Among new-age companies, some are changing the way we make payments, some are changing the way we consume food, and some are changing the way we shop for specific products. Each of these businesses has shown the capability to build strength. Over time, as they demonstrate the ability to scale up and grow profits, they are likely to find a place in most portfolios, said Alok Agarwal, Portfolio Manager, Alchemy Capital. In an interview with MintGenie, Agarwal shared his views on the market and economic trends.

Edited excerpts:

Are we out of woods or yet to see the worse? What is your view on the market for the next financial year? What are the key headwinds and tailwinds?

The bulk of the period since the global financial crisis (GFC) was characterized by quantitative easing (QE) where the central bankers cut rates and also printed money.

This had a positive impact on the risk assets, especially valuations.

All was well till the time inflation was in check. But, with multi-decade high inflation in various countries, the central bankers had to reverse this QE and resort to quantitative tightening (QT), since late last year.

This had a negative impact on risk assets.

At one point of time during the QE phase, we had seen over $15tn of global assets being invested in negative-yielding government securities.

Now, with rising yields, we are seeing that certain sections with high leverage are severely impacted as seen in recent banking turmoil in the US and Europe.

While inflation is showing signs of moderation and we may likely be closer to the end of the rate hike cycle than the beginning, the last few miles have to be travelled, which is showing signs of heightened volatility.

Valuations have corrected and are now closer to longer-term averages.

The ongoing quantitative tightening (QT) has ensured that ‘growth at any price’ is passe’.

However, relevant growth, which continues to be scarce, could still be chased, albeit at reasonable prices/premiums.

Nifty is trading at 17.3 times – one year forward earnings, this is the same as the last 10-years’ median valuation, nearly 24 percent below historic highs touched in October 2021.

Froth in valuations getting out of the way is a major tailwind for Indian markets.

It is interesting to note that, this is only the fifth occasion in history, where Nifty's one-year forward PE (price-to-earnings) has corrected over 24 percent from its peak. The previous four were in 2006, 2008, 2011, and 2020.

History suggests that accumulating during such times has been rewarded by markets.

India is amongst the fastest growing economies, with the most effective shock absorbers in current times.

Nifty earnings are expected to grow at 15 percent CAGR over the next two years – higher than any other major economy.

Hence, the absolute and relative strength of India is likely to continue keeping it a preferred investment destination.

As long as QT and rate hikes are on, difficult to say that we are out of the woods. However, in these times, India stands out.

While we are very bullish long-term on India, the next financial year is expected to be affected by multiple factors – the key ones have been discussed above.

We are positive for the next financial year and find these times attractive for accumulating equity.

The key headwind for the markets is QT and the key tailwind for India is world-beating growth both in terms of GDP and corporate earnings.

Is it still a buy-on-dips market? Why or why not?

It is a buy-on-dips market in our view. We need to zoom out and think. Valuations at 10-year averages and earnings growth are expected to be in the mid-teens over the next couple of years – this is a combination we have rarely seen in the last 10-15 years.

This comes at a time when the corporate balance sheet is significantly stronger than a decade ago.

While no one can time the exact bottom, the current banking turmoil in the developed world along with peaking-out signs in inflation shows that QT may not last for too long or at least is unlikely to get stronger.

These are times to accumulate good quality companies with a strong balance sheet, proven management and growth visibility.

