_1641277474905_1671700203888_1671700203888.jpg&w=3840&q=75)

The year 2022 was marked by multiple headwinds for the market. While the market remained volatile due to geopolitical tensions, rate hikes and slowing economic growth, there were pockets of opportunities.

The key lesson in 2022 was that even amid the gloom, there are stocks that can give stellar returns.

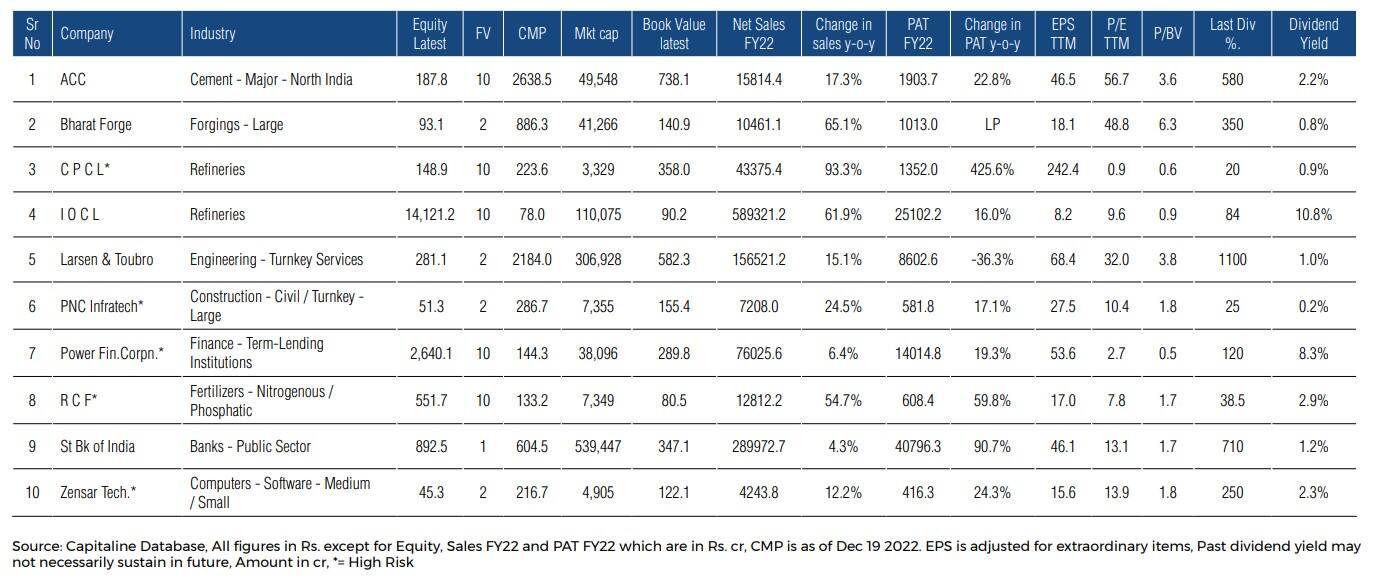

While uncertainty is expected to remain the theme for the market for a significant part of 2023, there will certainly be stock opportunities. Brokerage firm HDFC Securities recommends the following 10 stocks to buy for the new year. Have a look:

Adani’s buyout of ACC can be a catalyst for cost-saving opportunities, better procurement, logistics and brownfield expansions — which could drive earnings growth faster than peers.

The growth plans and cost-saving strategies by the new management will be the key trigger for stock performance.

The upcoming expansion in the central market will boost its volume growth visibility from FY24 onwards. ACC is also increasing its green power and fuel mix to mitigate the impact of rising fuel costs.

ACC will commission a 2.7/1mnMT clinker/cement integrated unit in Ametha, MP, in Mar-23. Its 2.2mn MT grinding unit in UP will get commissioned in FY24E. These will expand its cement capacity to 39mn MT. WHRS at Jamul and Kymore are partially commenced in Q3CY22.

