Post a spectacular quarter reported by the banking sector in Q2, brokerage house Kotak Institutional Equities (KIE) has raised target prices of select public sector lenders in its coverage on the back of strong business performance. The brokerage believes that tier-2 banks such as public sector and regional banks have better upside than the frontline banks.

Kotak Institutional Equities believes PSU lenders have better upside; Raises target price for select banks

TL;DR.

Post a spectacular quarter reported by the banking sector in Q2, brokerage house Kotak Institutional Equities (KIE) has raised target prices of select public sector lenders in its coverage on the back of strong business performance.

The brokerage, however, remains bullish on the entire banking space and maintains the investment thesis that we are still early in the credit cycle currently and visibility of a sharp deterioration in asset quality appears to be low.

"We upgrade fair values for banks under coverage partly to reflect the greater confidence in earnings led by lower credit costs, better-than-expected loan growth, and consequently higher operating profit growth. The increase in fair values is primarily in the second tier banks (public banks and regional banks), which have traded below or closer to book value where we are witnessing most of the improvement in business performance," said the brokerage.

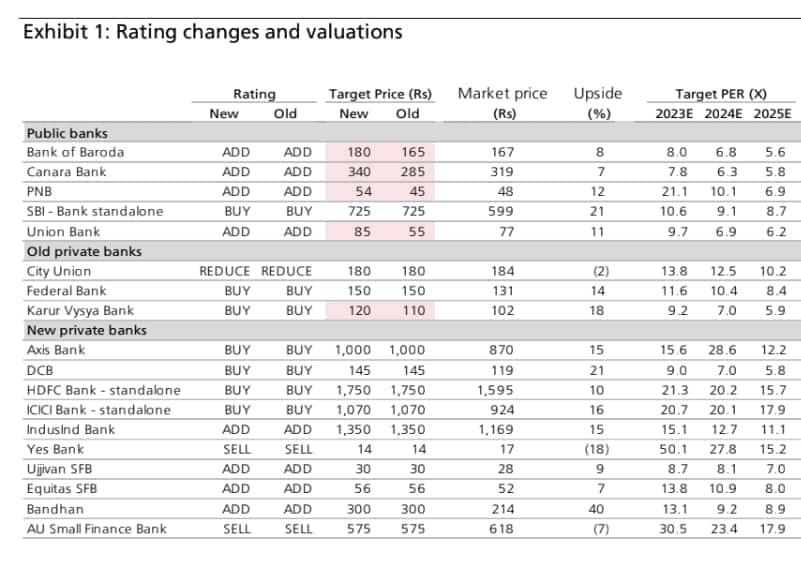

The brokerage increased the target price of Bank of Baroda to ₹180 from ₹165 earlier. The new target implies an upside of 8 percent from its current market price. It also upped the target price of Canara Bank to ₹340 (from ₹285 earlier), indicating a potential upside of 7 percent now. Punjab National Bank's target was also risen from ₹45 earlier to ₹54, implying a potential 12 percent upside. Finally, the target price of Karur Vysya Bank was upgraded to ₹120 (from ₹110 earlier), 18 percent upside seen.

Here's a list of all rating changes and valuations

Source: Kotak

Stock price trend

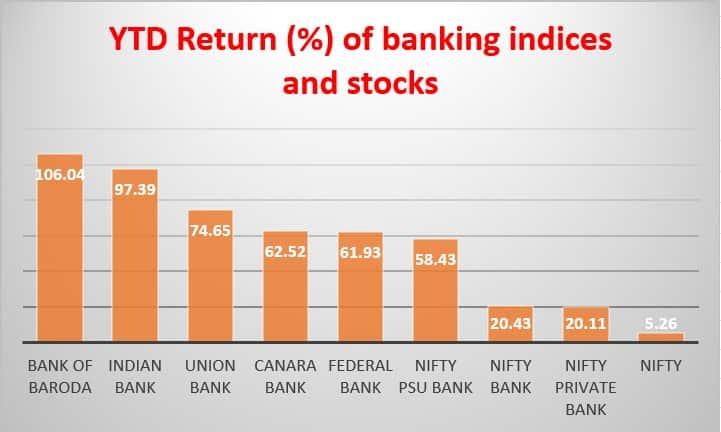

The brokerage further pointed out that there has been a very sharp increase in price performance in these banks over the past few years. Regional banks, public banks and non-frontline private banks have seen a sharp increase in prices and are outperforming the frontline private banks.

