After a challenging year, the cement sector in India is likely to witness the twin advantage of better demand and softening of operating costs, thereby leading to the recovery of margins, domestic brokerage house Centrum Broking stated in a recent report.

"Over the past year, the industry had faced challenges related to surging operating costs i.e., coal and pet coke, and we believe that the sector has managed to balance the cost pressures and demand well. Margin recovery has already started from 3QFY23 and we expect normalization of margins in FY24E given softening costs and better realizations," explained Centrum.

It expects cement demand to grow at a healthy demand CAGR of 7.8 percent over FY22‐25E driven by pre‐election spending by the government and affordable housing segment. Cement prices are likely to remain steady in FY23E with some improvement expected in Q2FY24E, it estimated. It sees an 11 percent and 12 percent CAGR in revenue/EBITDA for its coverage universe over FY22‐25E and expects EBITDA/mt to reach FY21 levels by FY24E.

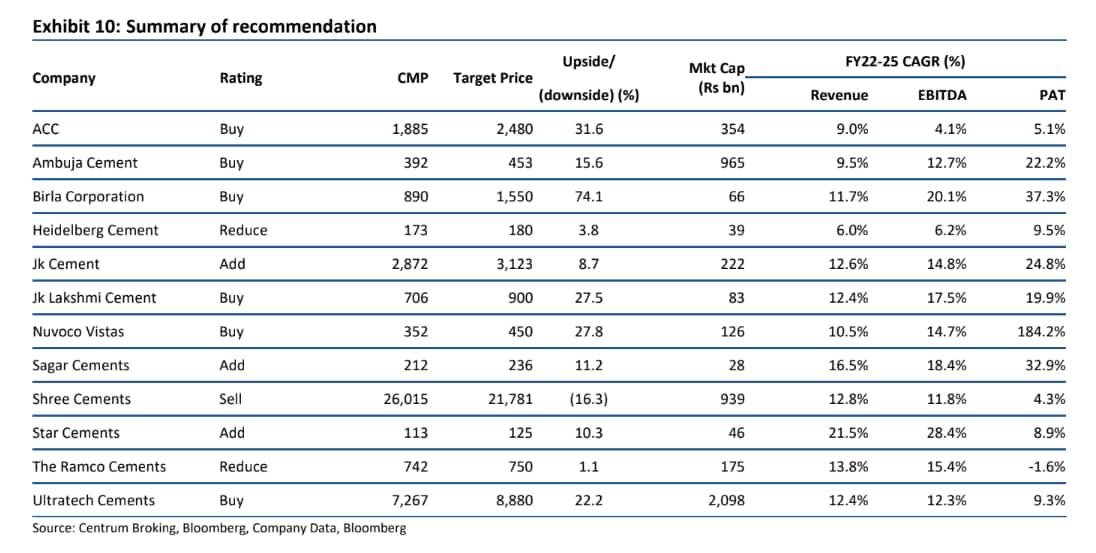

Given the weak base of FY23E, growth in revenue/EBITDA over FY23‐25E is likely to be better at 6 percent/26 percent, it further predicted. UltraTech Cement, Ambuja Cement, Birla Corp, Nuvoco Vistas, and JK Lakshmi Cement are Centrum's preferred picks in the sector.

Investment Rationale

Demand growth of 8 percent possible over FY22‐25E: The brokerage stated that the industry is expected to witness 7.8 percent demand CAGR over FY22‐25E given (1) Pent-up demand due to a weak base, (2) increased government spending in the pre‐election year and (3) revival of urban real estate sector. It believes that cement demand can grow at 8‐10 percent in FY23E and FY24E before normalizing back to less than 6 percent in FY25E. Multiple government schemes like PMAY and PMGSY will keep rural demand healthy whereas revival of urban real estate with a focus on the affordable housing segment is also likely to keep urban demand in good stead, it further said. Centrum expects the east and central regions to deliver better demand growth compared to the rest of the regions.

Concerns over excess supply overhyped: As per the brokerage, the industry is likely to add more than 100mn mt of capacity over FY22‐25E. While the quantum of capacity addition is definitely higher, the brokerage believes that demand is likely to keep pace with incremental supply and hence utilizations are expected to improve. “We are building in incremental demand of 90mn mt against an incremental supply of 87mn mt (weighted average). East and central regions are likely to witness the largest share in capacity addition whereas addition in north and west regions will be lowest,” it said.

Softening commodity prices to aid in normalization of margins: The brokerage noted that the cement industry benefitted from the benign cost environment over FY19‐21 and average operating costs for the sector in FY21 were around ₹3,800/mt. There has been more than ₹1,200/mt increase in operating costs for the sector over the past 1.5 years driven by power and fuel costs, especially coal and pet coke, it pointed out. However, it noted that recently, prices of crude and coal have seen a correction from peak levels coupled with a sizeable correction in pet coke prices. As a result, Centrum believes that operating costs for the sector have likely peaked in Q2FY23 and we will see a gradual correction in costs going forward.

Entry of Adani may lead to the long-awaited consolidation in the industry: In May 2022, Adani Group sealed one of the biggest M&A deals in the cement industry to acquire ACC and Ambuja from Holcim group to be 2nd largest player in the industry. Initially, there were concerns that an aggressive approach to increase market share is likely to result in increased competition and depressed margins for the industry. However, the brokerage believes that the group will follow a pragmatic and inorganic route for growth, resulting in increased market share without increasing supply and hence resulting in consolidation.

"We value cement stocks based on Sep’24 EV/EBITDA target multiples. To remove bias and judge the stocks based on merit, we have devised a valuation framework to identify correct target multiples for the stocks. We use long-term sector EV/EBITDA multiples as our starting point and then apply different weights for parameters like growth, return ratios, size and corporate governance to arrive at individual cement company’s fair valuation," explained the brokerage.