm.

Disclaimer: The views and recommendations given in this article are those of the broking firm. These do not represent the views of MintGenie.