HDFC Bank on Monday said its board has approved the amalgamation of HDFC Investments and HDFC Holdings with HDFC and that of HDFC into HDFC Bank

HDFC to be merged with HDFC Bank: What does this mean for investors

TL;DR.

The merger will create a large balance sheet of ₹25.61 lakh crore, which is now closer to the country’s largest bank — the State Bank of India with ₹45.34 lakh crore. The HDFC Bank was already the country’s second-largest bank. ICICI Bank has a balance sheet size of ₹17.74 lakh crore as of March 31, 2021.

The HDFC-HDFC Bank merger is expected to be completed by the second or third quarter of FY24. After the merger, HDFC Bank will be 100 per cent owned by public shareholders and existing shareholders of HDFC Limited will own 41 per cent of HDFC Bank.

Shares of HDFC Bank and HDFC jumped 10 per cent each in early trade after the entities announced the merger. HDFC Bank shares were up 9.99 per cent at ₹1,656.90 on BSE while shares of mortgage lender HDFC gained 10 per cent to trade at ₹2,696.

Area of business

The HDFC Corporation is a deposit-taking housing finance entity(ies); company registered with the NHB and its shares are listed on the Stock Exchanges.

HDFC Bank is a banking company licensed by the RBI under the provisions of the Banking Regulation Act, 1949. Its shares and American Depositary Receipts are listed on the Stock Exchanges and New York Stock Exchange respectively.

HDFC investments limited and HDFC holdings limited are non-deposit, accepting non-banking finance companies, registered with RBI, engaged in the business of investments in stocks, shares, dentures and other securities. Both are unlisted Companies.

What this means for investors

The amalgamation of HDFC into HDFC Bank will create the third-largest entity in India in terms of market capitalisation ( ₹12.79 lakh crore), after Reliance Industries ( ₹17.93 lakh crore) and Tata Consultancy Services ( ₹13.77 lakh crore)

The share exchange ratio for the amalgamation of HDFC with and into HDFC Bank will be 42 equity shares of the face value of ₹1. This means shareholders of HDFC as on record date will receive 42 shares of HDFC Bank ( ₹1 each) for 25 shares of HDFC Limited ( ₹2 each).

Post the amalgamation, HDFC Bank will be 100% owned by public shareholders and existing shareholders of HDFC will own 41% of HDFC Bank.

The merger will create a large balance sheet of ₹25.61 lakh crore, which is now closer to the country’s largest bank — the State Bank of India with ₹45.34 lakh crore. The HDFC Bank was already the country’s second-largest bank. ICICI Bank has a balance sheet size of ₹17.74 lakh crore as of March 31, 2021.

HDFC Bank, which is India's largest private sector bank, has a large base of over 6.8 crore customers. The bank platform will provide a well-diversified low-cost funding base especially current and savings accounts or CASA. The bank will be able to offer more competitive housing products.

| Particulars | HDFC | HDFC Bank |

| Annualised Profit after tax | ₹13,388 Crore | ₹35,875 Crore |

| Networth | ₹1,15,400 Crore | ₹2,29,640 Crore |

| Advances | Rs 5,25,806 Crore | ₹2,68,863 Crore |

| Source: Company reports |

HDFC has 445 offices across the country, these offices can be used to sell the entire product suite of both the Corporation and HDFC bank.

HDFC Bank would also enable seamless distribution of house loans by leveraging its enormous customer base of over 68 million clients, hence improving the rate of credit development in the economy.

The Proposed Transaction is expected to result in bolstering the capital base and bringing resiliency to the balance sheet of HDFC Bank.

HDFC Limited is a significant provider of home loans to the Low-Income Group (LIG) and Middle-Income Group (MIG) segment under the affordable housing initiatives of the Government of India. Access to housing finance for this category would be improved further on account of low-cost funds available with HDFC Bank.

ALSO READ: HDFC-HDFC Bank Merger: Key Highlights

The Boards of HDFC Ltd and HDFC Bank believe that the merger will create long term value for all stakeholders, including customers, employees and shareholders of both entities. The amalgamation of the two entities will provide further impetus to the Government’s vision of “Housing for All”.

Why did the deal take place?

The merger talks between HDFC Bank and its parent company, HDFC Ltd, began about eight years ago, when the Reserve Bank of India permitted banks to issue long-term bonds to support infrastructure and affordable housing.

Banks are not required to maintain Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) for funds raised through this mechanism, according to a notification issued by the RBI in July 2014. They are also exempted from reaching priority-sector lending targets on such funds.

Analysts and banking industry watchers had opined at the time that the regulatory action made sense for the merger of the country's largest pure-play home lender with the country's second-largest private sector lender, resulting in the country's second-largest financial sector company after SBI.

"Some regulatory difficulties must be handled in order for the combination to be more beneficial. Part of it was resolved with the issuance of the circular on infrastructure bonds, but there are a few more concerns about which we are talking to the regulators "In December 2014, Aditya Puri, the then-CEO and Managing Director of HDFC Bank, stated.

Keki Mistry, the vice chairman and chief executive of HDFC, had said a merger was possible "theoretically" and could be done at an appropriate time.

It should be noted that ideas of a merger between the two corporations had been circulating for some time, but supporters argued that there were benefits to continuing as distinct entities until the infrastructure bond notification came in.

HDFC

Housing Development Finance Corporation Ltd., incorporated in the year 1977 (having a market cap of ₹496,425.50 Crore) operating in NBFC sector.

Key Products/Revenue Segments include Interest, Income from Sale of Share & Securities, Other Services, Dividend, Fees & Commission Income and Rental Income for the year ending 31-Mar-2021.

