Amid concerns of recession in the US as well as overall rising inflation, the June quarter results of FY23 (Q1FY23) in the Indian IT sector are likely to be dragged by margin and cross-currency headwinds.

IT Sector Result Preview: Margin and cross-currency headwinds may have dragged June quarter numbers

TL;DR.

MOSL's IT Services coverage universe should witness modest median revenue growth in Q1FY23E, rising 3.3 percent QoQ. Growth in profit, however, will be impacted by wage hikes and supply-side pressure, despite a depreciation in the rupee, it added.

According to a report by domestic brokerage house Motilal Oswal (MOSL), management commentary on demand will remain under focus across both Tier I and Tier II companies in the IT Services space.

"While our recent discussions with managements indicate continued momentum in spends on technology services, we expect initial signs of an impact in sectors like Retail and Manufacturing in Q1FY23," the brokerage noted.

The first result from the sector will come in on July 8, when Tata Consultancy Services (TCS) will announce its numbers. Infosys will announce its results on July 24, the last among the top four IT firms.

According to MOSL, it's IT Services coverage universe should witness modest median revenue growth in Q1FY23E, rising 3.3 percent QoQ. Growth in profit, however, will be impacted by wage hikes and supply-side pressure, despite a depreciation in the rupee, it added. Profit across MOSL's IT coverage universe is likely to decline 2.8 percent QoQ.

Tier I companies are likely to deliver revenue growth in a narrow range (2.3-3.9 percent QoQ CC), while Tier II players will grow in the 1.9-5.3 percent range, excluding Persistent Systems, which is estimated to grow 9.5 percent QoQ due to a meaningful contribution from recent acquisitions, noted MOSL.

It also sees a limited change in the FY23 revenue growth guidance of Infosys, HCL Tech, Coforge, and L&T Tech in Q1, given the unchanged demand commentary.

Constant Currency (CC) revenue growth

Among individual stocks, the brokerage forecasts Infosys leading with revenue growth of 3.9 percent QoQ CC, followed by TCS/HCL Tech at 3.4 percent/3.3 percent. Meanwhile, Tech Mahindra and Wipro are expected to deliver 2.8 percent and 2.3 percent QoQ CC growth, respectively.

Among Tier II players, MOSL expects good revenue traction at Persistent Systems (up 9.5 percent QoQ CC). It also forecasts Coforge and MindTree to grow by 5.3 percent and 4.6 percent QoQ CC in Q1FY23.

Profit after tax (PAT)

MOSL expects its Tier-I IT coverage universe to see a 2.5 percent QoQ decline in PAT growth, while it will grow by 5.6 percent YoY.

Among stocks, TCS, Infosys and HCL Tech should deliver a PAT growth of 11.2 percent 9.8 percent and 4.6 percent YoY, respectively, while Wipro and Tech Mahindra will see a 9.2 percent and 10.4 percent YoY decline in PAT due to a compression in margins, noted MOSL.

Meanwhile, among Tier-II players PAT growth of 21 percent YoY is seen, but a decline of 6.3 percent QoQ. Coforge, Mindtree and L&T Tech are expected to lead the Tier II pack in terms of YoY PAT growth, while

Margin Impact

The brokerage sees muted margins in Q1FY23 due to of wage hikes and continued supply-side pressure as attrition is still elevated. The same for Tier I companies will be in the -80 bps to -190 bps range (with the exception of HCL Tech), however, the Tier II pack will operate in a wider range (-30 bps to -290 bps), it said.

"Among Tier I players, Tech Mahindra will see the highest impact (-190bp) due to higher employee costs and seasonality, while the wage hike impact for TCS, Infosys, and Wipro will be in a narrow range. HCL Tech should see some support due to seasonality in Products and Platforms," the report suggested.

In the Tier II pack, Cyient and Zen Tech will see a significant margin dip (-290 bps/-250 bps) on elevated employee costs and weaker growth, followed by L&T Infotech/Coforge with a 220 bps/210 bps hit. Meanwhile, L&T Tech, MindTree, and Persistent systems should see a more modest margin impact as their wage hike cycle in Q2FY23, said MOSL.

It further pointed out that attrition should remain at elevated levels and supply will continue to stay constrained, leading to elevated replacement costs. Moreover, a higher intake of freshers will result in lower employee utilization, which will further constrain profitability.

Outlook, Strategy and Top picks

With valuations correcting meaningfully over the last six months, the brokerage maintains a positive stance on the IT Services sector due to a favorable medium to long-term demand outlook. However, it anticipates an impact in H2FY23 and FY24 due to elevated inflation and an economic slowdown in both the US and Europe.

"We expect near-term pressure on valuations to continue as the worsening macro commentary is expected to flow down to industry deal flow and revenue over the next few quarters, leading to a moderation in the corporate commentary. Any consequent correction should be utilized to raise allocation to the sector," it said in the report.

