US-based IT major Accenture beat revenue expectations in the third quarter of FY22, with its revenue coming in at $16.2 billion, up 22 percent year-on-year (YoY). The IT major reported revenue worth $13.26 billion in the same quarter last year.

Is Accenture's Q3 results positive for the Indian IT sector? Here's what brokerages say

TL;DR.

Most experts believe that Accenture's double-digit growth is a positive for the Indian IT sector. Its commentary suggests that the demand environment remains supportive, they added.

The company follows a September-August financial year and the third quarter represents the March-May 2022 period.

The company's operating income also rose 23 percent YoY to $2.6 billion while its operating margin for the quarter came in at 16.1 percent.

The firm also raised its revenue guidance. For FY22, it expects revenue growth to be in the range of 25.5-26.5 percent from 24-26 percent previously. Meanwhile, for the fourth quarter, the company has guided for revenue of $15 to $15.5 billion, growing at 20-24 percent

However, despite the results beating analyst expectations, the Indian IT sector reacted poorly amid concerns regarding inflation and foreign exchange impact. The Nifty IT index fell around 0.8 percent in today's trade as against a 0.5 percent rise in Nifty50. It was the only sector in the red in an otherwise strong market.

Accenture also noted that revenues for Q3 reflect a foreign-exchange impact of -5 percent and for the fourth quarter, it sees a foreign-exchange impact of -8 percent.

Most experts believe that Accenture's double-digit growth is a positive for the Indian IT sector. Its commentary suggests that the demand environment remains supportive, and the weakening macro environment has not yet started impacting growth in the sector, they added.

Let's take a look at what major brokerages have to say regarding Accenture's third-quarter results:

Motilal Oswal

As per the brokerage, Accenture reported a better than expected Q3FY22, with revenue growing 27 percent YoY in constant currency (CC) terms. It also upgraded its FY22 revenue growth guidance by 100 bps at the mid-point, although its Q4FY22 revenue guidance missed consensus estimates, it added. This is likely to add to concerns about the impact of a deteriorating macro-economic environment in the US and Europe, MOSL said.

The brokerage views the results as mixed. While strong revenue growth and commentary on the pipeline is positive for the IT Services sector, weak employee addition (lowest in the last six quarters) and moderation in deal bookings (-13 percent QoQ) should dampen the demand outlook, it noted.

MOSL further pointed out that the management indicated a healthy pipeline and strong spends in the areas of Digital, Cloud, Sustainability, and Security. While it did not indicate any slowdown in demand due to a weakening macro-environment, it sees a shift in spends towards cost savings as against a growth focus earlier, stated the brokerage. MOSL views this as a positive for its Indian IT Services peers as cost optimization is a key driver of offshoring.

"While supply-side challenges remain a point of concern, with elevated attrition and lower headcount addition, ACN’s margin guidance implies a stable margin performance in FY23. We maintain our positive stance on the sector as we expect sustained growth with a stable margin. Infosys, HCL Tech and TCS remain our preferred picks within the Tier I IT space," it said.

Nomura

The global brokerage noted that the revenue growth of Accenture was broad-based across all key industry verticals and geographies. Accenture tightened its revenue growth guidance for FY22, however, it expects the negative impact of cross-currency movements on FY22 revenue growth to be 450 bps vs 300 bps expected earlier, said Nomura.

"The demand outlook remains strong, particularly aided by demand for transformational services and cloud adoption. In our recent IT sector downgrade report, we had noted that while FY23F demand outlook remains strong, we expect it to slow down faster than consensus estimates for FY24F," it added.

Nomura further believes that cross-currency could be a material headwind to the reported growth of Indian IT companies in FY23F, however, pricing increase may act as a key lever in margin defense. Accenture noted that it has begun to see some effects of price increases in 3QFY22, and it expects further boosts in coming quarters, it pointed out.

"We recently downgraded the India IT sector driven by our expectation of slower revenue growth in FY24F and continue to prefer large-caps over mid-caps. Infosys and TechM remain our only Buy calls in the sector," Nomura said.

Kotak Institutional Equities

As per the brokerage, Accenture management indicated no change in decision-making and expects strong bookings and revenue growth in 4QFY22. Results were strong though the focus of the Street has shifted to impact on business in a recessionary environment, it added.

"The immediate impact of a deteriorating environment is not visible from the results or decision-making of clients. In fact, Accenture increased revenue growth guidance, reported stronger growth in Europe (perceived to be more vulnerable) and delivered better growth in bookings in consulting (considered to be more vulnerable). In a way, the results and outlook are as good as it gets, especially in the context of lowered expectations, visible in 12 percent correction in stock price in the past three months (46 percent correction from the peak)," said Kotak.

