Sun Pharmaceuticals and Syngene are global brokerage house Jefferies' top picks in the pharma space while it downgraded Biocon, Cipla and Laurus Labs.

Jefferies says big pharma firms to get bigger; lists Sun Pharma and Syngene as top picks, downgrades Biocon, Cipla

TL;DR.

Jefferies expects big companies and big brands to become bigger as consolidation gathers pace in the pharma sector.

"We rate Sun Pharma and Syngene as Buys and our top picks," said the brokerage.

The $27 billion domestic pharma industry has structural growth drivers in place and is well-placed to achieve low double-digit growth in the coming years, predicted Jefferies. As per the brokerage, increased spend on medicines as the population starts to age in the coming decade and a rising share of chronic ailments such as cardiac disease, diabetes, and cancer should help sustain double-digit growth.

Jefferies expects big companies and big brands to become bigger as consolidation gathers pace in this sector. For chronically focused companies, it sees Earnings Before Interest, Taxes, Depreciation, and Amortisation (EBITDA) margins improving gradually.

It further noted that the CRO/CDMO outsourcing market has high entry barriers, and is estimated to reach a size of $200 billion by 2025 (11 percent CAGR). As western firms are looking to diversify their supply chains, it believes Indian companies with global capabilities stand to gain. Such companies have the potential to achieve mid-teens revenue growth on a sustained basis with an improving margin profile, added Jefferies.

Amongst generics, Sun Pharma's specialty pipeline ramp-up along with strong positioning in India and emerging markets ensures sustainable double-digit revenue growth and a best-in-class margin profile, Jefferies pointed out.

Meanwhile, it has lowered its ratings on Cipla (non-consensus) and Biocon from Buy to Hold. While the US pipeline for Cipla and Biocon provides a sustainable revenue stream, delays in key approvals for FY24 pose downside risk to earnings, and leave limited upside for these stocks from a 12-month perspective, it said.

Dr Reddy's is in the process of rebuilding its US pipeline, and while its evolution is some time away, current valuations leave limited downside potential, added the brokerage.

Amongst the outsourcing names, it believes Syngene is at an inflection point. Capex of over $400 million incurred over the last four-five years is starting to bear fruit with recent big contract wins, noted the brokerage.

Further, it cut FY24-25E EPS for Laurus Labs by 14/22 percent, and downgraded it from Buy to Hold, as it expects margin pressure in FY24E due to lower CDMO sales.

Let's see what the brokerage has to say about the different pharma stocks in its coverage:

