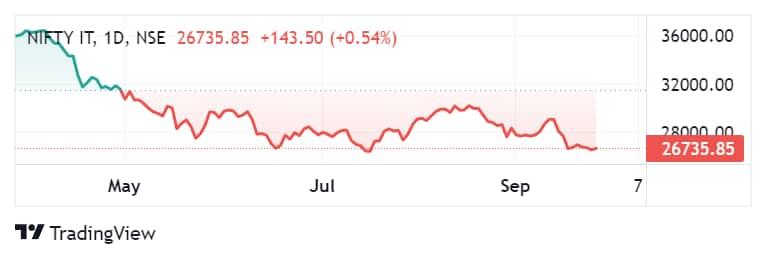

The Nifty IT index has massively underperformed benchmarks in the last 1 year as well as in 2022 YTD. The index has tanked 28 percent in the last 1 year and 31 percent in 2022 YTD. In comparison, the Nifty has lost 4.5 percent in the last 1 year and 1.5 percent in 2022 YTD.

The stocks have been falling amid heightened worries that a recession in the US will erode demand for IT services which will put pressure on the margin of Indian IT firms, which is already declining.

As per analysts, sticky inflation is likely to cause a prolonged phase of rate hikes which may mean a longer recession. Investors are concerned that the earnings of IT companies in FY23 and FY24 may be subdued. This concern also seems to have triggered a selloff in IT stocks.

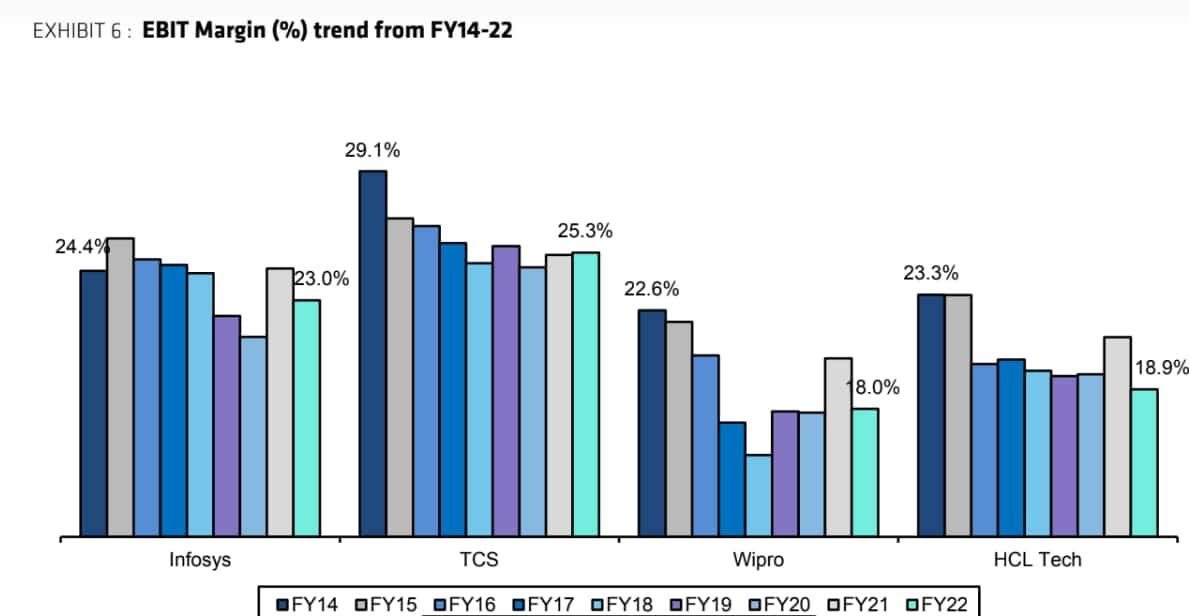

Brokerage house Bernstein takes a look at the margins (quarter on quarter) for the top 3 IT firms - TCS, Infosys and HCL Tech from Q1FY22 to the recently reported quarter Q1FY23.

TCS: Supply side challenges have been a bigger issue in the near term and a headwind on margins. TCS has indicated that salary hikes in FY22 could be in the range of FY23. In FY22, margins were impacted by wage hikes, subcontractor costs and cost of attrition which has an overall impact of 330 bps. EBIT margins for Q1FY23 were a miss at 23.1 percent (down 190 bps QoQ) driven by annual salary increment to the tune of 150 bps, noted the brokerage.

Infosys: Infosys margin guidance in FY23 is 21-23 percent. EBIT margin in Q1FY23 was a miss with margin headwinds from wage hikes (160 bps), lower utilization (40bps) & sub-contractor costs (30 bps), it said.

HCL Tech: HCLT maintained guidance of 18-20 percent for FY23. Margins decline 90 bps in Q1FY23 led by100 bps of sub-con costs & 50 bps wage hike, stated the brokerage.

But the question remains whether margins have bottomed out. Brokerage house Bernstein looks back at past cycles in 2001 (Y2K) & in 2009 (GFC) and how margins panned out.

