Housing Development Finance Corporation (HDFC) is consolidating its financial business as the firm on April 4 announced that it will merge its operations along with HDFC Investments Limited and HDFC Holdings Limited into HDFC Bank.

"Housing Development Finance Corporation Limited (Corporation) at its meeting held on April 4, 2022, has approved a composite scheme of amalgamation for the amalgamation of (i) HDFC Investments Limited and HDFC Holdings Limited, with and into the Corporation and (ii) the Corporation with and into HDFC Bank Limited," the housing finance company said in a BSE filing on April 4.

The proposed merger is subject to regulatory approvals from the Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), the Competition Commission of India, the National Housing Bank (NHB), the Insurance and Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, the National Company Law Tribunal, stock exchanges and other statutory and regulatory authorities, along with the respective shareholders and creditors.

"Post the combination, HDFC Bank’s customers will be offered mortgages as a core product in a seamless manner. HDFC Bank will also leverage the long tenor mortgage relationship to offer varied credit and deposit products enabled through better insights throughout the customer life-cycle. This will result in an enhanced value proposition and customer experience for all customers of the combined entity," HDFC said.

HDFC is India’s premier housing finance company while HDFC Bank is one of the largest private sector banks of the country, with more than 68 million customers and 6,342 branches.

Key highlights of the proposed merger

- The share exchange ratio for the amalgamation of HDFC with HDFC Bank shall be 42 fully paid-up shares of the face value of ₹1 each of HDFC Bank for every 25 fully paid-up shares of the face value of ₹2 each of HDFC.

- This means if you have 25 shares of HDFC of the face value of ₹2 each, you will get 42 shares of HDFC Bank of the face value of ₹1 each after the merger.

- Subsidiary and associates of HDFC will become subsidiaries and associates of HDFC Bank now. HDFC Bank will be 100 percent owned by public shareholders and existing shareholders of HDFC Limited will own 41 percent of HDFC Bank.

- The merger is expected to be achieved within 18 months, subject to the completion of regulatory approvals and other customary closing conditions. The company expects the merger to be completed by the second or third quarter of FY24.

- In the next four months, the company will seek regulatory approvals, then in the next 12-14 months, it aims to complete other formalities such as filing of scheme and NCLT, creditors and other approvals. After all these, the company will complete the ROC filing and allotment of shares.

