The Indian rupee has been under pressure in the last one year, moving from the levels of 72.77 per dollar to 77.93 per dollar. So far in the calendar year, the domestic unit is down about 5 percent.

Can the rupee go beyond 80 per dollar mark by next year?

TL;DR.

- Given that Fed will continue to deliver rate hikes till the year-end and high oil prices will expand the current account deficit, the Indian rupee can depreciate further.

The rupee has been reacting to deteriorating macroeconomic indicators such as widening current account deficit, fiscal deficit and trade deficit while higher inflation and rate hikes by the US Fed have added further pressure to the currency.

Given that US Federal Reserve will continue to deliver rate hikes till the year-end and high oil prices will expand the current account deficit, the Indian rupee can depreciate further.

On June 8, the Reserve Bank of India raised the repo rate by 50 bps to keep inflation under control. However, considering the evolving geopolitical scenarios, the possibility of inflation coming down looks feeble. Some analysts believe the Indian rupee will continue to depreciate in the coming year.

Naveen Mathur, Director, Commodities and Currencies, Anand Rathi Shares and Stock Brokers expects the rupee to cross 80 levels in the coming months owing to weak fundamentals.

"Surging commodity prices, especially crude, might widen the trade deficit further, which has already widened to a record $23.3 billion in May 2022. Meanwhile, theaggressive Federal Reserve rate hike cycle ahead might amplify the capital outflows, causing thebalance of payments to widen further in the current fiscal. Rate hikes by RBI might not be sufficient, as Fed is better prepared to deliver multiple 50 bps hikes, which might lead to prolonged dollar rally this time and Rupee might eventually depreciate," said Mathur.

"So far, the outlook for the Indian rupee does not appear promising, with the USD/INR likely to fall to 80 per dollar by 2022-23," said Kshitij Purohit, Lead - commodity and International Research at CapitalVia Global Research.

Hitesh Jain, Lead Analyst – Institutional Equities, Yes Securities believes the downside in the rupee can extend to 78.5 but thereafter we should see a bottom around those levels.

Dilip Parmar, a research analyst at HDFC Securities believes spot USD/INR may consolidate in the range of 79 to 76 for the rest of the year.

The rupee's trajectory will depend on how the dollar behaves in the coming months. Some analysts believe the US economy may see capped growth due to aggressive rate hikes and slowing global economies. This will weaken the dollar and help the emerging market currencies, including the rupee.

"Over the next one year, we can see the situation change for the Rupee. The next couple of quarters are going to be challenging as fast hikes from Fed and higher commodity prices can cause Rupee to depreciate. However, over the next 9/12 months, we expect the US economy to slow down on the back of slower global growth, high inflation and higher cost of funding due to rapid rates from the Fed. This will allow for the dollar to depreciate in the Q3-Q4 of FY23. As a result, USD/INR which runs the risk of 78.50-79 over the next two quarters, may very well reverse course and decline towards 77 levels during the second half of the financial year, due to improved FPI inflows," said Anindya Banerjee, VP, Currency Derivatives & Interest Rate Derivatives at Kotak Securities.

What should the RBI do?

India’s forex reserve has declined about 7 percent from its record high of over $640 billion last September. However, it is still well on key matrices like import coverages and short-term debt obligations.

Purohit believes a limited intervention technique could be used by the RBI to maintain ammunition amid a broad currency rise spurred by expectations of aggressive monetary tightening by the Fed.

"The RBI's declared goal remains to reduce excessive currency volatility, and reserves have declined in recent weeks, indicating market intervention. The RBI may be content to take no action to put pressure on exporters. However, if necessary, it may urge exporters to return dollars more quickly," said Purohit.

"Putting a restriction on outflows would be insulting, given that our economy is still relatively closed on the capital account. So, unless the RBI is forced to act, I don't expect any limitations on outflows," he added.

There are concerns that since India's forex reserve has declined in the recent past, RBI might not sell dollars aggressively to save the rupee. Also, the depreciation of the rupee would mean an optical rise in India's forex reserves.

However, analysts believe RBI would do all that it can to stabilise the currency. They underscore that the RBI targets to keep the rupee stable and they achieve that by intervening on both sides of the market when the rupee shows signs of becoming an outlier amongst its peers. This policy should continue, ensuring the rupee remains a well-managed currency.

"Rupee depreciation can help RBI’s economic capital, as per Bimal Jalan Committee Report. But that deprecation has no impact on realised equity of RBI. RBI would continue to keep the rupee a median performer amongst its peers. Buying the dollar when the rupee is too strong and selling when the rupee is too weak," said Banerjee.

Mathur underscored that RBI reserves have fallen below $600 billion in May, from an all-time high of $642.45 billion in September 2022, amid intervention to prop up the domestic currency from the fallouts of Russia Ukraine war.

A falling rupee at a time of declining forex reserves is very much not in RBI’s favour, as it would add to imported inflation, putting further pressure on RBI.