MOSL continues to prefer Tier I players over their Tier II counterparts, given their relative valuation attractiveness and diversified client portfolio. Among Tier I players, It likes Infosys, HCL Tech, and TCS.

Among Tier II IT, it prefers Mphasis and L&T Tech.

Due to a weak near-term outlook, it cut FY23/FY24 INR EPS by 2-5 percent, despite a positive 300-400 bps impact from a lower rupee (79/USD). The impact on earnings will accrue from weaker revenue growth as it continues to see support to margins from a large fresher intake and a partial price increase, highlighted MOSL.

It added that the commentary on demand, the impact of an upward price revision, and a weakening macro-economic outlook on deal conversion will be key monitorables to look for.

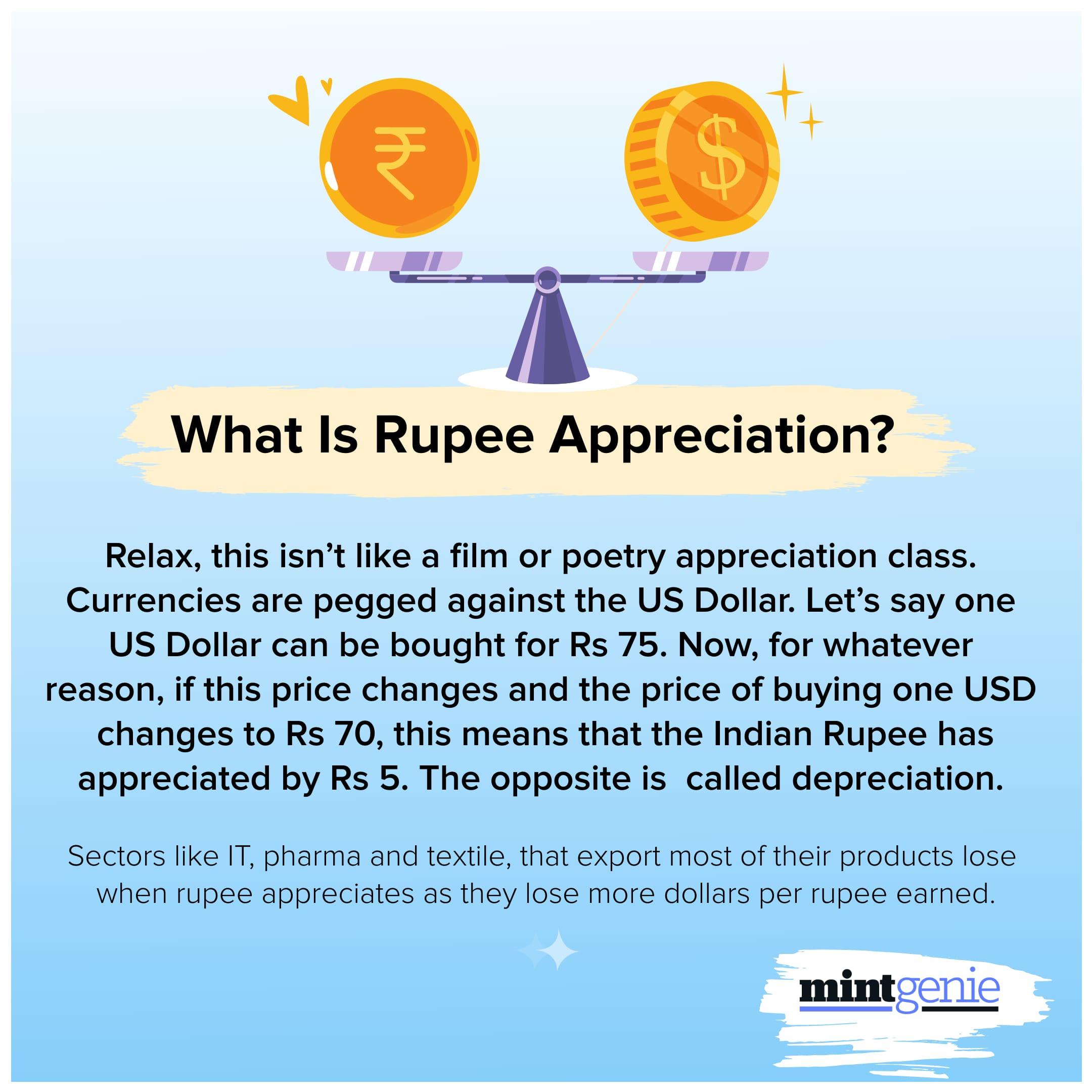

What is rupee appreciation?

First Published: 04 Jul 2022, 12:58 PM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

What investments you can make to ensure that inflation doesn’t ‘swindle you’?

Team MintGenie