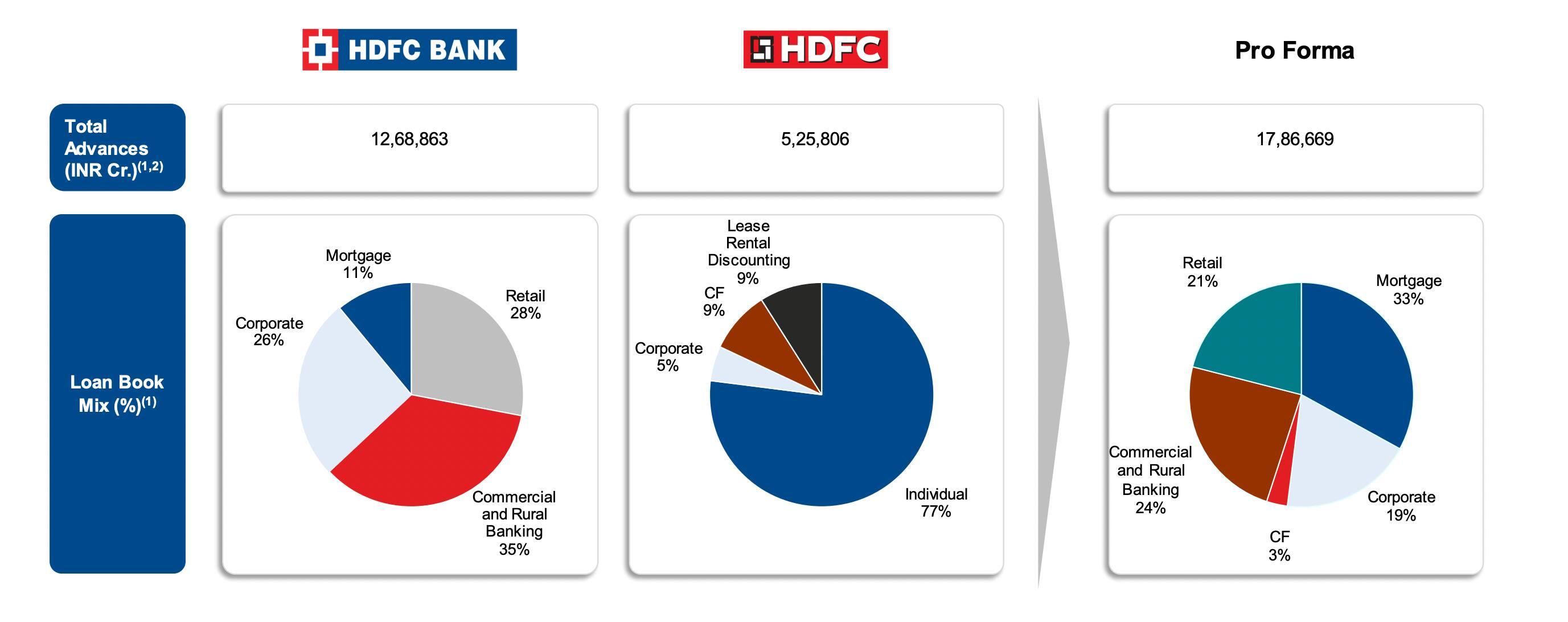

Total Size

HDFC, which is India’s largest housing finance company with a total asset under management (AUM) of ₹5.26 lakh crore and a market cap (m-cap) of ₹4.44 lakh crore will merge into HDFC Bank, India's largest private sector bank by assets with a market cap of nearly ₹8.35 lakh crore.

Cumulatively, their market cap will top ₹12 lakh crore which will make HDFC Bank the third company in India with more than ₹10 lakh crore m-cap, after Reliance Industries and TCS (as on April 1, 2022 m-cap). HDFC Bank currently is the third-largest company in India in terms of m-cap. On April 1, its m-cap was ₹8.35 lakh crore.

As per HDFC filing, it had total assets of ₹6,23,420.03 crore, turnover of ₹35,681.74 crore and net worth of ₹1,15,400.48 crore as on December 31, 2021.

On the other hand, HDFC Bank has total assets of ₹19,38,285.95 crore, turnover of ₹1,16,177.23 crore (includes other income) and net worth of ₹2,23,394 crore, as on December 31, 2021.

Management Speak

“This is a merger of equals. We believe that the housing finance business is poised to grow in leaps and bounds due to the implementation of RERA, infrastructure status to the housing sector, government initiatives like affordable housing for all, amongst others," said Deepak Parekh, Chairman HDFC Limited.

"Over the last few years, various regulations for banks and NBFCs have been harmonised, thereby enabling the potential merger. Further, the resulting larger balance sheet would allow underwriting of large ticket infrastructure loans, accelerate the pace of credit growth in the economy, boost affordable housing and increase the quantum of credit to the priority sector, including credit to the agriculture sector," Parekh added, highlighting the rationale behind the merger.

As per HDFC BSE filing, Credit Suisse, Kotak Securities, Jefferies, Arpwood, Motilal, Axis, JM Financial, IIFL and Ambit, acted as financial advisors to HDFC Limited while JP Morgan, Goldman Sachs, Citi, Nomura CLSA, BNP, HSBC, ICICI Securities and Edelweiss acted as financial advisors to HDFC Bank.

"This transaction helps in realizing the potential of what HDFC’s housing finance business can achieve by leveraging the distribution and customer base of HDFC Bank. It is a step in the right direction, taken at the right time, for value creation for all the stakeholders," said Keki M. Mistry, Vice-Chairman and CEO of HDFC.

Sashi Jagdishan, CEO & MD, HDFC Bank said that the proposed transaction was value accretive and ticks all the right boxes.

"It ticks all the right boxes in terms of completion of product offerings, product leadership in home loans as with other retail assets products, distribution strength across the country and a customer base that can be leveraged to cross-sell a complete suite of financial products. It is value accretive for all the stakeholders of both the organisations, including shareholders, employees and customers," Jagdishan said.