Post installation of WHRS in Jamul, Kymore and Ametha (combined capacity of 39 MW), the green power share will rise to 15 percent.

Volatility in input costs is a concern for ACC. Moreover, cyclicality in the cement sector is also a concern.

ACC remains exposed to demand and pricing dynamics in the cement industry, which is influenced by the cyclical economic trends and capacity additions by the players in the respective regions during such periods. When the capacity additions exceed the incremental demand, the prices and consequently, the profitability of the players get impacted.

Bharat Forge (BFL) is a leading player in the forgings industry. The company operates in several sectors including automobile, power, oil and gas, rail & marine, aerospace & defence, construction, mining, etc.

Its forging business is benefitting from China+1 and EU+1 strategy globally. The government’s initiative to enhance local manufacturing through the PLI schemes and mission of ‘Atmanirbhar Bharat’ is boosting prospects for the company. BFL has already announced a capex of ₹240 crore in the next few years to utilise opportunities in defense and e-mobility areas.

BFL has bagged ₹178 crore order from the defence ministry to manufacture Kalyani M4 vehicles and expects further orders going forward. In aerospace, the company has already set the target to reach ₹1,000 crore by FY23 from the current ₹400 crore.

Demand cyclicality in automobiles, a slowdown in the US and Europe, and volatile raw material prices are the key concerns.

Chennai Petroleum Corporation (CPCL) is one of the leading PSU refining companies, with a current refining capacity of 10.5 million tonne per annum (mtpa) at Manali.

The company produces petroleum products, lubricants, and additives. CPCL also provides high-quality feedstock such as propylene, superior kerosene, butylenes, naphtha, paraffin wax, and sulphur to other industries.

Refining fundamentals remain robust. CPCL’s average gross refining margin (GRM) in the first half of FY23 (H1FY23) stood at $14.58 per bbl versus $5.75 per bbl in H1FY22 and GRM was at $4.44 per bbl in Q2FY23 versus $5.83 per bbl in Q2FY22.

The brokerage firm expects that GRM could be flat to slightly up quarter-on-quarter (QoQ) in Q3FY23.

Economic slowdown, volatility in oil and gas prices, fall in gross refining margin (GRM) and regulatory changes in the oil and gas industry could impact its growth story in the future. The changing macroeconomic scenario can have an impact on the growth plans of the company.

Indian Oil Corporation (IOCL) through a JV with CPCL is also setting up a 9-mmtpa refinery at Cauvery Basin, Nagapattinam, at an estimated project cost of ₹31,580 crore, wherein IOCL and CPCL will together hold a 50 percent stake (i.e. 25 percent each in the JV), while the remaining 50 percent is to be held by other investors.

Economic slowdown, volatility in oil and gas prices and regulatory changes in the oil and gas industry could impact its growth story in the future.

The company’s profitability is also exposed to the forex rates (INR-US$) given the business is largely depending on the volatility of the rupee against the dollar on sales, crude procurement and foreign currency loans. Marketing margins are impacted because of the low freedom to reprice auto fuels.

L&T is India’s premier engineering giant with decades of experience in the engineering and construction sector. It is well poised to be the key beneficiary of capex upcycle driven by investments in both public and private sectors.

L&T is targeting to reduce debt by ₹5,000 crore over the next two-three years led by receipt of an interest-free loan of ₹3,000 crore from the Telangana government and monetization of ToD rights of ₹2,000-2,500 crore.

L&T expects the bid-to-award ratio to further improve in H2FY23 to over 55 percent which would drive the order inflows.

The company is engaged in large turnkey time-barred projects. Thus, the timely execution of layout is an important factor.

Further, a significant rise in commodity prices due to a shortage of inputs materials and global supply chain disruptions may affect the stage of execution and margins of the company. Dependence on the economic situation in the Gulf and GoI’s infra spending remains key monitorable.

