In the September quarter (Q2FY23), overall housing finance companies (HFCs) posted decent numbers. In an earnings review note by domestic brokerage house ICICI Securities, it noted that earnings surpassed expectations for HDFC, Repco, Aavas and HomeFirst; only LIC Housing posted disappointing earnings due to a decline in its net interest margin (NIM).

ICICI Securities sees 100% upside in Repco, downgrades LIC Housing

TL;DR.

Among stocks, post the Q2 earnings, the brokerage expects over 100 percent upside in Repco Home Finance whereas it sees over 40 percent upside in Aavas as well as Home First.

Among stocks, post the Q2 earnings, the brokerage expects over 100 percent upside in Repco Home Finance

whereas it sees over 40 percent upside in Aavas as well as Home First.

Repco Home Finance (Repco) reported a PAT of ₹71.2 crore in Q2FY23 – ahead of expectations of ₹61.3 crore, noted the brokerage. "Encouragingly, despite the entire restructured pool moving out of moratorium and stage-3 aligned to the revised NPA norms, stage-3 assets were up by a mere 10 bps QoQ to 6.5 percent. Further supported by utilisation of ₹20 crore from the contingency provision created in Q1, credit cost settled at 63 bps. Disbursements surpassed our expectations – being up 16 percent QoQ and 54 percent YoY to ₹750 crore. The yield on assets improved by 30 bps QoQ to 10.5 percent, which supported 20bps NIM expansion to 4.8 percent," informed the brokerage.

The company’s business franchise is currently undervalued – the stock trades below its FY23E book and at 3.4x FY23E earnings, and is available at <0.15x AUM, added the brokerage. It has a target price of ₹470 for the stock, indicating a 104 percent upside.

For Home First, the brokerage has a target price of ₹995, indicating an upside of 40 percent.

"The business momentum seen in H1FY23 improves visibility on HomeFirst being able to register over 35 percent AUM CAGR over FY22-FY4E with a stable-to-moderate decline in spreads and contained credit cost. We expect the company to deliver RoAs of 3.8-3.9 percent and RoEs of 13-14 percent until FY24E. Maintain BUY with an unchanged target price of ₹995 (4.25x FY24E book). Key risks: i) Sourcing as well as collections managed by front-end team, and ii) elevated operating cost," it said.

For Aavas, the brokerage has a target price of ₹2,845 (6.0x FY24E BV), implying an upside of 49 percent. Key risks, however, include elevated opex weighing on RoA improvement and competitive pressure on yields, it said.

"Aavas Financiers’ (Aavas) Q2FY23 earnings beat our estimates primarily due to higher assignment income and lower than anticipated credit cost. Disbursement momentum sustained driving 23.6 percent YoY and 5.5 percent QoQ AUM growth. We expect revenue and earnings to compound at >25 percent CAGR over FY22-FY24E and RoAUMs to sustain at >7.5 percent by FY24E," it noted.

However, the brokerage downgraded LIC Housing Finance to 'add' from 'buy' post its disappointing earnings and revised its target price to ₹415 from ₹490 earlier. The new target indicates an upside of just 12 percent.

"LIC Housing's erratic NIM behaviour across quarters makes it difficult to forecast its NIM trajectory with a reasonable degree of confidence. Q2FY23 too has been disappointing. NIM plunge of >70bps QoQ to 1.8 percent (against expectations of an improvement) led to a significant earnings miss. The stock is trading at an inexpensive valuation of 0.7x FY24E P/B, but that is due to volatility and lack of consistency/visibility in earnings," stated ICICI. Key risks include lagged NIM improvement and higher stress flow from restructured pool, it added.

For HDFC, The brokerage has a target price of ₹3,205, implying an upside of 19 percent. "We expect NII growth to further gain traction in the coming quarters with repricing benefit likely to be reaped in its entirety. Maintain BUY with a SoTP target price of Rs3,205 (assigning a multiple of 2.7x to FY24E core mortgage book). Key risks: i) lagged NIM improvement; ii) modest non-individual growth transitioning into the merger," it said.

What worked and failed?

The brokerage has also penned down a few notable trends in operating performance of HFCs.

What encourages

Sustained disbursement and AUM growth momentum: The momentum in disbursements has continued in Q2FY23 as well with players registering a sequential uptick in disbursements in the range of 5-15 percent, said the brokerage. Growth in home loans was seen in both the affordable housing segment as well as in high-end properties, it added. Due to a better-than-anticipated disbursement trajectory, growth in HDFC’s individual loan book improved to 20 percent YoY, HomeFirst registered 36 percent YoY AUM growth, Aptus at 32 percent YoY, Aavas at 24 percent YoY and encouragingly, Repco too registered 1.7 percent QoQ growth, informed the brokerage.

Quarterly run-down rate moderated further: For Repco, balance transfer (BT)-out stood at 12 percent and normal repayments at 6 percent totaling 18 percent, which was flat QoQ but low from 22 percent in Q4FY22, said the brokerage, meanwhile, for Aavas, the pace of BT-out has moderated to monthly 0.5 percent of opening AUM an HomeFirst's BT-out rate was steady at 5.6 percent, it pointed out.

Stress pool in Q2FY23 was managed better across delinquency buckets: Stage-3 assets improved QoQ for HDFC, LIC Housing, HomeFirst, Aptus and PNB Housing while it was broadly stable QoQ for Repco and Aavas, stated ICICI.

