Domestic brokerage house Geojit Financial Services has assigned a ‘sell’ call to energy and environment solutions provider Thermax on the back of premium valuation and moderation in high-value orders.

It has given a price target of ₹1,806 per share, implying a potential downside of 13 percent.

The stock has risen 15 percent in the last year and around 6 percent in 2023 YTD. However, it fell 11 percent between November and January.

The stock has given exemplary returns in the long term. It has surged over 4,500 percent in the last 10 years and around 100 percent in the last 5 years.

"We expect execution to pick up in the coming quarters due to a healthy order book, softening commodity prices, and easing supply chain issues. However, the current expensive valuation and expectation of moderation in high-value orders remain a concern. We, therefore, assign SELL rating with a TP of Rs. 1,806 based on a P/E of 28x on FY25E EPS," said the brokerage.

Thermax Ltd (TMX) offers integrated, innovative solutions in the areas of heating, cooling, power, water & waste management, air pollution control and chemicals.

In the December quarter, the company reported a net profit of ₹126 crore, up 59 percent YoY versus ₹79 crore reported in the same quarter last year.

Its revenue also witnessed a strong growth of 27 percent YoY to ₹2,049 crore as against ₹1,615 crore in the year-ago period. This was led by superior execution in the energy (27 percent YoY), and environment (29 percent YoY), while chemical segments registered a muted growth.

Stabilisation in input price and freight costs also led to an 86 bps YoY improvement in EBITDA margin to 7.9 percent during the quarter.

Its 9-month order book also reported a jump of 33 percent YoY, however, order inflows declined by 10 percent YoY during the quarter.

The brokerage highlighted that the management has said, "We could witness moderation in revenue due to the absence of high-value orders in the order book which could be offset by multiple short cycle orders in the range of ₹300 crore to ₹1,000 crore traction in orders from cement, fertiliser, sugar/distillery, metals and refinery & petrochemicals."

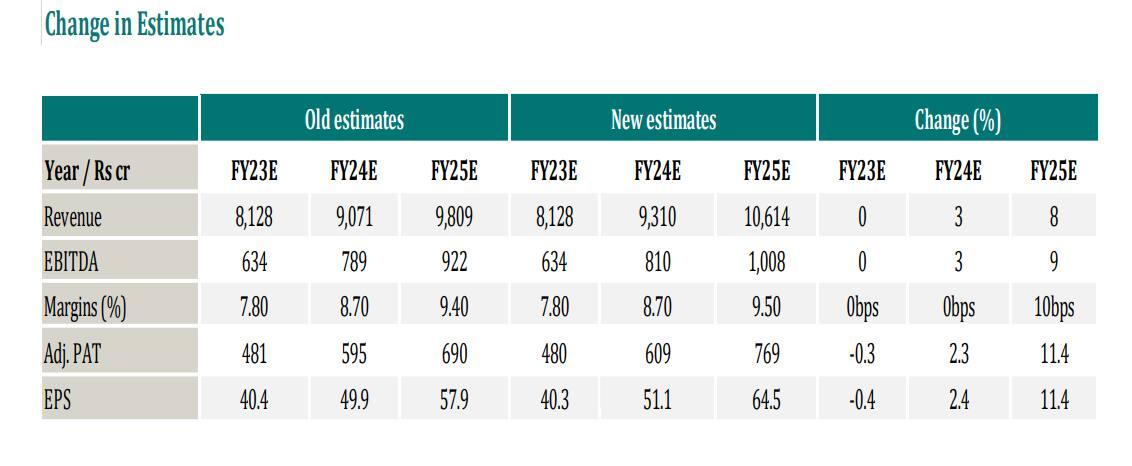

The brokerage has maintained its FY23E revenue estimate while increasing the FY24/FY25 revenue estimate by 3 percent/8 percent, respectively, due to the strong order book pipeline and pick-up in execution. It also expects margins to improve in coming quarters due to the softening of commodity prices.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.