IT major HCL Technologies reported in-line earnings for the March quarter of FY23 (Q4FY23). The company's net profit rose 10.6 percent year-on-year (YoY) to ₹3,981 crore in the March quarter as against ₹3,599 crore in the year-ago period.

HCL Tech Review: Earnings positively surprise in Q4 but brokerages remain mixed on the stock

TL;DR.

While there have been no downgrades, some brokerages have retained ‘buy’ calls with positive upside predictions while others forecast some downside in the next 1 year.

Its revenue from operations for the quarter came in at ₹26,606 crore, up 17.74 percent from ₹22,597 crore in the same period last year. Constant currency (CC) revenue was down 1.2 percent quarter-on-quarter (QoQ) and up 10.5 percent on-year. Meanwhile, its US dollar revenue came in at $3,235 million, up 8.1 percent YoY.

"Our pipeline is near an all-time high, which reflects our differentiated business mix and strong client demand for our offerings. We have added 3,674 employees this quarter and overall employee strength has now grown beyond 225000. All these set us well in FY24 for a healthy revenue growth in the 6-8 percent range with operating margins in the 18-19 percent range,” said C Vijay Kumar, CEO & MD, HCL Tech.

After IT major TCS and Infosys' Q4 earnings missed Street estimates, investors were expecting another disappointment from HCL tech. However, the company surprised the Street with in-line results for the March quarter.

However, despite good Q4 results, brokerages remained mixed on the stock. While there have been no downgrades, some brokerages have retained ‘buy’ calls with positive upside predictions while others forecast some downside in the next 1 year.

Here's what brokerages have to say:

IDBI Capital

The brokerage has a ‘hold’ call on the stock with a target price of ₹1,010, indicating a potential downside of 3 percent.

"HCL Technologies reported 15.8 percent cc organic growth in FY23E led by market share gains. The company’s Q4 IT services revenues were also healthy led by the ramp of mega deals won. Going forward the company has guided FY24E revenue growth of 6-8 percent YoY and EBIT margins of 18-19 percent for FY24E. We expect the company to be at the lower end of the guidance mainly led by lower annual contract value (ACV) growth (up 4.3 percent YoY vs 21 percent YoY in FY22). Further, we expect ramp-downs in projects, delay in renewals and lower discretionary spending to further impact revenue growth. In addition, due to headwinds like wage hikes and a lower ability to manage cost in uncertainty we have assumed margins at the lower end of guidance (18 percent). Consequently, we have lowered our EPS estimates by 1.7 percent and 1.6 percent for FY23E & FY24E," predicted the brokerage.

Nirmal Bang

The brokerage has retained its 'sell' call on the stock with a target price of ₹930, indicating a downside of 16 percent. HCL Technologies delivered CC QoQ revenue decline of 1.2 percent, which was below expectation of 1.5 percent growth but in line with Street estimates and did not shock like the results of Infosys, stated the brokerage.

Nirmal Bang believes that the flat pricing assumption for FY24 will be challenged as HCLT has already indicated that some clients have asked for price cuts. While both Infosys as well as TCS have indicated weakness in the BFSI space, especially in North America in 4QFY24, HCLT had a strong quarter with a QoQ growth of 6.9 percent due to ramp-up of large deals won in the previous quarters, noted the brokerage. "The sense we get from HCLT commentary is that the worst on the macro front is over, which is contrary to our belief. We, therefore, assume a slightly lower than the guidance revenue growth for FY24 largely due to the view that the pricing trend will turn for the worse in 2HFY24," said the brokerage.

In the very near term, the stock may react positively to the better-than-feared results. However, it remains concerned about likely pressures emerging in H2FY24, it stated.

Religare Broking

The brokerage has maintained its ‘buy’ call on the stock with a target price of ₹1,333, indicating an upside of over 28 percent.

"For the near term, challenging macro and delay in deals may impact growth. However HCL Tech is better placed than its peers in the medium to long term because of lower attrition as compared to peers, its large deals momentum in the service business and new projects from Europe region will aid growth. The company is well diversified across its portfolio and has a balance of cost optimization and vendor consolidation products which help clients to choose according to its requirement. Besides, its strong deal across geography, verticals and offerings as well as improving utilization and cost measures will aid margin improvement going ahead. We have estimated its revenue/EBIT growth in INR terms to grow at a CAGR of 11.8 percent/15.3 percent over FY23-25E. Further, HCL is trading at a comfortable valuation," it said.

Kotak Institutional Equities

The brokerage has retained its ‘buy’ call on the stock with a target price of ₹1,225, indicating an upside of 18 percent.

“As per the brokerage, HCLT’s 4QFY23 results were ahead of our estimate led by surprise in the products segment, even as IT services disappointed. FY2024E revenue growth guidance of 6-8 percent is ahead of our estimate but seems aggressive at the upper end, noting weak deal wins. Kotak maintains revenue estimates and EPS estimates. A more balanced portfolio mix with momentum in apps and decent positioning in vendor consolidation and cost take-out mandates can offset vulnerability in ERD and products portfolios, and can drive peer-matching growth,” it explained.

Its FY2024E revenue growth estimate stands at 6.3 percent and EBIT margin at 18.5 percent.

Reliance Securities

The brokerage has a ‘buy’ call on the stock with a target price of ₹1,160, indicating a potential upside of 12 percent.

The brokerage expects HCLT to report a decent revenue driven by transformational and cost optimisational deal wins, ramp-up in recently won new large deals and commencement of new projects. Post the recent stock price corrections, stock valuation is attractive, which coupled with better 4Q performance than peers support positive view, it noted. It also believes that HCLT’s revenue growth momentum would continue at a better pace than peers.

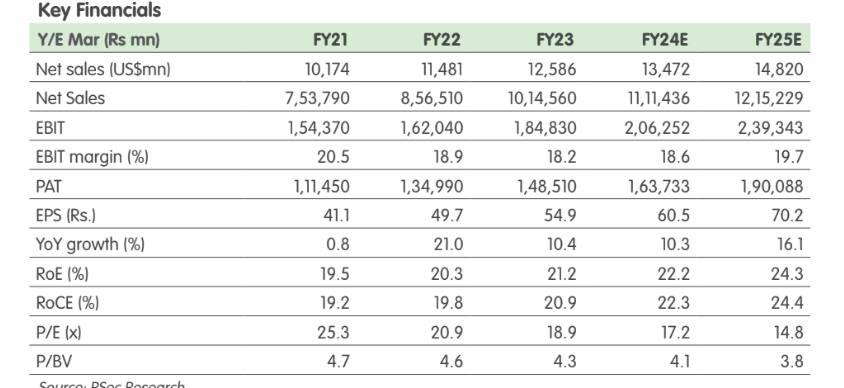

It estimates an FY24E/FY25E EBIT margin of 18.6 percent/19.7 percent. It expects the company’s revenue/EBIT/PAT to clock 9 percent/14 percent/13 percent CAGR over FY23-FY25E. Current valuation captures the negative impact of the ongoing global slowdown and likely impact on IT services, making risk-reward favourable, it said.

Source: Reliance Securities

First Published: 21 Apr 2023, 02:36 PM IST