Indian markets have lost over 5 percent in 6 sessions on the back of a hawkish Fed. However, Indian markets are still better placed than global peers. While the US markets have entered the bear category, with Dow Jones down over 20 percent from its 52-week high, Nasdaq is down 33.2 percent from the peak and S&P 500 is down 24.3 percent from the peak. The Euro Stoxx 50 is down 24.3 percent from its peak. These are clear bearish signals from markets in the developed world.

India is a distinct outlier with only a 9 percent decline from the peak in Nifty. India can remain an outperformer supported by its strong fundamentals but India cannot remain immune to major global trends. Will this outperformance against global peers? Brokerage house Phillip Capital analyses.

According to the brokerage, post the hawkish Fed, it expects the rupee to weaken further, global growth to be severely dented as aggressive tightening takes place across nations, and an adverse impact on global earnings and equities.

For India, while we can outperform, we cannot fly against the wind, warned the brokerage.

"Structurally, India is best placed in the long-term but only at certain valuations. Considering the risks and valuations, we turned neutral in Nifty at 17,300-17,400 and cautious-negative at the latest peak. For March 2023- September 2023, we continue to hold our long-held Nifty target at 18,000-19,000," it said.

However, the long-term positives for India are intact, it added. The brokerage continues to advise buy-on-dips for a long-term portfolio. Positive festive season cues were well-factored in at the peak of equities, it further noted.

Phillip Capital also pointed out that the upcoming RBI policy will be crucial to gauge RBI’s stance post a slew of global central banks' policies. It will help us better gauge our future stance on interest rates, currency and equities, it added.

The brokerage has listed some reasons that will linger on equities in the near term; some of the below factors are a watch list, it added. Let's take a look:

Tight domestic liquidity and prevailing elevated borrowing cost: It’s not a desirable mix for the accelerated expansion of an economy considering a higher inflationary scenario, said the brokerage.

