Global IT firm Accenture delivered robust earnings in the quarter ended February 2022 (Q2FY22). The firm follows the September to August financial year. The firm posted revenue growth of 28 percent year-on-year at $15 billion, in constant currency terms, in the quarter under review. While in dollar terms the growth came in 24 percent YoY.

Reported revenues were higher than the guidance band of $14.5-14.75 billion. The IT major also raised its full-year FY22 revenue growth guidance to 24-26 percent as against 19-22 percent forecasted earlier. For the third quarter, Accenture expects revenues to be in the range of $15.70-16.15 billion, up over 20 percent from the current quarter.

The sharp upwards revision indicates strong spending which is also a positive for Indian IT. Accenture’s performance is usually seen as an indicator of the IT sector’s outlook in India as well. The broad-based, double-digit growth and all-time high deal bookings of $19.6 billion (17 percent above the previous high seen in 1QFY22) will provide good demand visibility for IT services.

The strong results posted by Accenture led to a rise in Indian IT stocks in intra-day deals. Infosys, L&T Technology Services, Wipro, Coforge and Tech Mahindra rose around 1-2 percent in an otherwise weak market, while TCS, Mindtree, HCL Tech and Larsen & Toubro Infotech were in flat-to-positive range.

"Outstanding second-quarter financial performance demonstrates continued strong broad-based demand across all our markets, services and industries," said Julie Sweet, chair and CEO at Accenture.

However, the firm added that the third quarter and full-year business outlook does not include assumptions for a significant escalation or expansion of economic disruption or the conflict's current scope, which could have a material adverse effect on the company's results of operations.

Impact on Indian IT

In a recent note, global brokerage house Nomura said that a prolonged war leading to significant weakness in the eurozone GDP growth rate could lead to India IT companies sounding caution in their FY23 outlook and guidance in the coming weeks.

However, post the Accenture results, domestic brokerage house Motilal Oswal believes the demand environment continues to remain strong and is sustainable in the long run. Further, an upgrade in FY22 guidance provides visibility to the Indian IT services sector’s growth momentum, it noted.

"While supply-side challenges remain a point of concern, Accenture's margin guidance (marginal cut of 10bp) implies stable margin performance in FY23. We maintain our positive stance on the sector as we expect sustained growth with stable margins. Infosys, HCL Technologies and TCS remain our preferred picks within the Tier-I IT space," said Motilal Oswal.

Nomura also believes that newer contracts coming in at better pricing may help to offset margin headwinds. In largecaps, Nomura prefers Infosys and Wipro, while in midcaps, its top pick is Persistent Systems.

Nomura has buy calls on all three stocks. For Wipro, it has a target price of ₹850 (41 percent upside). For Infosys, it has a target price of ₹2,440 (31 percent upside), and for Persistent, it has a target price of ₹5,330 (19 percent upside).

As per Jefferies, Accenture’s Q2 FY22 performance and guidance suggest a very strong demand environment for the sector over the next few quarters. Strong results provide ease of concerns over growth in client IT budgets amid worsening macroeconomic situation, it added. While margins are likely to be under pressure, the brokerage prefers Infosys and Tech Mahindra given their strong growth outlook.

Meanwhile Phillip Capital said, "With strong bookings, robust pipeline, strong guidance upgrade, optimistic demand commentary and no impact of Russia-Ukraine crisis on business (yet), provides strong visibility for the Indian IT Sector."

