Two major IT firms Infosys and HCL Tech posted their third-quarter earnings for the financial year 2022-23 (Q3FY23) yesterday, January 12. Both the firms reported better-than-expected earnings growth, but which one did it better? Let's find out:

Infosys, HCL Tech post Q3 earnings: which IT major did it better?

TL;DR.

Two major IT firms Infosys and HCL Tech posted their third-quarter earnings for the financial year 2022-23 (Q3FY23) yesterday, January 12. Both the firms reported better-than-expected earnings growth, but which one did it better? Let's find out:

Profit and Revenue

Infosys reported quarterly profit that beat estimates, and raised its annual revenue outlook, helped by a strong deal pipeline.

The country's second-largest IT firm reported a 13.4 percent rise in its consolidated net profit for the quarter ended December 2022 at ₹6,586 crore, as against ₹5,809 crore in the same quarter last year.

The company's consolidated revenue from operations increased 20.2 percent to ₹38,318 crore as against ₹31,867 crore in the corresponding quarter last year. In the December quarter, constant currency revenue growth was strong at 13.7 percent on year, and 2.4 percent sequentially.

HCL Tech also surpassed estimates in terms of profitability, revenue as well as margins in Q3

HCL Technologies reported a 20 percent rise in its consolidated net profit for Q3FY23 at ₹4,096 crore as against ₹3,442 crore a year ago.

Its consolidated revenue from operations increased 19.61 percent to ₹26,700 crore against ₹22,321 crore in the corresponding quarter last year. Revenue in terms of constant currency was up 5 percent sequentially and 13.1 percent YoY.

Revenue and margin guidance

Infosys raised its revenue guidance for the current financial year to 16-16.5 percent from the estimated revenue growth of 15-16 percent projected earlier.

However, HCL Tech narrowed its guidance for FY23 or the current financial year to 13.5-14 percent from 13.5-14.5 percent earlier.

Meanwhile, Infosys retained its operating margin guidance for FY23 at 21-22 percent whereas HCL Tech also lowered its operating margin guidance to 18-18.5 percent from 18-19 percent earlier.

Deal Wins

Despite the quarter being a seasonally weak one for the sector, Infosys won deals worth $3.3 billion, the strongest in the last eight quarters.

Meanwhile, HCL Tech said it won 17 large deals during the quarter - seven in the services segment and 10 in software. The total contract value (TCV) of new deal wins was at $2.35 billion, up 10 percent YoY.

Stock price trend

Infosys has been mostly flat, swinging between gains and losses after its third-quarter results. The stock recovered after falling around 1 percent to rise a little over 1 percent to ₹1,501 in intra-day deals.

Meanwhile, HCL Tech has been in the red post its Q3 results. The stock has fallen around 2 percent to ₹1,042 in intra-day deals.

What brokerages say:

Motilal Oswal

The brokerage has buy calls on both stocks. It has given a target price of ₹1,760 for Infosys, indicating an upside of 19 percent. For HCL Tech, its target price is ₹1,270, implying an upside of 18 percent.

Infosys posted a strong set of earnings in 3QFY23 despite seasonality. Its strong FY23 growth guidance and strong deal pipeline provide further demand visibility, said MOSL. It expects Infosys to deliver a margin at the lower side of its guided band, with strong growth and reduced dependence on sub-contractors as attrition falls. It also sees Infosys as a key beneficiary of acceleration in IT spends.

MOSL added that Infosys reported a strong TCV of $3.3 billion (the highest in the last eight quarters), with the highest-ever 32 large deals, of which 36 percent were net new. The deal pipeline remains strong with a higher focus on cost-saving programs, it added. Signs of weakness in macro are clearly visible. Europe is more affected than the US. Mortgage, IB, Telecom, Hi-Tech and Retail are the most affected, with uncertainty on spends, noted the brokerage.

