Shares of Hindalco Industries, the Aditya Birla Group metals flagship, rose nearly 5% in intraday trade on Monday, despite the company reporting a 35.4% drop in consolidated net profit at ₹2,205 crore for the September ending quarter compared to ₹3,417 in the year-ago period, owing primarily to an increase in input costs. However, the company numbers came in line with analyst estimates.

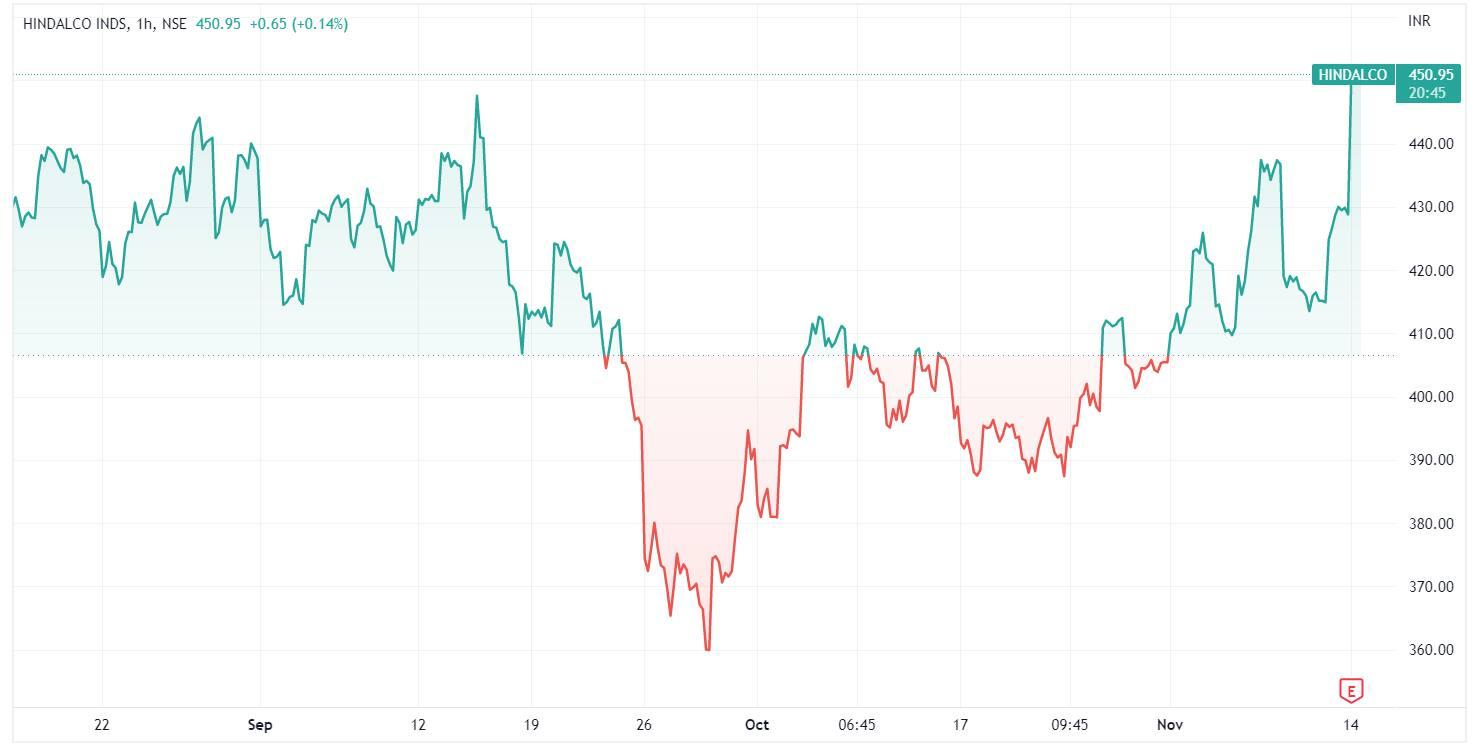

During Monday's intra-day trade, the stock opened with a gap up of ₹5.15 at ₹435 and soared further to hit an intra-day high of ₹452.85. At 01:00 p.m., the stock was trading at around ₹450.25, up by 4.72% on the BSE.

On Friday, Hindalco reported a 17.56% YoY rise in total revenue at ₹56,504 crore compared to ₹48,063 crore in the same period last year. However, the company's operating profit fell by 29.02% YoY to ₹5,743 crore from ₹8,045 crore, impacted by rising input costs and unfavourable macros. This was partially offset by the better operational performance of the copper and downstream businesses, the company said in a statement.

The total expenditure of the company jumped nearly 26.86% to ₹50,756 crore in Q2 from ₹40,008 crore in the corresponding quarter of last year.

The EBITDA margin of the company dropped to 9.54% YoY in Q2 from 15.85%, falling by almost 631 basis points (bps).

Mr Satish Pai, Managing Director of Hindalco Industries, commented on the results, saying, "Despite a surge in input costs, the company produced the highest-ever aluminium metal volumes." "While the upstream aluminium business' EBITDA was impacted due to elevated raw material and energy costs, our downstream aluminium business performed well, with EBITDA more than doubling YoY due to better pricing and market demand."

The copper business outperformed, reporting its highest-ever metal and copper rod sales. Novelis delivered another solid quarter with higher shipments driven by a recovery in the automotive and aerospace segments and better pricing, he added.

On the stock performance front, the stock started the year off on a strong note, returning nearly 40% in the first three months. However, since then, the stock has declined, reaching a 52-week low of ₹315 in June. However, the stock has seen some buying momentum since then and is currently trading at ₹450 levels., though it is still down 29% from its one-year high. At current

Following the Q2 earnings, domestic brokerage firm ICICI Direct Research has given a 'buy' call on the stock with a 12-month target price of ₹500, an upside of over 16.55% from the stock latest closing price. The brokerage expects Hindalco to report a consolidated EBITDA margin of 12.9% for FY23E and 13.1% for FY24E. It also expects Novelis to report EBITDA of US$485/tonne for FY23E and US$525/tonne for FY24E.

The company has indicated that higher energy and logistics costs and an unfavourable metal price lag are likely to impact the second half, ICICI research said.

Global brokerage firm JP Morgan has kept its overweight rating on the stock and reduced the target price to ₹520 from ₹560 per share. The brokerage cut its FY23 EPS estimate by 17% and FY24-25 by 9-10%, CNBC-TV18 reported.

"In the near-term, the stock should trade higher with LME aluminium, while in the medium term, the Novelis margins are difficult to call," it said.

An average of 21 analysts polled by MintGenie have a strong 'buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.