2022 was not a very exciting year for the consumer staples sector, with both the NSE and BSE consumer indices falling in double digits on the back of high inflation and rural slowdown. However, the companies still managed to report strong YoY growth, benefiting from a low base (Covid-19), pent-up demand and network expansion.

Consumer sector outlook 2023: Jefferies prefers Staples over Discretionary in 2023; lists top picks

TL;DR.

In this new year, global brokerage house Jefferies sees a pick-up in growth along with margin expansion for consumer staples even as discretionary and retail are likely to face growth moderation.

In this new year, global brokerage house Jefferies sees a pick-up in growth along with margin expansion for consumer staples even as discretionary and retail are likely to face growth moderation. Its top picks are HUL, Godrej Consumer, and Britannia, while it remains on the sidelines in most discretionary and retail names.

"We expect the rural economy to bottom out and see a recovery through CY23, led by factors like a better outlook for wages, crop margins, rising construction activity, and gov't spending, etc. On the other hand, urban demand could see a softening due to factors like a high base, slowing IT hiring, etc. The impact should be visible in segments like QSR, in our view," said the brokerage.

EBITDA

The brokerage further pointed out that consumer staples faced severe headwinds due to a sharp rise in input prices over the past few quarters - while the industry resorted to product price hikes, the gross margin contracted sharply, with 150 bps YoY Ebitda margin contraction in 1HFY23.

However, going ahead, Jefferies expects the impact of lower crude & palm oil prices to show up in coming quarters; further price hikes by food companies should offset agri price inflation and in turn drive up gross margins. A&P spending would also go up but the Ebitda margin should still see a YoY expansion, it added.

Urban demand

Regarding Urban demand, Jefferies noted that it has benefited from several tailwinds including strong hiring trends in several sectors (notably IT services and start-ups), the accumulation of savings due to COVID-19 restrictions on mobility, and pent-up demand in a few categories, which offset inflationary headwinds. However, for 2023, the brokerage is cautious on the demand outlook as the above-mentioned tailwinds wane.

In fact, net hiring by IT companies under Jefferies coverage has cooled off and is now lower than even pre-pandemic quarters. Further, active job openings in IT services have fallen by 53 percent from the peak to a 22-month low. A slowdown in start-up funding has driven job cuts in several cases, even as an increase in interest rates would lead to higher EMI outgo for households, it added.

Outlook

2023 is likely to be a year of a pick-up in earnings growth for consumer staples as inflationary headwinds start to moderate, predicted the brokerage. Key inputs such as crude oil and palm derivatives have corrected 20-40 percent from the peak, although benefit from this has been delayed due to high-cost inventory, it noted.

"While prices for several agri inputs remain firm, overall raw material inflation should moderate for most companies. This should drive 200bps GM expansion for our coverage, after a 500 bps contraction seen in the last four years. While this would be partly re-invested in ad spends, Ebitda margin should still see a modest expansion. Further, volume growth trajectory should also improve as the base should remain soft for most of 2023 along with a gradual rural recovery," it highlighted.

Put together, Jefferies expects an 18 percent EPS growth for consumer staples in FY24, the highest in nearly a decade.

Source: Jefferies

Segments

Paint: As per the brokerage, paint companies have faced severe margin headwinds for the last 18 months, due to inflation in crude oil derivatives and titanium dioxide. In the last few months, prices for both these inputs have corrected by 15-25 percent. This should allow paint companies to recoup margins and provide a tailwind to EPS growth in CY23, it said.

"While we build a volume growth slowdown for Asian Paints going forward, margin expansion should still drive over 15 percent EPS growth in 2HFY23 and FY24. However, competition is set to rise in the paint industry with the entry of Grasim," noted the brokerage.

Jewellery: Jewellery has shown the strongest growth trends across retail & discretionary categories in the last few quarters, with industry demand 60 percent higher than pre-Covid levels in value terms (volume too slightly higher pre-Covid), informed the brokerage. Value growth was supported by a rally in gold prices, along with strong discretionary consumption in urban India and pent-up demand from periods of Covid-19 lockdowns, it said. Apart from strong category tailwinds, organised players also benefited from accelerated network expansion, with market leader Titan tracking a 20 percent revenue and 30 percent Ebitda growth on a 3-Year CAGR basis in 9mCY22, Jefferies pointed out.