For HCL Tech, it stated that despite seasonality and a tough demand environment, the firm maintained its growth momentum in both IT Services and ER&D verticals. HCL Software delivered strong growth, ahead of expectations on seasonality and the deal wins remained strong (book to bill of 0.7x), it said. While there is visible weakness in macro, especially in Europe, increased vendor consolidation deals, a strong pipeline of cost-take-out deals, and favorable pricing should help HCL Tech tackle any softness in discretionary spending and weak macro, noted MOSL.

"The strong growth guidance and margin performance in an environment, where demand for IT services is expected to be incrementally weaker, should boost investor confidence in HCL Tech’s business and lower the valuation gap with larger Tier-1 peers. We continue to see HCLT’s defensive business as positive in a demand-constrained environment," rationaled MOSL. Strong sequential growth within Services, robust headcount addition, healthy deal wins, and a solid pipeline indicate an improved outlook, it added.

Nirmal Bang

The brokerage has a sell call on both Infosys and HCL Tech post their Q3 Earnings. For Infosys, it has a target of ₹1,161, implying a downside of 22 percent whereas for HCL Tech, it has a target of ₹847, indicating a downside of 21 percent.

Infosys’ Q3FY23 CC QoQ revenue growth at 2.4 percent came in ahead of our 1.6 percent estimate, but with 110 bps gain coming from pass-through of ‘third-party items for service delivery to clients’, noted NB. The brokerage is assuming a low-mid single-digit growth from both lower volume as well as some price compression whereas consensus is building in a high single-digit growth implying a soft landing in the US. It expects tighter IT spending by customers due to a significantly weaker corporate revenue/profit picture amid a likely shallow recession in CY23 in the US. Also, as was the case in FY22, when third-party items had added 150 bps to growth, based on our understanding, 9MFY23 seems to have added another 200 bps, noted NB. The unusually high ‘third-party items for service delivery to clients at 6 percent in 9MFY23 seems to have helped Infosys in winning integrated deals, however, the brokerage believes a continuance of this strategy will lead to margin dilutive growth in the times ahead.

HCL Tech (HCLT) in Q3FY23 delivered CC QoQ revenue growth of 5 percent, much above the 3 percent growth that the brokerage was estimating, largely driven by the 30.5 percent QoQ growth delivered by HCLT Software, noted NB. The company has indicated that 4QFY23 should see softness on a QoQ basis but the brokerage feels that the management sounded optimistic on the medium growth picture though it dropped hints that there could be a few soft quarters in the foreseeable future.

The brokerage feels that the firm seems to be assuming that there is going to be a no-recession situation in the US in CY23. The positive view also likely stems from a rather strong net new order inflow that the company has seen in the last few quarters. While FY23 is in the bag, NB believes that growth will materially slow down in FY24. It believes that HCLT will also feel the negative impact of the stagflationary environment developing in the western world, which will likely affect tech spending in FY24 and as macro deteriorates, it sees clients wanting to squeeze pricing on this part of their spend.

HDFC Securities

The brokerage has a buy call on Infosys with a target price of ₹1,815, implying an upside of 22.5 percent. Meanwhile, for HCL Tech, it has an add call with a target of ₹1,090, indicating an upside of just 1.6 percent.

As per the brokerage, key drivers for Infosys in Q3 include strong deal bookings, commentary on pipeline supporting growth visibility, recovery expected in North America, acceleration in vendor consolidation, and cost take-out deals reflected in the growth in core services. On the flip side, however, large deal aggression is getting reflected in higher pass-through components and BFSI vertical (-1.7 percent QoQ) underperformed, impacted by higher furlough, some project completion, and softness in mortgage & investment banking sub-segments.

HCL Tech (HCLT) posted in-line services revenue and higher-than-estimated software revenue, driven by Q3 seasonality, said the brokerage. Key positive catalysts for HCLT in Q3 were an increase in large deal wins supported by infra services led cost optimisation and vendor consolidation, synergy services deals from the software installed base and stability in the software business, it noted.

