Shares of Kotak Mahindra Bank rose almost 2 percent in intraday trade on BSE on January 23 after the bank released its December quarter scorecard.

The bank on January 21 said its standalone net profit jumped almost 31 percent year-on-year (YoY) to ₹2,791.88 crore in Q3FY23 compared to ₹2,131 .36 crore in the same quarter a year ago.

As Mint reported, Kotak's asset quality improved with gross NPA declining sharply, however, provisions increased during the quarter.

Net interest income (NII) stood at ₹5,653 crore in Q3 of FY23, up 30.43 percent from ₹4,334 crore in Q3FY22.

Net interest margin (NIM) expanded to 5.47 percent in Q3FY23 from 4.62 percent in the same quarter year ago.

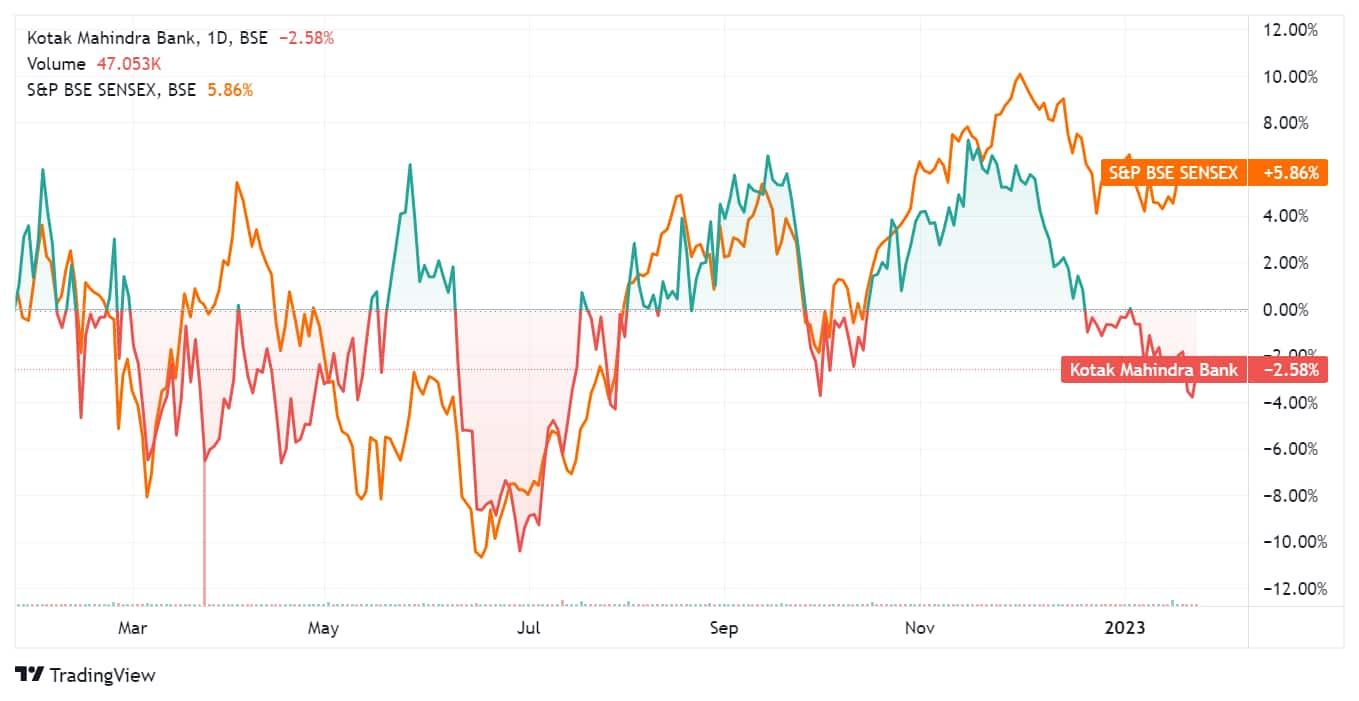

Shares of Kotak Mahindra Bank have been lacklustre in the last one year, underperforming the benchmark Sensex.

Brokerages express mixed views

Brokerage firm Phillip Capital maintained a buy call on the stock with a target price of ₹2,100.

Phillip Capital said Kotak Bank’s Q3FY23 earnings were above expectation largely because of high NII, driven by margin expansion.

It added that the lead impact on asset repricing with liability is yet to follow, doing most of the honours.

"Kotak Mahindra Bank has pressed the growth pedal which is visible in sequential growth number. The bank has geared to invest in capabilities to acquire customers. In the journey to add scale to its business, some of the matrix like the cost to income ratios may witness near term challenge," said Phillip Capital.

"As most of the banks are geared to capture growth opportunity with improving credit behaviour in tight liquidity scenario, we believe the superior liability franchisee would be an important margin driver from hereon," Phillip Capital said.

Nirmal Bang Institutional Equities also maintained a buy call on the stock with a target price of ₹2,121 and said Kotak Mahindra Bank reported solid earnings for Q3FY23, beating its estimates, driven by margin expansion and lower provisions.

"We believe that overall NIM is likely to normalise going forward due to pressure from the higher cost of funds (CoF). Asset quality improved QoQ, driven by lower gross delinquencies. Credit cost was negligible as the bank reversed Rs380mnn of covid provisions. The restructured book declined QoQ, suggesting a positive outlook for asset quality," said Nirmal Bang.

On the other hand, brokerage Emkay Global reduced the rating on the stock to a 'hold' from a 'buy' with a target price of ₹2,000.

Emkay expects Kotak's RoAs to normalise to 2 percent in FY25E from a high of 2.2 percent in FY23E, and RoEs to settle at around 13 percent.

Emkay believes that the impending MD change in Jan-24 will emerge as a key overhang on the stock in the near-to-medium term, as we move closer to the event.

"We trim our P/ABV for the standalone bank to 3 times from 3.5 times earlier, and revise our target price downwards to ₹2,000 (including subs value at ₹550 post the 20 percent discount). We also lower our rating on the stock to 'hold' from 'buy'. Difficulty in mobilising low-cost deposits, management attrition, and asset-quality risk in the unsecured loan book are the key risks," said Emkay.

Brokerage firm Motilal Oswal Financial Services maintained a 'neutral' call on the stock with a target price of ₹2,000.

Motilal said Kotak Mahindra Bank delivered a strong quarter, with healthy loan growth, strong NII, and controlled provisions.

"NIM has expanded further, and the outlook remains buoyant, given the improving asset mix and a higher mix of floating loans. Asset quality remains robust, with a further decline in GNPA/NNPA, while the restructured book remains under control at nearly 0.25 percent of loans. We slightly increase our earnings estimates and expect the bank to deliver a 17 percent earnings CAGR over FY22-25," said Motilal Oswal.

According to a MintGenie poll, an average of 38 analysts have a ‘buy’ call on the stock.

Disclaimer: The views and recommendations given in this article are those of broking firms. These do not represent the views of MintGenie.