While Titan continues to see strong demand momentum in the near term, the brokerage remains cautious as tailwinds for urban discretionary consumption wane. It sees 16 percent growth in jewellery revenue in FY24, lower than the 20-22 percent 3Y CAGR that Titan is tracking currently. It expects margins to remain close to 13 percent, as Titan focuses on growth, especially in wedding jewellery. While Titan's overall EPS growth still remains healthy at 15 percent in FY24, the stock is priced to perfection and offers limited upside, forecasted the brokerage.

Retailers: As per the brokerage, brick-and-mortar multi-category retailers such as DMart and Reliance Retail made a comeback in CY22, as store operating hours normalized and COVID-19 restrictions subsided, further supported by steady network expansion. For DMart, recovery however was uneven on a revenue per store/ per sq. ft. basis. While per-store food and FMCG throughput largely normalised (inflation benefit), mass discretionary categories such as general merchandise (GM) and apparel lagged owing to acute inflationary pressure faced by consumers, it said. Jefferies sees scope for per-store revenue to move up higher in CY23, as GM & apparels recover, albeit in a gradual manner. This, along with continued network expansion should drive over 25 percent EPS CAGR in FY24. Ebitda growth nonetheless will remain at 20 percent levels and all eyes will be on the balance sheet, given the substantial cash burn seen in FY23, said the brokerage.

QSR: Jefferies noted that QSR players had a mixed-bag year in 2022. On one hand, network expansion remained strong, with most players delivering a 10-30 percent CAGR in store additions. The dine-in format also recovered this year, while the share of delivery normalized, it informed. Further, despite aggressive additions, per-store revenue remained at par or higher than pre-Covid levels across formats, partly due to inflation and consequent hikes in menu prices. On the other hand, higher prices of key raw materials have impacted gross margins and SSS growth on a 3Y Cagr basis was also muted in the Sept quarter, despite product price hikes indicating pressure on volumes, pointed out the brokerage. In 2023, it expects network expansion to remain strong although lower than the trends seen in the last two years. It sees downside risks to SSS growth and per-store revenue, given our concerns about urban discretionary consumption.

Prefers staples over discretionary

Consumer stocks largely saw moderate returns in CY22, albeit, there were some notable outliers — VBL (+95 percent), ITC (+52 percent), Trent (+39 percent) — which mainly benefited from opening up post-Covid. Devyani (+27 percent) and Britannia (+18 percent) also delivered well, as they outperformed peers on earnings growth.

"For staples, EPS downgrades were a key driver for muted returns, given weak volume growth and high input cost inflation. However, for discretionary stocks, EPS downgrades were actually limited to only Jubilant Foodworks, and stocks saw some de-rating (from unsustainable levels) after a strong run in 2021.

Going forward, we expect staples to see a pick-up in earnings growth in FY24 as input cost inflation moderates and volume growth recovers. We expect 18 percent EPS growth for our staples coverage (excl. ITC/ VBL) in FY24. Valuations for most staples are at a 5-year average and should sustain, as growth recovers," noted the brokerage.

On the other hand, there are concerns about a slowdown in discretionary & retail, especially after nearly two years of strong recovery and aggressive network expansion, it added. FY24 will also see EPS growth converging for staples and discretionary stocks, with downside risk to estimates in discretionary, predicted the brokerage. Discretionary stocks continue to trade at a premium to staples and also, their own history, and are prone to further de-rating in 2023 if growth moderates, explained the brokerage.

It prefers staple stocks over discretionary with a 12-Month view. "While we expect a recovery in rural growth and improvement in Ebitda margins to play out in staples in 2023, margin recovery should be a more dominant theme in the near term with rural uptick playing out gradually through the course of CY23. In the near term, we prefer plays that benefit the most as inflation subsides - this includes HUL, GCPL, and Britannia, which are our top picks. However, we also like Dabur and Colgate, given their higher rural skew. In discretionary, we remain selective and Devyani is the only BUY," said Jefferies.