HDFC has total assets of ₹6,23,420.03 crore, turnover of ₹35,681.74 and net worth of ₹1,15,400.48 crore as on December 31, 2021.

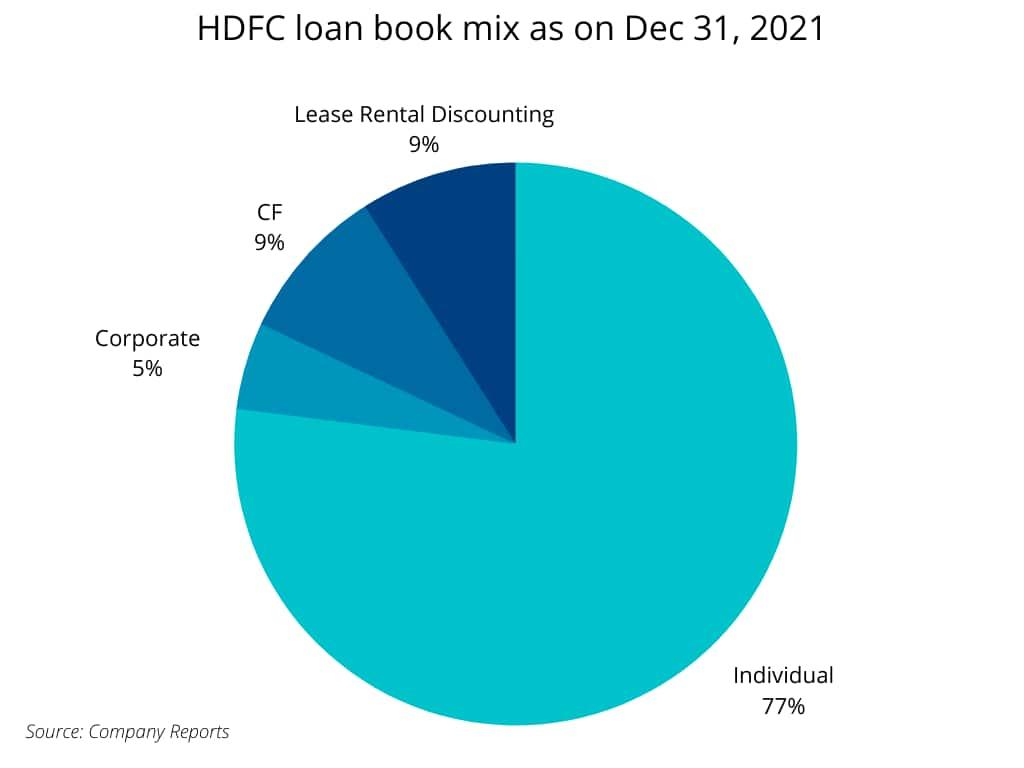

HDFC loan book mix

In FY22, HDFC has approved retail home loans to the tune of ₹2 trillion. This is the highest ever home loan approval by the mortgage financier in a financial year. This is a 30% increase over the loans worth ₹1.55 lakh crore sanctioned in FY21.

Peer Comparision

| Financials (Rs) | HDFC | GRUH Finance | LIC Housing Finance | AAVAS Financier |

| Market Cap(Cr) | 482,564.67 | 23,291.87 | 21,075.66 | 20,034.07 |

| Net sales | 1,39,033 | 2,026 | 19,881 | 1,103 |

| Net Profit | 13,566 | 447 | 2,741 | 288 |

| ROE(%) | 11.95 | 23.64 | 13.30 | 12.03 |

Home loan market in India

At the end of FY-21, the outstanding loan portfolio of home loans in India stood at a whopping ₹22.4 lakh crore, growing 12.1% since its size in FY-20. Also, between FY-17 and FY-21, the Indian home loan market grew by 32% CAGR.

Experts believe the market will show strong growth levels, nearing a 22% CAGR between 2021-2026. And one segment that may drive these growth levels is the affordable housing market.

Between FY-20 and FY-21, affordable home loans showed a YoY growth of 8%, reaching ₹13 lakh crores in portfolio size.

ALSO READ: HDFC Ltd and HDFC Bank to merge: Here's all you need to know

The demand for housing loans is being driven by first-time homeowners as well as by those who are looking to move up the property ladder. Geographically, the demand for housing loans is coming both from metros and non-metros. And, if one were to look at the segments, demand is being driven by affordable housing as well as high-end markets. The sweet spot for housing is still in the price range of ₹50 lakh to ₹1 crore, the lender said in a statement.

“In over four and half decades, I have not seen a better time for the housing sector than now due to lower interest rates, stable property prices, government’s thrust on affordable housing, improved affordability, favourable demographics, increasing urbanisation, and rising aspirations,” said Renu Sud Karnad, MD, HDFC Ltd.

The central government has come out with schemes such as the credit-linked subsidy schemes (CLSS) under the Pradhan Mantri Awas Yojana (PMAY) that have helped in moving towards the goal of housing for all.

Around 270,000 home loan customers of HDFC Ltd have availed off the benefits of the CLSS scheme of the government. The lender has disbursed loans to the tune of ₹45,914 crore under the CLSS scheme as of December end, wherein the subsidy amount stood at ₹6,264 crore.

Further, for the nine months ended December 31, 2021, 30 per cent of home loans approved in volume terms and 13 per cent in value terms have been to customers from the economically weaker section (EWS) and low-income groups (LIG).

Stressed assets of public banks spike over past seven years

First Published: 04 Apr 2022, 02:39 PM IST