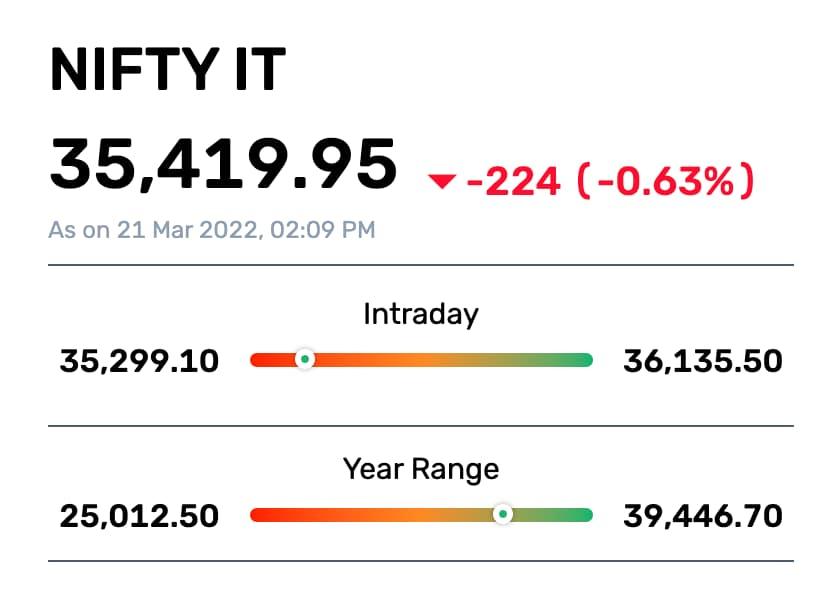

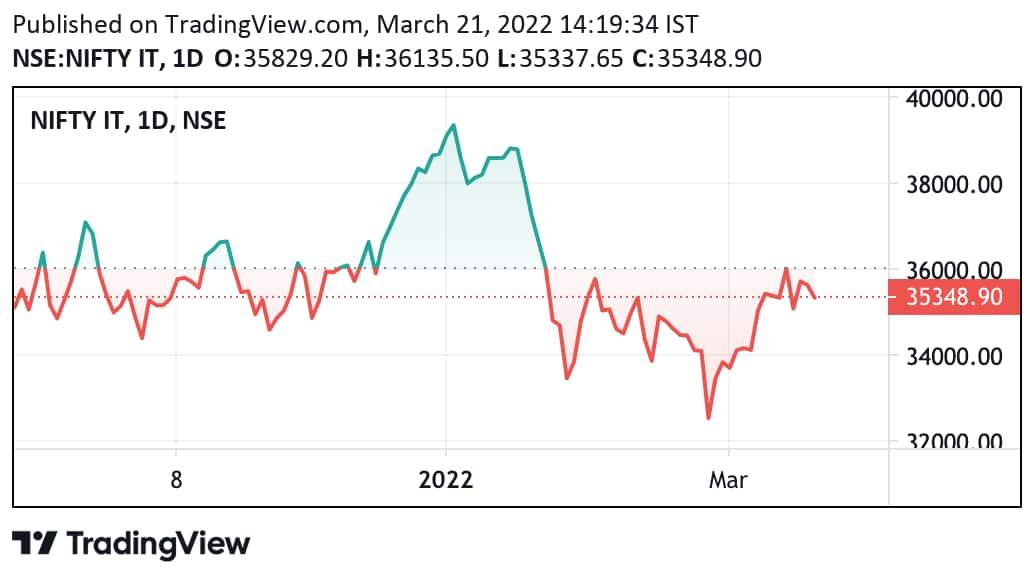

IT stocks had seen a sharp correction from highs, before recovering recently. The Nifty IT index over 11 percent between January and February but has outperformed the benchmark, rising 4 percent in March till date. In comparison, benchmark Nifty has gained 2 percent in March till date.

Counter View

Meanwhile, brokerage house Nirmal Bang pointed out that this strong performance could also be a threat to the Indian IT companies in terms of market share.

“Accenture has seen accelerated market share gains in FY20-FY22 compared to Tata Consultancy Services Ltd and Infosys Ltd, indicating that its capability set is probably seeing greater market traction. It has been talking about 3x industry growth in recent days versus 2x in the past" it said in a report.

The total new bookings in Q2 reached a record $19.6 billion and the number of clients with bookings over $100 million stood at 36, up from 20 clients in Q1.

As per Nirmal Bang, this suggests that Accenture is capturing increased market share in mid and large deals, which are likely complex, multi-service line deals and involve business transformation. Accenture has also gained market share through acquisitions of $1.8 billion in 1HFY22, it noted.