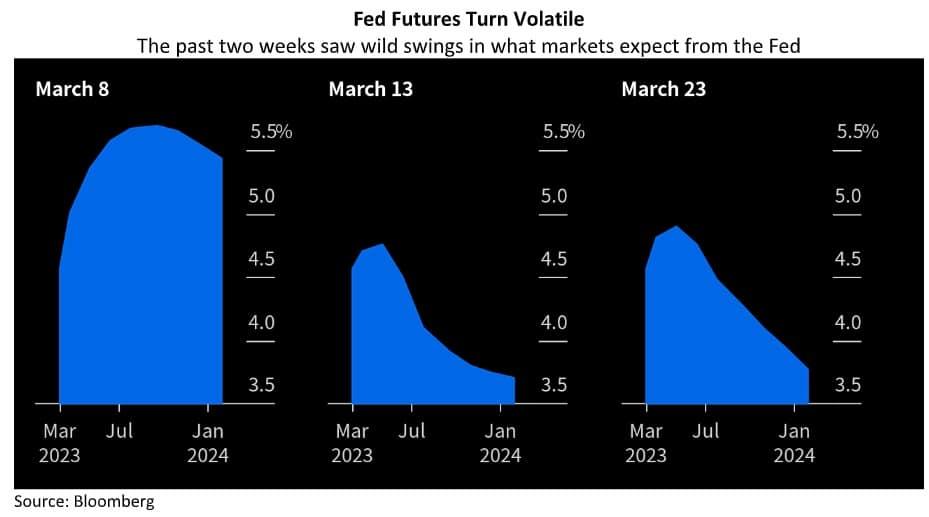

The market is expecting the US Fed to take a pause on rate hikes soon while the Fed expects the market to factor in a long phase of higher rates. Do you think there is a clash between markets’ hopes and Fed policy? When can Fed start reducing rates?

Lower rates with higher liquidity are a forever wish for markets. However, the Fed has made it clear that it is focused on taming inflation.

While US CPI inflation has come down to 6 percent from a peak of 9.1 percent in June 2022, the Fed is not too keen on stopping the hikes till their target of 2 percent inflation is met.

Now, with rates rising, there will always be a section that will lose out, especially institutions having a major asset-liability mismatch. Add leverage to it and the problem compounds.

This has been at the centre of recent banking turmoil in the US and Europe. This adds another dimension for Fed.

While targeting inflation, they now need to do a balancing act of taming inflation while trying to avoid a hard landing and manage the institutions that are on the edge – it’s like balancing the role of being the slayer of inflation and also a crisis firefighter.

Federal Reserve has pushed ahead with its policy of raising interest rates to bring down inflation. But in reality, things are not the same after a string of bank collapses sent tremors through world markets.

Although the Fed hiked, the fact is that the hike was only half of what was expected before the recent banking collapses.

Analysts and market observers are now significantly hopeful that the US will not see a recession this year. What are your views on it? Is the global economy in a better situation than it was six months ago?

These observations have seen a significant change in the last few weeks with the banking collapses in the US and Europe.

This is bound to impact the risk-on capabilities, overall credit offtake and growth recovery.

The odds of the US seeing a recession have certainly increased due to these events. Such an unprecedented hiking cycle has usually resulted in a hard landing if we go by history.

The odds of avoiding one this time were on the rise, but the events in the last few weeks have changed a lot of expectations.

Goldman Sachs raised its odds of a recession this calendar year from 25 percent to 35 percent, citing recent volatility and near-term stress stemming from SVB's collapse.

The bond market also concurs with the inversion between the two-year and 10-year treasury yields (an indicator of an incoming downturn) flashing its largest recession warning in 42 years in early March.

JP Morgan strategist recently said that the US economy is likely on track for a hard landing scenario, with recent bank crises significantly raising the odds of a recession.

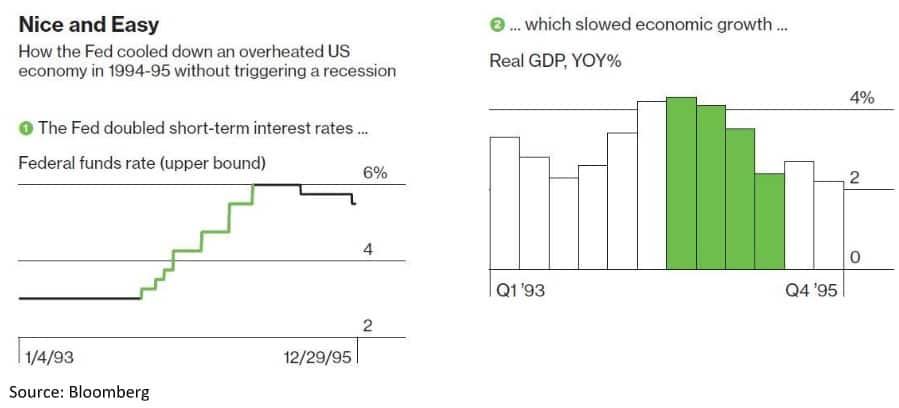

It is worthwhile to look back and check whether the Fed has ever succeeded in cooling down the US economy by hiking rates without causing a recession. The answer is yes, in 1994-95.