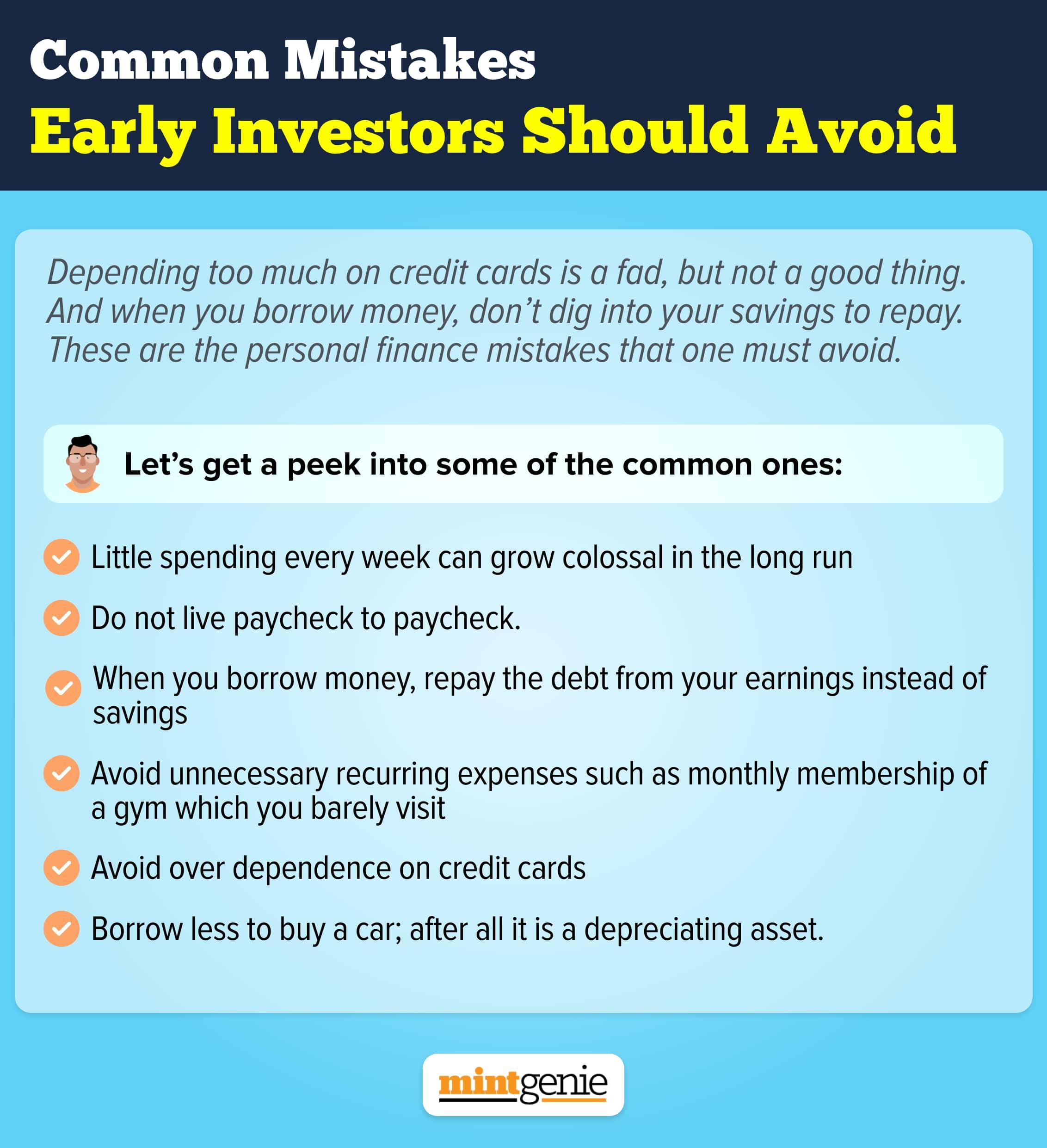

Common mistakes early investors should avoid.

First Published: 24 Jun 2022, 01:20 PM IST

Related Stories

personal finance

Fund managers advise investment in dynamic bond funds amid rate hike environment: Report

Team MintGeniemarkets

This Tata group stock rises 110% in one year; brokerage sees another 25% upside

A Ksheerasagar

Explain Like I am 5

personal finance

Berkshire's annual meet: 7 key lessons investors can learn from Warren Buffett

Team MintGenie