In the last 1 month, Nifty PSU Bank has jumped 22 percent as against a 4 percent rise in Nifty Bank. Meanwhile, on a YTD basis, the PSU Bank index has soared 60 percent versus a 21 percent rise in Nifty Bank and in the past 1 year the Nifty PSU Bank has advanced 46 percent as against a 15 percent rise in Nifty Bank.

In 2022 YTD, among PSU banks, Bank of Baroda has surged the most, giving multibagger returns, up 107 percent followed by Indian Bank (up 99 percent), Union Bank (up 78 percent), Canara Bank (63 percent), Bank of India (58 percent), and UCO Bank (58 percent). Other PSU Banks including Bank of Maharashtra, Punjab National Bank, SBI, and Central Bank of India have also given double-digit returns in this period, up between 20-45 percent.

Meanwhile, among frontline banks, HDFC Bank and Kotak Bank have given single-digit returns in 2022 YTD, up 9 percent and 8 percent, respectively. Meanwhile, ICICI Bank has added 25 percent and Axis Bank is up 30 percent in this period.

Nifty PSU Bank

Investment thesis

The brokerage said that its positive investment thesis at this point for the sector is relatively straightforward.

"We believe that the sector is still in the very early stages of recovery post-Covid. We are currently seeing a strong intent to lend from the providers of debt capital. Banks, especially public banks, which had been affected by the corporate NPL cycle, have come back strongly in recent quarters. This has resulted in credit costs declining sharply in recent quarters and strong improvement in headline asset quality ratios. We also see public banks, regional banks and NBFCs showing greater comfort to grow their balance sheet as well," it explained.

It also pointed out that with a strong flow of funds, the probability of non-performing loans (NPL) ratios declining further is still high, which implied that the lower credit costs across banks could be visible for a much longer period as well.

KIE also mentioned that this decline in credit costs implies that RoEs (return on equity) are likely to move closer to the industry average fairly quickly from here and the dispersion of RoEs, which was quite high in recent years to converge for most banks. It has also marginally changed its cost of equity estimates as well to capture the same.

Macro risks

KIE acknowledges that the macro risks are still quite high and may warrant a change in view. However, it is hard to build an investment thesis that is currently dependent on a possible slowdown till it can assess the impact of that slowdown, it noted.

"It does appear that the growth could be slower rather than a repeat of the corporate NPL cycle. We have seen that the slowdown caused by the capex slowdown was different from the slowdown that was caused by Covid on banks. Public banks or large private banks had a negligible impact during the Covid cycle while they were deeply impacted during the corporate slowdown. As such, we are yet to see an asset bubble currently either in the corporate sector through a large capex cycle or in the real estate sector. These are usually sectors that can potentially result in a sharp slowdown and consequently result in high loss rates. Note that the loan book has more retail loans in the current cycle and hence, the probability of a higher credit cost appears to be lower. Affordability appears to be quite comfortable despite the recent increase in interest rates," cautioned the brokerage.

Q2 Earnings

The banking sector reported strong September quarter (Q2FY23) earnings, led by healthy loan growth, margin expansion, and continued moderation in provisions. Loan growth was led by sustained traction in Retail and SME (small and medium enterprises) segments, along with a sharp revival in corporate loans.

Only Punjab National Bank (PNB) reported a year-on-year (YoY) decline in its profit after tax (PAT) in the September quarter as provisions for non-performing assets rose. All other banks posted robust profit growth for the quarter under review. In fact, eight of them posted over a 50 percent jump in their Q2 profit.

Outlook

Brokerage house Bank of America Securities (BofA Sec), in a recent report, said, "State-owned banks are now guiding for steady growth - in line with or better than the system. PSBs' aggregate loan growth in FY22 improved to 8.8 percent (versus private banks' 16 percent) - the highest since FY14. More importantly, growth across PSBs was more broad-based across segments."

Meanwhile, Satish Menon, Executive Director at Geojit Financial Services, said, "A deep discount in PSBs valuation and improvement in quarterly results reflecting growth in business, buffer provision, and asset quality led to the rally. The GNPA of PSBs has more than halved from the peak of 14.6 percent in FY18. A huge valuation gap between private and public sector banks created the arbitrage opportunity. However, the gaps have rapidly narrowed, limiting the upside in the short term. While on a long-term basis re-rating is expected to extend.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

YTD return of banking stocks.

First Published: 24 Nov 2022, 12:27 PM IST

Related Stories

Explain Like I am 5

personal finance

Your Questions Answered: How to reach your financial goals, build an emergency fund and much more

International Money Matterspersonal finance

Fixed Deposits: Worried about the penalty on premature withdrawal of FD? Here’s how to avoid it

Kirti Jha