Overall provisions as a percentage of AUM trend (QoQ) mixed across players: For Q2FY23, PNB Housing had the highest credit cost at 224bps, followed by LIC Housing at 131 bps, Aptus at 95 bps, Repco at 63 bps, Home First at 49 bps, HDFC at 42 bps and Aavas at mere 5 bps, it noted.

What fails to cheer

Repricing of loans at a slower pace compared to repo rate hike: Recent credit rating upgrades and optimised borrowing profiles for a few affordable HFCs have helped them manage funding costs well. HFCs have raised rates in Q2FY23 and are planning to raise rates in Q3FY23 as well. However, the quantum of rise is not directly proportional to the repo rate hike, explained the brokerage. Aavas has increased its prime lending rate (PLR) by 75bps in H1FY23 and hiked it by another 50bps w.e.f. 5th Oct’22. Aptus has not hiked its lending rates yet. HDFC has increased its benchmark lending rates by 50bps w.e.f. 1st Oct’22 in addition to the hikes taken in H1FY23. HomeFirst has raised PLR by 25 bps in Q2FY23 and is contemplating another raise of 50 bps either in Q3 or Q4. LICHF has further raised PLR by 115bps from 1st Oct’22 over and above the 60bps in Jul’22. Repco has hiked its lending rates by 35bps in Q2FY23, it informed.

Opex to assets sees a sequential uptick: Opex trend was largely similar for affordable HFCs wherein Aavas, HomeFirst and Aptus saw rise of 30-45 percent YoY; Repco, LIC Housing and HDFC saw rise of 10-20 percent YoY, while LIC Housing was the only outlier with 5 percent YoY decline in opex, said the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

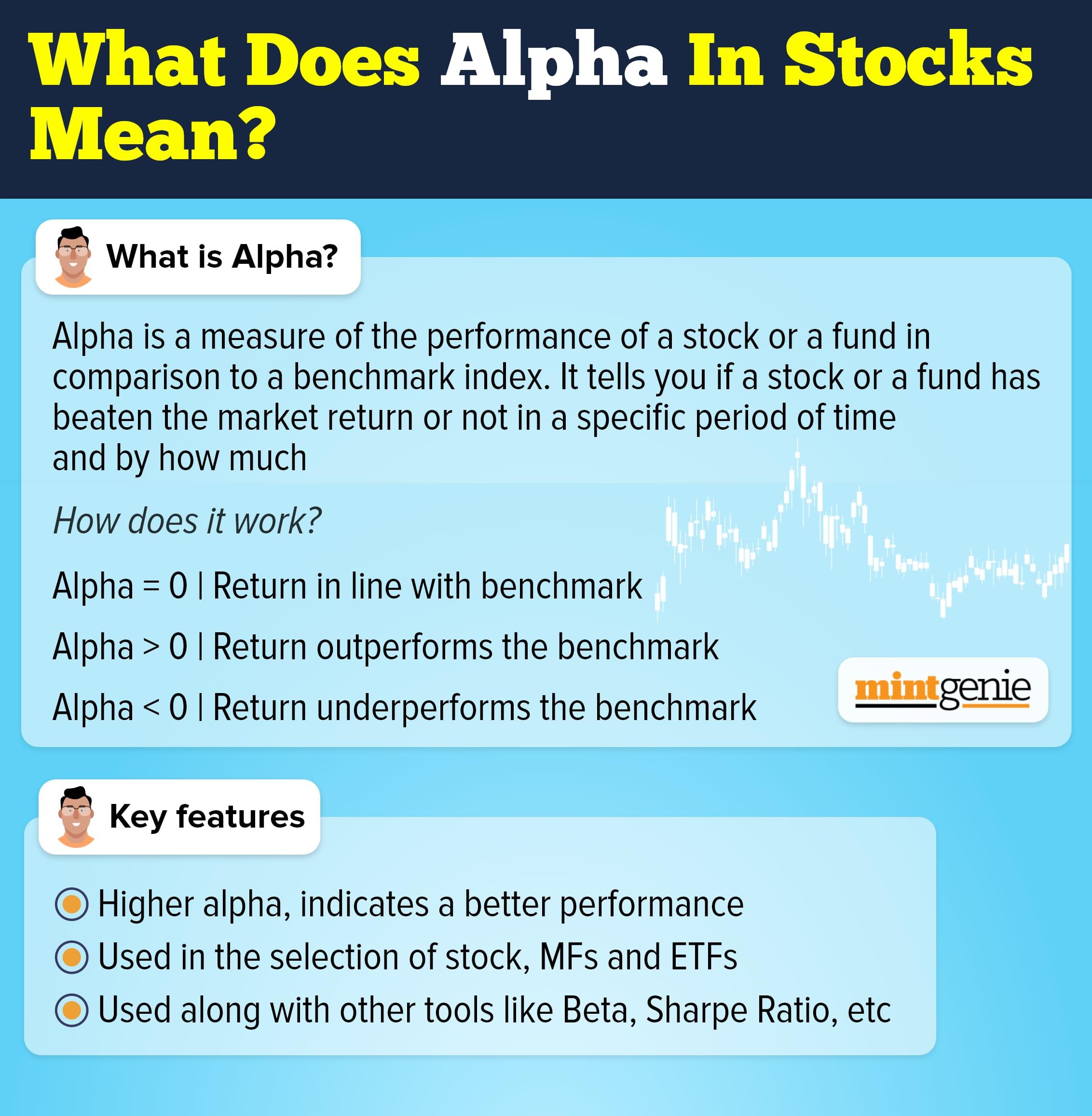

What is alpha in stocks

First Published: 25 Nov 2022, 03:14 PM IST