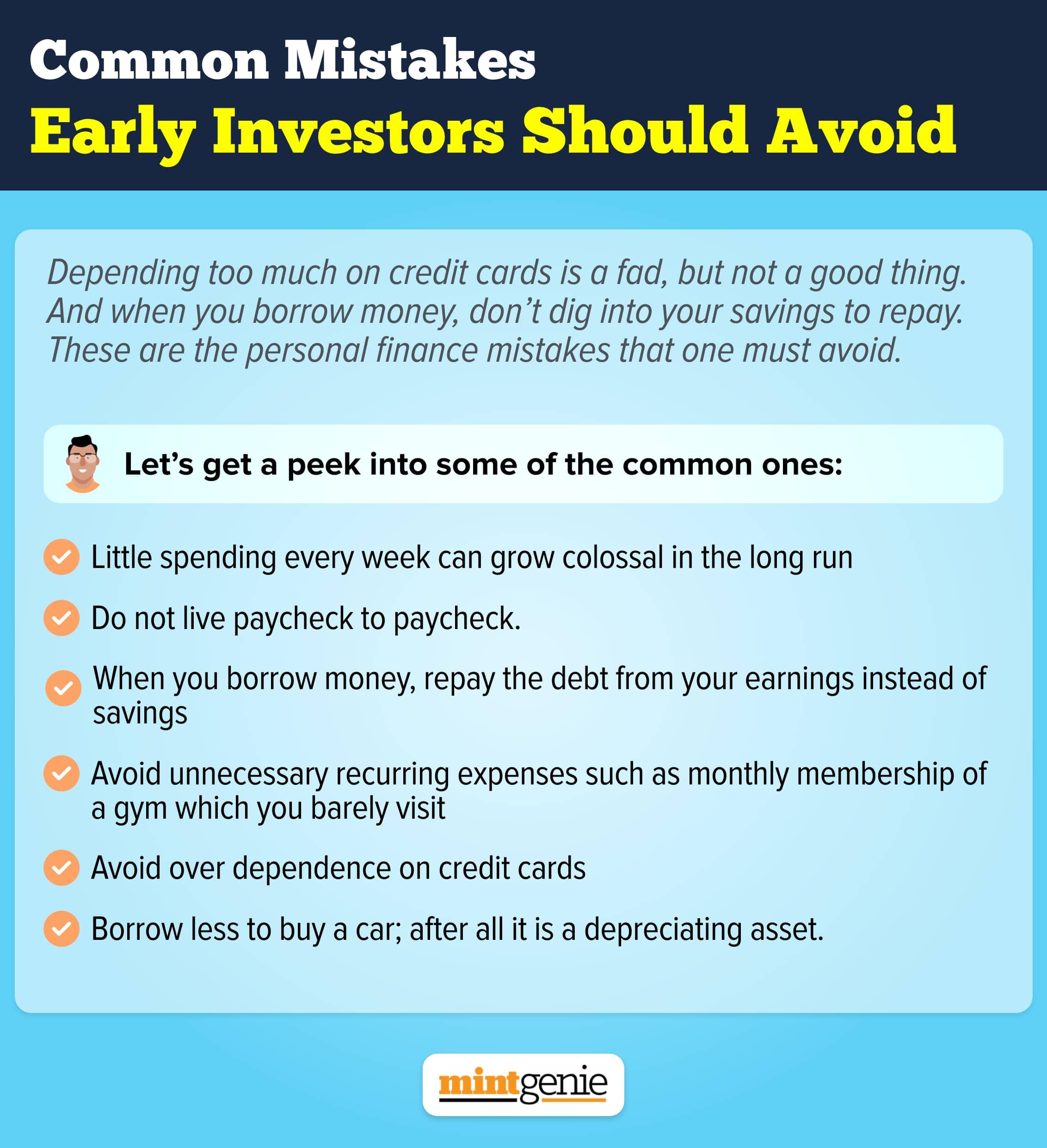

These are the common mistakes which early investors should avoid.

First Published: 13 Jan 2023, 12:25 PM IST