The current order book of the company as on Sept’22 stands over ₹19,200 crores which give the company a robust revenue visibility over the next two-three years. The executable order book excluding new HAM-awarded projects stands at 2 times FY22 revenue.

The government’s plan to expand the national highway network by 25,000 Km in the current fiscal year is supported by this massive increase in budget. The allocation by MORTH grew by ₹80,000 crore from about ₹1.11 lakh crore to ₹1.9 lakh crore, representing a 70 percent year-on-year (YoY) growth.

The company is engaged in large turnkey time-barred projects. Thus, the timely execution of the project layout is an important factor.

The order book under execution is approximately ₹19,000 crore, the majority of which constitutes of government orders from water and HAM road projects, thus also facing the risk of delay in receivables.

Power Finance Corporation (PFC) is the largest government-owned NBFC that provides funding to the Indian power sector. In FY22, the company was conferred ‘Maharatna’ status by the Government of India, the highest recognition for a public sector company. In Mar-19, PFC acquired GoI’s 52.63 percent paid-up share capital in Rural Electrification Corporation (REC).

A higher-than-expected deterioration in the asset quality could result in the erosion of the Tier I capital. Fresh formation of bad loans could keep provisioning high and return ratios compressed for a longer time.

Further, any delay in the recovery, higher than expected haircuts or a sharp rise in the slippage could impact the profitability and business growth prospects. This could also impact its ability to payout large dividends.

Rashtriya Chemicals and Fertilizers

Rashtriya Chemicals and Fertilizers (RCF) is a leading fertilizers and chemicals manufacturing company with 75 percent of its equity held by the Government of India.

RCF (31.85 percent share), along with Coal India, GAIL and FCIL is setting up a coal gasification-based fertilizer complex, comprising of 2200 MTPD Ammonia plant and 3850 MTPD Urea plant at FCIL, Talcher, Odisha.

The unit will have an output of 1.27 MMTPA of ‘Neem’ coated prilled urea and is expected to be completed by September 2024.

Industrial Products Division has achieved the highest-ever sales turnover of ₹2,265 crore during FY22 versus ₹1,023 crore during FY21, up 113 percent.

For H1FY23, revenue amounted to ₹1,739 crore versus ₹995 crore in H1FY22. RCF also intends to set up a new AN Melt plant of 425 MTPD at RCF Trombay unit with cost of ₹187 crore and a payback period of three-four years.

Indian banking industry has seen a healthy recovery in terms of both loan growth and improvement in asset quality.

The loan book quality now seems healthier as the majority of the back book clean-up has been done and recovery pace has accelerated.

Bank lending has been growing at double-digit rates as of this fiscal. Revival in consumer demand and a rise in private capex followed by a rise in government spending can be triggers for the growth. SBI, being a leader in the industry, could be the best play on this theme.

A higher-than-expected deterioration in the asset quality, low credit growth, fall in NIMs due to a scramble for deposits, weak performance of the subsidiaries and high MTM loss due to rising yields could impact the profitability of the bank.

Zensar is a mid-size IT software and infrastructure services and solutions provider with industry expertise across manufacturing (Hitech and Industrial), retail, insurance, banking and financial services.

Zensar witnessed an increase in multi-service line deal wins in Q2FY23. Advanced engineering services grew 7.4 percent QoQ and data engineering services grew 16.8 percent QoQ led by multiple wins in cloud migration, cloud modernisation and enterprise transformation.

Deal wins in Q2FY23 stood at US$142mn, up 13.4 percent QoQ and down 24.4 percent YoY, with a healthy mix of new wins and renewals. A healthy order book and favourable industry demand outlook provide revenue visibility going forward.

Rupee appreciation against the dollar, macro uncertainty in US and Europe, higher attrition rate, margin contraction, visa cost and strict immigration norms are key concerns.

Disclaimer: The views and recommendations given in this article are those of the broking firm. These do not represent the views of MintGenie.