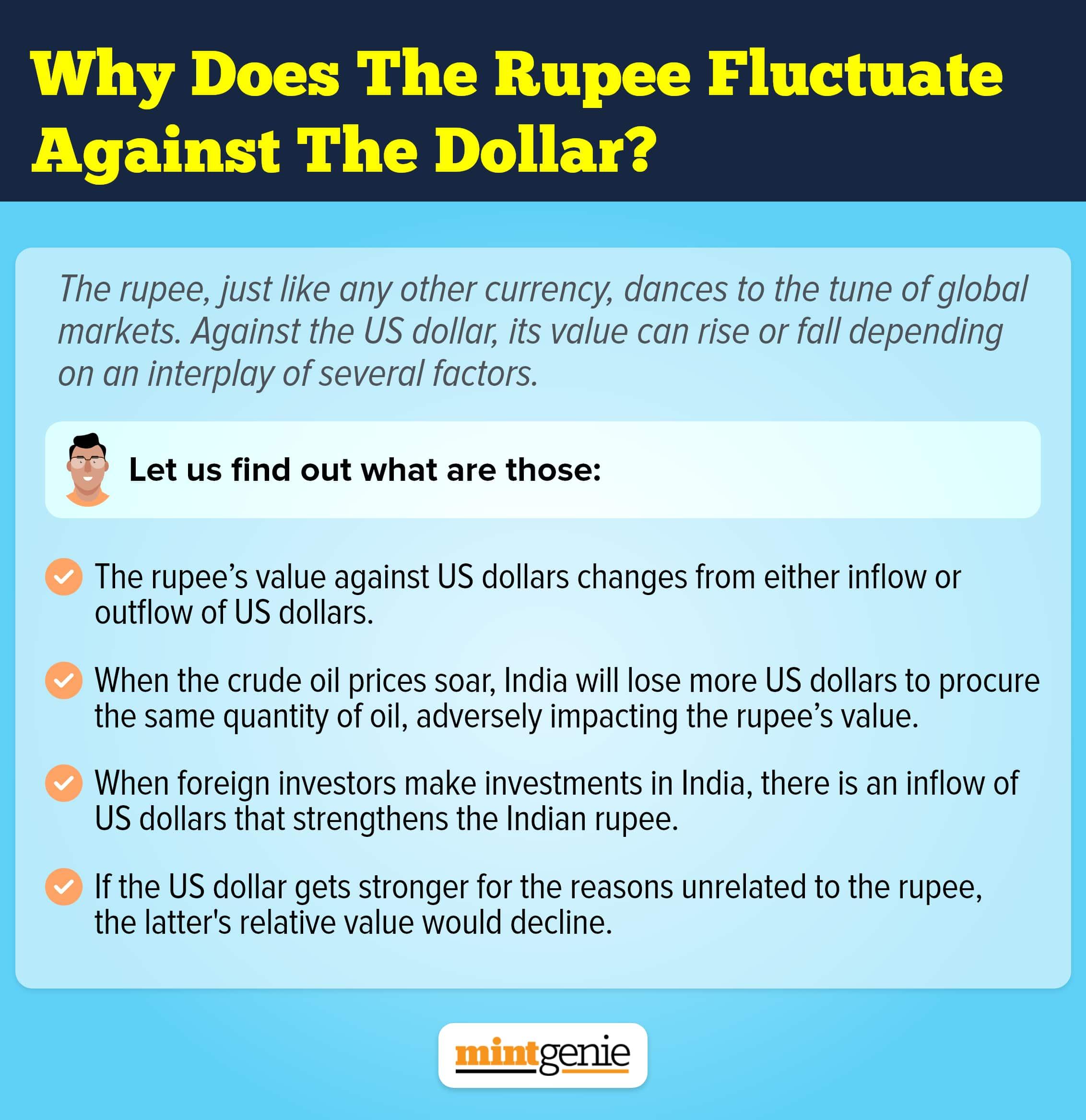

Depreciating USD-INR: Considering DXY levels that are being talked about, the rupee can further weaken against the Dollar (82-85), stated PC. While, lower brent prices are positive for the current account deficit; a lower yield gap will incrementally weigh on debt flows and rupee, it added.

Forex reserves: Strong forex position has worked in the advantage of the health of the Indian economy post covid. But, India has seen a dip of $95 billion from the peak owing to capital outflows and RBI intervention noted the brokerage. The current forex reserves of $485 billion are robust, however, diminish RBI’s ammunition power, it pointed out. It stood at $450 billion pre-covid.

Further tightening: RBI is expected to tighten the repo rate by 35-50 bps in the upcoming monetary policy. They may have to continue tightening considering rupee weakness, rising food inflation, and yield gap, cautioned Phillip Capital. This can take bond yields higher even from the current levels, further raising the borrowing cost, it warned.

Fiscal deficit: While the brokerage does not expect significant stress in FY23, it sees the second-half borrowing calendar to be in sync with budget estimates. Government borrowings are generally elevated considering historical standards, not offering support to bond yields, it added.

FII flows: BS tightening by Fed will adversely weigh on FII flows. This will also impact the free flow of private equity investments which was booming in the last couple of years, contributing to the expansion of certain sectors and employment generation, noted the brokerage.

Swift and sharp global tightening sharply raise the risk of a slowdown in many economies simultaneously. This along with lingering geo-political risks doesn’t offer any confidence in global equities, pointed out the brokerage.

DII flows: Considering last year’s trend, DII flows have substantially softened, however, ₹10,000/month is reasonable. That said, in case of FII outflows and equity drop, this quantum will fall short to support markets, stated the brokerage.

Leverage-driven expansion: In the last couple of years, the brokerage said that it has seen meaningful reliance of the retailers on leverage spending, in which the cost of borrowing plays an important role. It will be watchful of this segment, going ahead, said PC.

Growth trajectory: The brokerage continues to estimate GDP growth of 6.5-7.5 percent in FY23-24 but higher interest rates are a downside risk to these estimates. But as per the brokerage, the festive season is expected to be buoyant and imports used for the economic expansion will be costly.

Exports: While a weak Rupee is a positive for exports, however, the global economic slowdown will not be a supportive factor in the medium-term, said PC.

These above-mentioned factors will impact the equities going ahead.