Mathur said that the best thing for the RBI to do is to continue with the rate hike trajectory which will cool off inflation and support the rupee.

It is also a fact that the RBI will buy the dollar when it sees weakness in the greenback. As Jain pointed out, although RBI has intervened to stem the volatility in the rupee, the central bank is inclined to maintain a high buffer of forex reserves as an insurance against growing volatility and evolving geopolitical situation. So though RBI is selling dollars in spot markets to limit the downside in the rupee, it is maintaining a healthy level of net purchases of dollars in the forward markets.

Parmar said even after a whopping $28 billion in outflows in the last nine months from foreign institutions, RBI managed to curtail sharp depreciation. Near term worry for the RBI, along with the other central bank, is to control the surging inflation and for that stability in the currency is a must, he said.

Disclaimer: The views and recommendations made above are those of individual analysts and not of MintGenie.

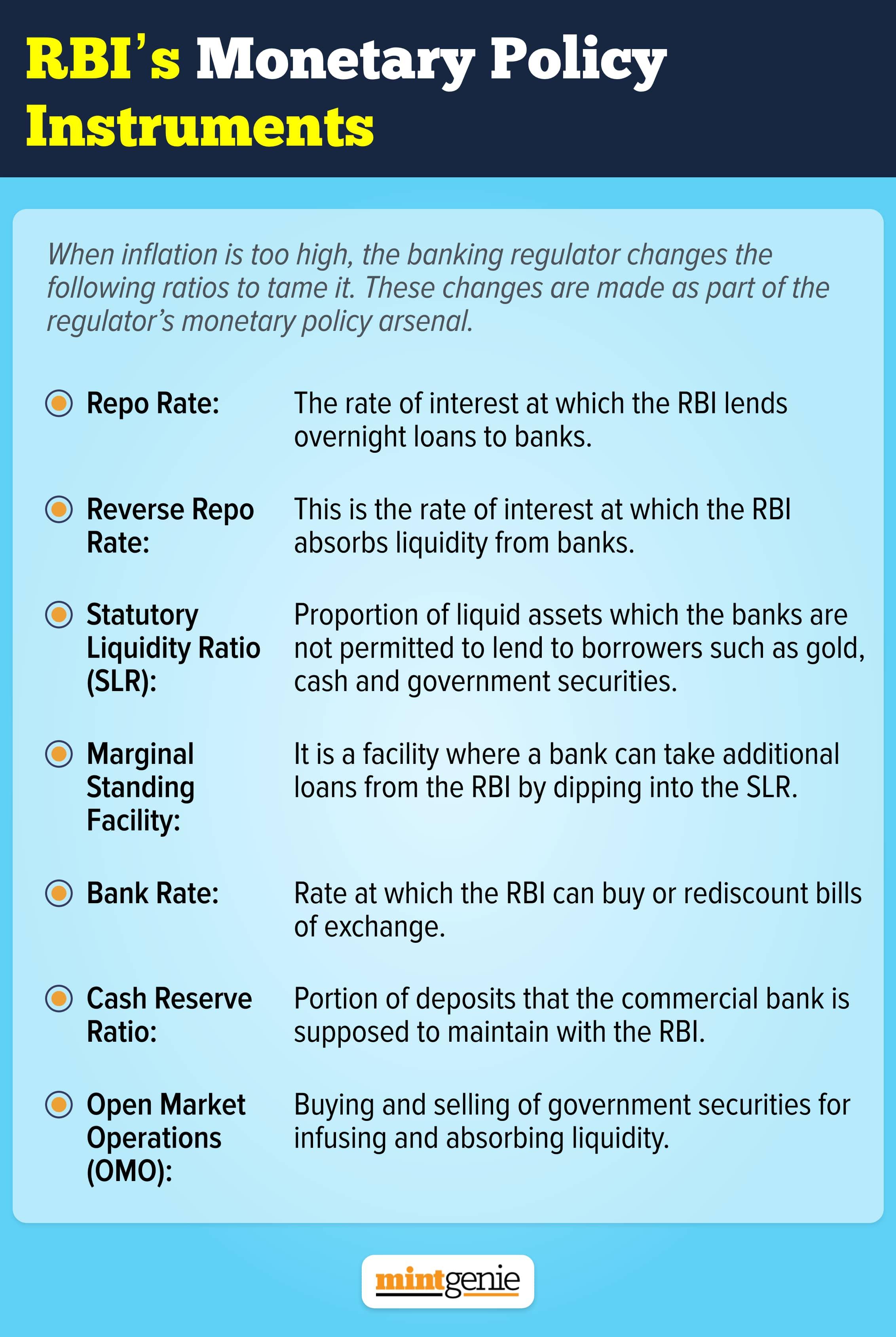

These are the RBI's monetary policy instruments.

First Published: 09 Jun 2022, 07:43 AM IST