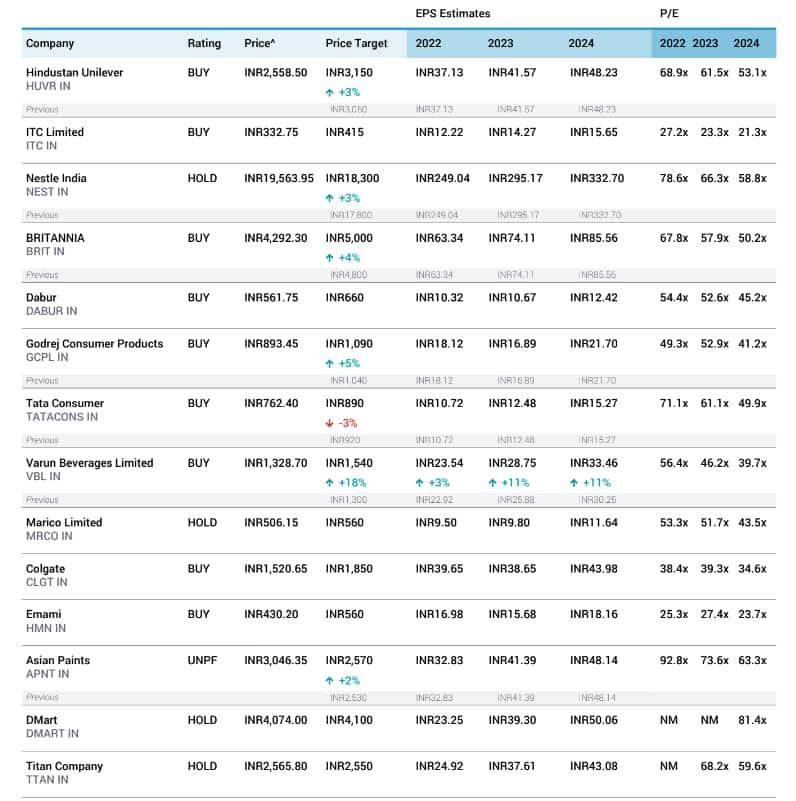

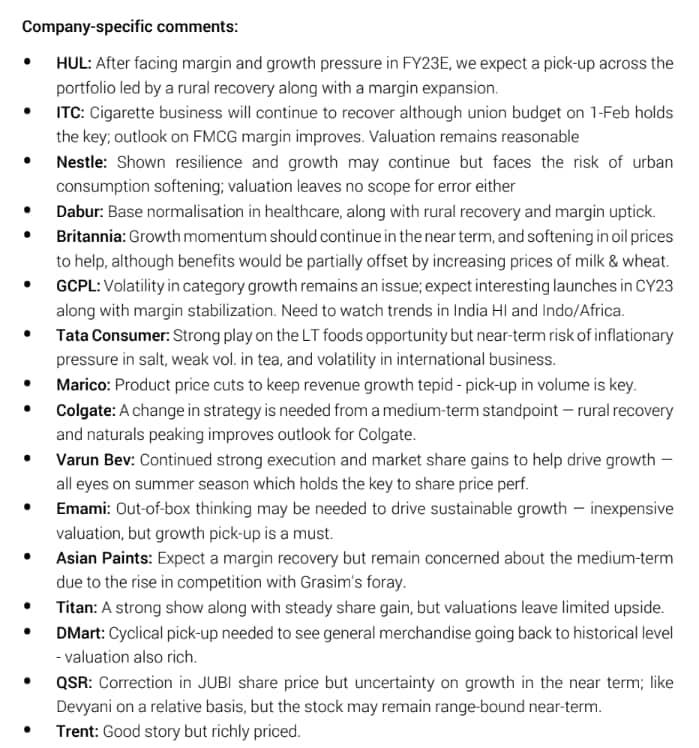

Here's what the brokerage has to say about each stock:

Source: Jefferies report

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

First Published: 09 Jan 2023, 08:00 AM IST