PSU bank stocks have been suffering this year so far. Have they lost their mojo? What is the outlook for PSU banking stocks?

We are positive about the banking sector. The sector remains healthy in terms of capital position, liquidity, and provisions.

Sector valuations remain attractive (as one-year forward P/B Nifty Bank trades at a nearly 25 percent discount to Nifty50 versus a long-term average of nearly 11 percent discount), especially in the context of strong earnings growth, healthy loan growth and margins.

However, we continue to prefer large private banks as they are more likely to deliver healthy NII (net interest income) growth along with benign credit cost outcomes in FY24E.

Valuations for most large private banks are at or below mean and hence they offer better risk-reward at this stage.

In the aftermath of the recent collapses of banks in the US followed by a newly minted UBS-CS merger, we saw selling by FIIs and a good part of that came in financials.

PSU banks being higher beta and perceived to be higher risk than large private banks, saw a bigger correction.

While we are not negative on PSU banks, our preference in the current environment is for large private banks, where we have a higher certainty of NII growth, liquidity, ROA, ROE, and lower credit costs.

What sectors one should invest in at the current juncture? Please explain your views.

We are positive on banks, autos and manufacturing. In our view, the banking sector’s balance sheet is amongst the strongest it has been in the last 10 years, especially in terms of credit cost potential.

Further, the system credit growth has surprised all with a 10-years high number of 17.4 percent YoY till the fortnight ended December 2, 2022, indicating continued improvement in economic activity.

Improving fundamentals and earnings visibility coming at a time when the sector bore the brunt of record FII selling as it forms nearly one-third of the FII portfolio.

Auto: Volumes are improving across segments after a lull of a few years. Over the last few years, the sector had suffered from Covid, rising raw material prices, rising crude oil prices, higher insurance costs, and semiconductor chip shortages.

Most of these issues have been settling down. As a result, the sector can likely see improvement in volumes, realizations, and margins.

Manufacturing: While public capex led by the government is already on, the private capex is expected to pick up soon.

Drivers of capex spend: Increasing capacity utilization (exceeded 75 percent), deleveraged corporate balance sheets (BSE500 cos Net Debt to EBITDA is down from 3.4 times to 2.3 times in the last six years), strong revenue collection by the government and softening commodity prices are aiding capex activity.

The manufacturing sector’s share in the Indian economy reached the pre-covid level of nearly 18 percent of GVA (gross value added) in FY22 and is poised to hit an all-time high in the medium term.

We observe nascent signs of capex cycle recovery, with recovery in the real estate cycle, government policy initiatives (especially the PLI schemes), continued FDI inflows and the China+1 related export opportunities.

What are your views on the new-age tech firms? Do you see value in them? Are they buy-worthy?

Most of the new-age companies came in with IPOs at a time when the market was ready to assign any valuation for growth prospects, without too much attention to profitability.

In the wake of rising inflation and quantitative tightening, the risk appetite globally nose-dived over the last year or so.

As a result, most of these new-age companies were forced to rework their strategy towards profitability.

Bull market rally in technology and new-age sectors and subsequent burst is not a new phenomenon and was last observed during the 2000 bull market.

History shows that some of them go on to become multi-baggers even from the high levels of the previous peak, while others lost significant value.

The key to identifying them lies in their path to profitability, which in turn depends upon their execution and ability to change the way their customers carry out their functions.

In the current bouquet of new-age companies, some are changing the way we make payments, some are changing the way we consume food, and some are changing the way we shop for specific products.

Each of these businesses has shown the capability to build strength. Over time, as they demonstrate the ability to scale up and grow profits, they are likely to find a place in most portfolios.

Disclaimer: The views and recommendations given in this article are those of the expert. These do not represent the views of MintGenie.