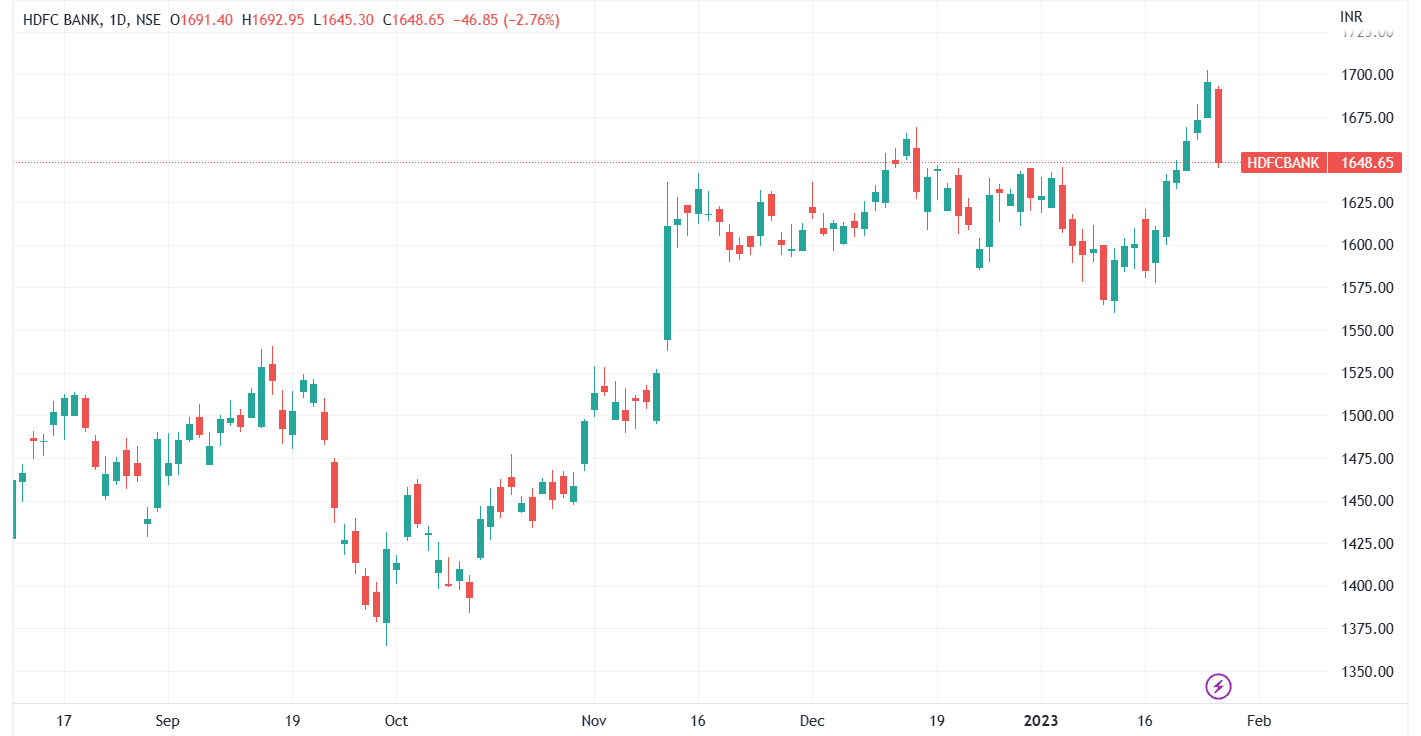

Shares of HDFC Bank, the country's largest private sector lender, fell sharply in Wednesday's trade after rallying for the last six trading sessions. The stock slipped 2.96 percent to hit an intraday low of ₹1,645 in today's trading session before finishing the day at ₹1,648.65, down 2.76 percent.

The stock began its bull run on January 17 after investors reacted positively to the bank's December quarter results. The stock rose nearly 7 percent over the next five trading days and at current levels, it is just 4.25 percent away from its 52-week high of Rs. 1,722, which it attained on April 04, 2022.

HDFC Bank's shares have increased by more than 18 percent in the last six months. Over the last one-year period, the market price of the stock has gained 12.84 percent.

The stock has soared 10.07 percent in CY22, underperforming the Nifty Bank by 11.08 percent, which rose 21.15 percent during the same period.

For the December quarter, the bank reported a 19.9 percent jump in the net profit to ₹12,698 crore, on the back of low provisions and the expansion in net interest margins. The bank had posted a net profit of ₹10,605.78 crore in the preceding quarter.

Total income on a standalone basis rose to ₹51,207.61 crore in the October-December quarter of FY23, as against ₹40,651.60 crore in the same period of the previous financial year.

The bank's net interest income surged 24.6 percent to ₹22,987.8 crore and the net interest margin came in at 4.1 percent of total assets.

The gross NPA ratio of the bank fell to 1.23 percent in Q3 FY23 as against 1.26 percent in Q3 FY22, while the net NPA stood at 0.33 percent in Q3 as against 0.37 percent in the same quarter last year.

Following the release of the third quarter earnings, brokerage firm Axis Securities said it continues to like the bank from a long-term perspective due to its strong franchise, consistent performance delivery across business cycles, and potential to generate a robust RoA and RoE of 2 percent and 17–18 percent, respectively.

The brokerage has raised its target price to ₹1,860 apiece from ₹1,800 earlier. "HDFC Bank continues to expand its geographical footprint aggressively, which should steer strong new customer additions and thereby enable robust business growth for the bank," said Axis Securities.

Similarly, IDBI Capital also remains positive about the stock and has retained its "buy" tag by raising the target price to ₹2,070 per share from ₹1,860.

"We remain structurally positive on HDFCB given its superior credit underwriting, structurally better NIM, and the ability to maintain a higher RoA among its peers," said the brokerage.

ICICI Securities said that the earnings of the HDFC bank were in line with their estimates. The brokerage remained optimistic about the stock and maintained a "buy" call with an unchanged target price of ₹1,874 apiece.

The regulatory costs associated with the HDFC merger and elevated opex will be a significant downside for the stock, according to ICICI Securities.

38 analysts polled by MintGenie on average have a 'strong buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.