Maintaining its upward trend, shares of Gujarat Fluorochemicals hit an all-time high on the BSE in Tuesday's trade. Following the company's strong first-quarter results, the stock continues to set new highs week after week. The stock also piqued the interest of institutional investors with its one-year performance.

In Tuesday's trading session, the stock opened with a gap up of ₹41.8 per share, at ₹4,021, and rose further, reaching a new all-time high of ₹4,048.70 on the BSE. At the current levels, the stock is trading 133.48% above its 52-week low of ₹1,708, recorded on October 25, 2021.

In the last one-year period, Gujarat Fluorochemicals' share price has surged from ₹2,089 to the current level of ₹3,990, climbing by almost 91 percent. Further, over the last three years, the market price of the stock has zoomed by 465 per cent.

Gujarat Fluorochemicals Limited (GFL) is a part of the INOXGFL Group. The company is a leading producer of fluoropolymers, fluorospecialities, refrigerants, and chemicals for applications in various industries. The company caters to both domestic and international markets, its website shows.

The company's net profit has been steadily increasing over the last few quarters. After posting a net loss of ₹480.4 crore in the December 2020 quarter, the company quickly turned to a net profit the following quarter, posting ₹112.8 crore, and the company's net profits have grown steadily quarter after quarter since March 2021.

In the recent quarter that ended in June, the company posted a two-fold jump in its net profit to ₹306.3 crore as against ₹206.3 crore in the same quarter of the previous fiscal. In the June quarter, the company reported the highest revenue to date, at Rs. 1,360.2 crore.

Further, the company’s EBITDA grew almost two-fold to ₹458.9 crore in Q1FY23 as against ₹255.1 crore in the corresponding quarter of last year. Similarly, GFL's EBITDA margin increased by 34.40% year on year, from 27.98%, expanding by almost 642 bps, which is the highest to date.

While the company grew its EBIT margin by 26.60% and net profit margin by 19.62% in FY22, it also had a return on equity of 18.23% and a ROCE of 22.60% in FY22.