The brokerage pointed out that in 2001, industry margins were reset lower but helped drive over 40 percent CAGR growth from 2004-08. However, in 2009 (Global Financial Crisis) the margins were protected driven by deep cost/wage cuts.

"Margins have moderated for the industry as growth slowed. Growth post-GFC moderated down due to scale & shift from legacy services to digital services," said the brokerage.

In a recent note, the brokerage looked at the likely margin outcomes and analyze the micro variables of costs for the sector.

Cost structure: Bernstein believes that the current scale of the business and flexibility in cost structure allows the Indian IT companies margin leverage. "Salary costs have the highest mix within total costs with 50-55 percent of revenues. Few companies have announced variable pay cuts, subcontractor costs are 7-8 percent of revenues, and travel is 1.5-1.6 percent of revenue but has come down to 0.7 percent post-Covid. Other costs are 2.5 percent of revenues," it informed.

Historical margin performance: The brokerage pointed out that the period of 2004-08 was a period of high growth which led to IT services companies relaxing hiring and performance norms. Salary costs expanded as companies absorbed the limited talent leading to margin erosion, it noted.

However, during the GFC in 2009, variable pay was realigned to get flexibility on margins, it said, adding that then, in 2020 margins expanded led by an increase in offshoring and limited travel costs. Now, in 2022 (Q1FY23), the margin impact was led by wages/high attrition (150-200 bps).

It highlighted that growth post-GFC moderated down due to scale & shift from legacy services to digital services. Growth remained healthy at 10-15 percent post-2010-2015 with global IT spend growth only at 2-3 percent average growth rate, however, growth declined during Covid in 2020 but accelerated strongly to 15-20 percent growth in 2021 led by pent-up demand in the sector, it noted.

Profitability drivers: As per the brokerage, the EBIT margins for Indian IT services companies are driven by a few key variables a) pricing power from customers, b) wage inflation c) currency d) pyramid, mix/offshoring. With headwinds from wage inflation, Indian IT companies are using other levers to manage margins in the near/medium term, it noted

Levers to support margins: Key levers to support margins are higher offshoring and better pyramid mix, stated the brokerage. Pricing discussions have been constructive with expectations of improvement, however, they back-ended in H2FY23. Other margin levers include lowering attrition, it added.

Margin outlook: Infosys believes it has sufficient levers to improve margins (from the bottoms of Q1FY23), noted the brokerage. Margin improvement to be driven by Potential pricing increase in digital, higher utilization as more freshers get billed while offshoring remains a lever, it said.

FY23 Margin estimates: Infosys has guided for 21-23 percent EBIT margin, while for HCL Tech guidance ranges between 18-20 percent. Wipro had indicated margins likely below the guidance band of 17-17.5 percent over the next 2-3 quarters and TCS is expected to maintain margin within a tight band of 25 percent. Bernstein expects EBIT Margins to moderate over FY23. Its estimates for margin for Infosys is 22.5 percent, TCS at 25.2 percent, HCL Tech at 19.5 percent and Wipro at 17.5 percent.

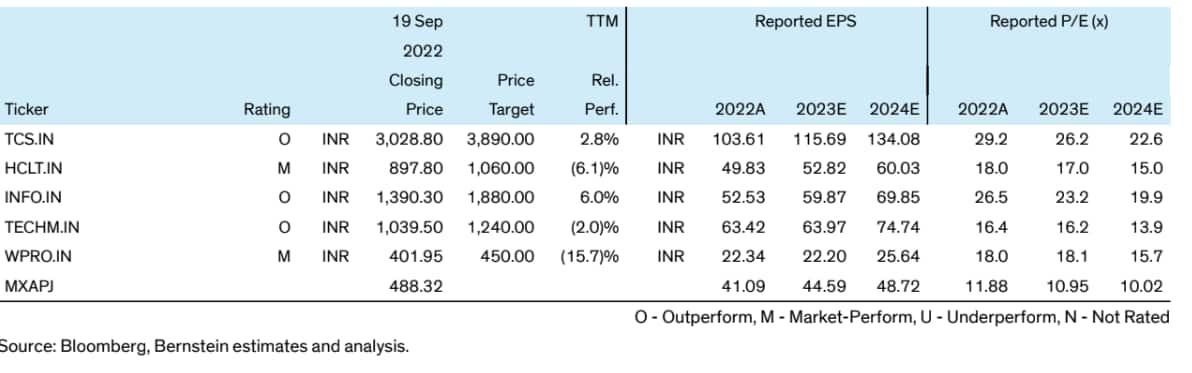

Top picks: The brokerage remains positive on the sector and prefers large caps over mid-caps. Its top pick is Infosys driven by deep digital positioning, strong growth momentum (13-15 percent FY23 YoY CC guidance), and attractive valuation (20 percent discount to TCS). Meanwhile, it is 'Outperform' on TCS given the strongest Billion Dollar Playbook, and resilient margins, however, valuations are keeping risk/reward in the balance.

In its coverage, it has an 'outperform' call on Infosys, TCS and Tech Mahindra while having a 'market-perform' call on Wipro and HCL Tech.