Alkem Labs | Rating: Underperform

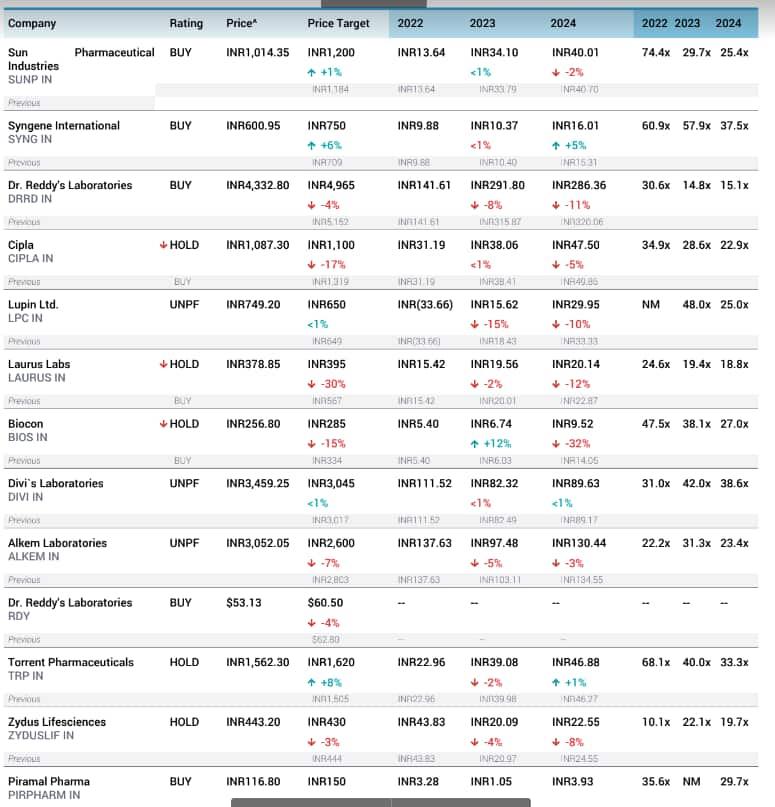

The brokerage has reduced the target for the stock by 7 percent to ₹2,600 from ₹2,803 earlier. The new target price indicates a downside of 14 percent from the current level. "We expect double-digit revenue growth in India, but EBITDA margins will remain under pressure," the brokerage said in its report.

Biocon | Rating: Downgraded to 'hold' from 'buy'

The brokerage cut its target price by 15 percent to ₹285 from ₹334. The new target price indicates an upside of 13 percent. The recent acquisition of Viatris front-end and vaccine partnership with Serum Institute will push revenue growth. However, the increasingly competitive landscape for biosimilars and delays in upcoming launches impact the core business earnings. Approvals for Bevacizumab, bAspart, market formation around the launch of Humira and US FDA action on Bangalore and Malaysia plants will be things to watch out for, said Jefferies.

Cipla | Rating: Downgraded to 'hold' from 'buy'

The brokerage cut its target price by 17 percent to ₹1,100 from ₹1,319 earlier. The new target price implies a potential upside of just 3 percent. As per the brokerage, the delay in key US approvals leads to a 5-6 percent EPS cut for FY24-25. US pipeline is solid but timely approval is key to sustaining current valuations.

Sun Pharma | Rating: ‘Buy’

The brokerage has raised its target price to ₹1,200 from ₹1,184 earlier. The new target implies an upside of 16 percent. Specialty pipeline ramp-up should drive positive margin surprise, said Jefferies, adding that Sun Pharma is its top pick in the sector. In-licensing deals for specialty products will be monitored, it added.

Torrent Pharma| Rating: ‘Hold’

The brokerage raised the target price of the stock by 8 percent to ₹1,620 from ₹1,505 earlier. The new target indicates an upside of 4 percent. Current valuations adequately factor the earnings growth over the next two years, stated Jefferies, adding that the synergy benefits from the recent acquisition of Curatio will be monitored.

Laurus Labs | Rating: Downgraded to ‘hold’

The brokerage has reduced the target price of the stock by a massive 30 percent to ₹395 from ₹567 earlier. The new target implies an upside of 10 percent. "High price erosion in ARV business and uncertainty regarding new contract wins leads to near to challenges in ARV business. Lower paxlovid sales are likely to put pressure on margins for the company in FY24E," noted Jefferies.

Syngene International | Rating: ‘Buy’

The brokerage has raised the target price of the stock by 6 percent to ₹750 from ₹709 earlier. The new target implies an upside potential of 21 percent. At an inflection point, capex of $400m+ incurred over the last four-five years is starting to bear fruit with a recent big contract win. This is a testimony to Syngene's capabilities, and provides visibility on improved asset utilization, said Jefferies. It expects Syngene's EBIDTA to double over FY22-25E.

Piramal Pharma | Rating: ‘Buy’

The brokerage initiated coverage with a ‘buy’ call and a target of ₹150, implying a potential upside of 28 percent. The recovery in CDMO revenue starting 2HFY23 (a seasonally strong period anyway) should drive operating leverage benefit, said the brokerage, adding that its valuations are at a steep discount to peers. The turnaround in CDMO operations is the key catalyst, it added.

Source: Jefferies

First Published: 16 Jan 2023, 06:10 PM IST