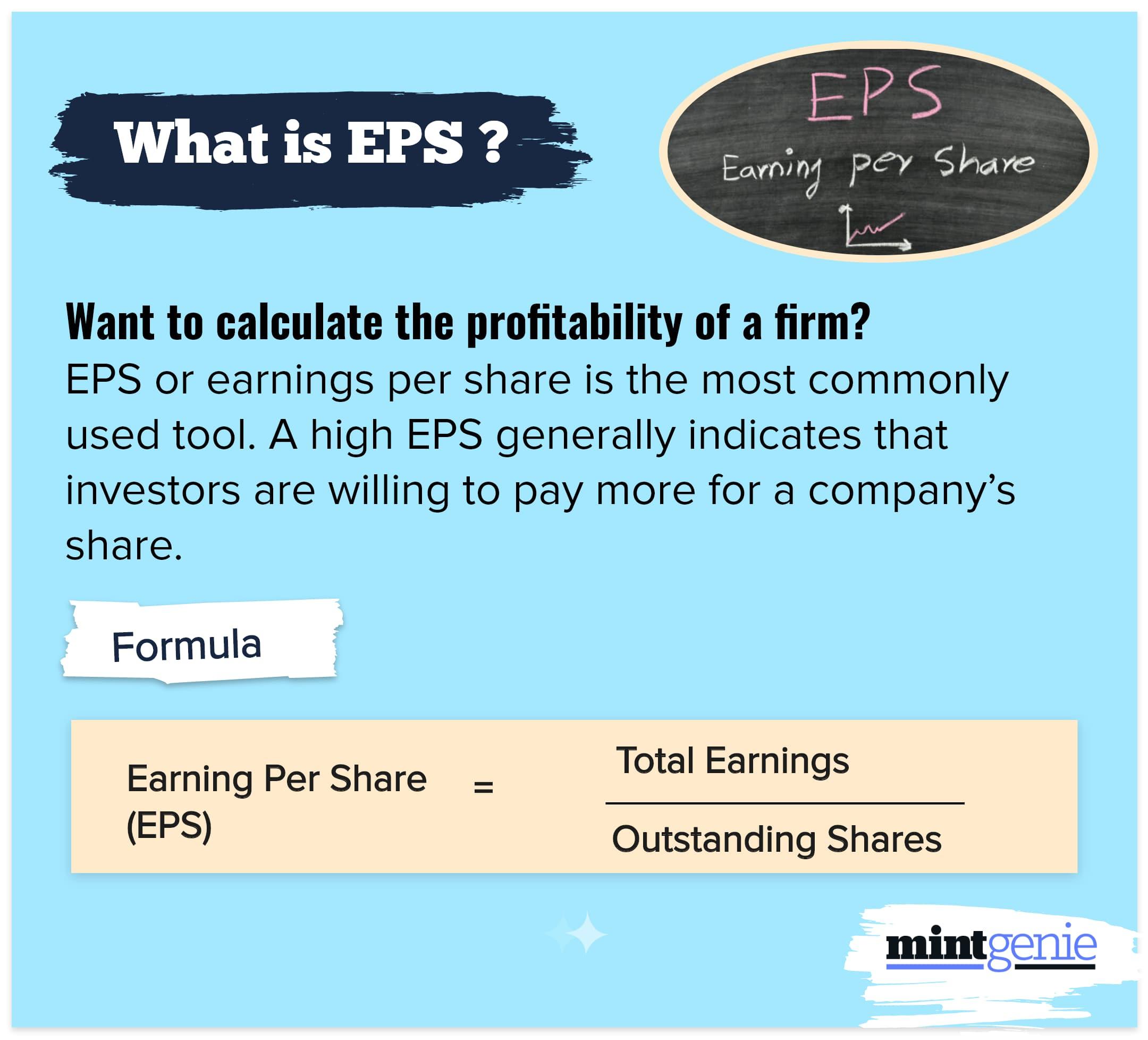

Despite such strong gains in the last one year period, domestic brokerage firm ICICI Securities is still bullish on the stock and has given a 'buy' call with a target price of ₹4,270/share. The brokerage firm has raised its EPS estimates by 2–10% over FY23E–24E.

GFL is close to completing the integrated battery chemicals complex at Dahej. The plant is intended for the production of LiPF6, the most popular electrolyte salt for lithium-ion batteries, with an initial capacity of 1,800 tpa to be expanded in two equal phases, said the brokerage.

The company will send samples for certification and customer verification. It also plans to subsequently produce electrolyte solutions for use by battery OEMs and is targeted at the Indian market. Electrolyte salt will be marketed in India, Europe, and the US. One GWh of battery needs 120te of electrolyte salt and 1,000te of electrolyte solution.

"Post FY25, GFL expects significant opportunities from battery chemicals, for which it is planning to commercialise the first plant in the next two quarters. According to the note, GFL is well placed to increase its revenues on the back of its significant exposure to new-age industries such as batteries, solar and green hydrogen. "It aspires to double revenue in the next three years and maintain an EBITDA margin of at least 30-35%," ICICI securities said in a note.

The company is planning to put up a blending facility for R-410a in the Middle East immediately. This can help secure consumption quotes for the regional market for HFCs. GFL also plans for a few fluoropolymer capacities such as PPA and FKM, which find application in films. The blending plant is likely to be commercialized by FY23-end, and the company plans to buy R-32 from the market until its own facility is commissioned.

GFL in its earnings presentation disclosed a capex of Rs11.5bn for FY23, but it expects some frontloading capex for fluoropolymers during the year, so capex can jump to Rs15bn. FY24 Capex also includes investment in the aforementioned integrated battery chemicals plant, said the brokerage.

The brokerage firm, however, highlighted some key risks, including a slower than expected ramp-up in capacity utilization, a faster than expected drop in prices, completion of the HFC project before the capacity addition freeze kicks in, and success in battery chemicals.

FIIs now favour buying the stock. They increased their stake from 2.2 percent in the June 2021 quarter to 4.1 percent in the June 2022 quarter. Promoters held 66.1% of the company, and retail shareholders held 25.6%. In contrast, mutual funds owned 4.3% of GFL.

An average of 6 analysts polled by MintGenie have a 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.