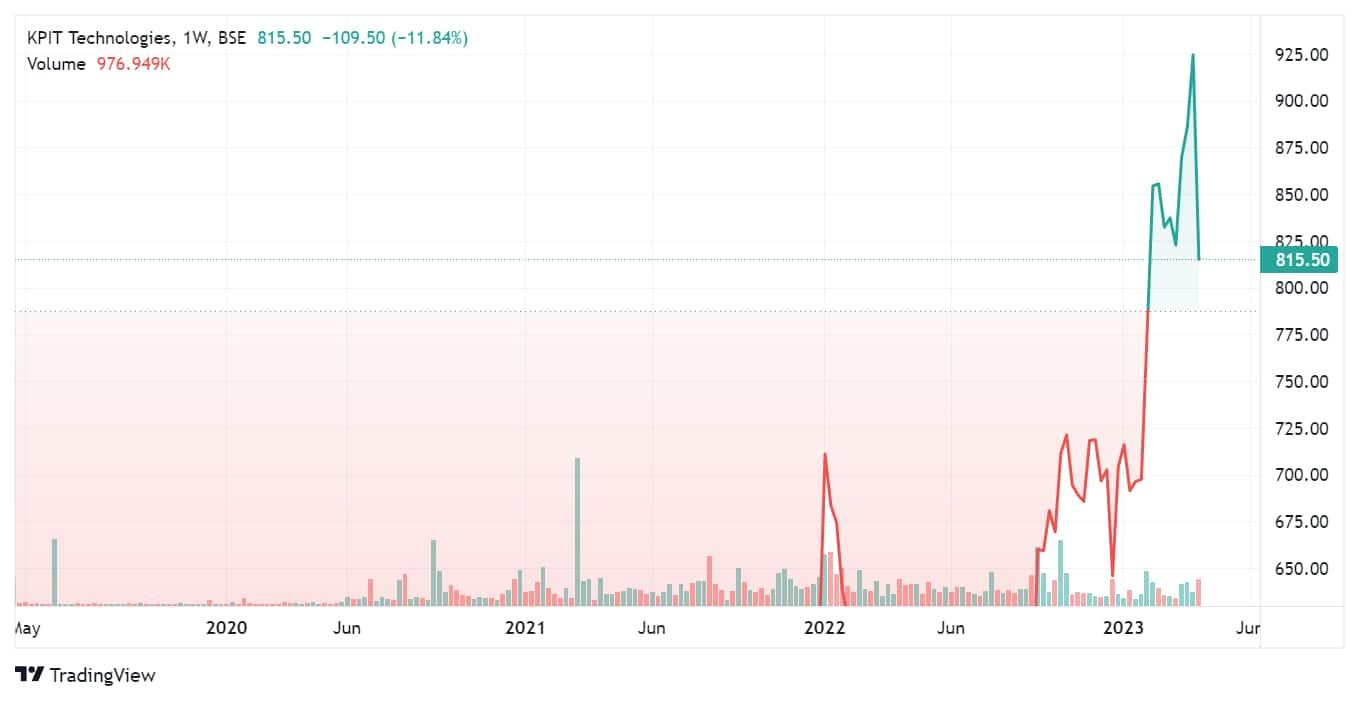

After surging over 2200 percent from its COVID low and almost doubling investor wealth in less than one year, midcap IT firm KPIT Tech is likely to fall 35 percent in the next 1 year, according to global brokerage house JPMorgan.

The brokerage has initiated coverage on the stock with an 'underweight' call and a target price of ₹520, implying a downside of 35 percent from its current market price of ₹809.50, as on April 3, 2023. Post the release of the JPMorgan report, the stock tanked over 12 percent on April 3.

Just in the previous session, on March 31, the stock had hit its record high of ₹946.50.

"A combination of lower structural margins, risks from the single vertical presence and high client concentration, and excessive valuations drive our UW rating on KPIT," said the brokerage.

From its COVID low of ₹34.35, hit in March 2020, the stock has skyrocketed as much as 2256 percent to ₹809.50 till date.

In the last 1 year, it is up 30 percent while it rose 15 percent in 2023 YTD. It has gained 8.3 percent in January, 8.7 percent in February, and 11.5 percent in March 2023, however, lost 11.9 percent in the 2 sessions of April after the JPMorgan report.

The brokerage noted that it likes KPIT’s focus on the fast-growing auto vertical but advises investors to wait for an attractive entry point. Based on growth expectations vs current valuations, its pecking order in Engineering and R&D (ER&D) services is Persistent Systems>L&T Tech>Tata Elxsi>KPIT.

Key de-rating catalysts for KPIT are slowing growth beyond FY24 to less than 20 percent and scarcity premium going away with the announced IPO of Tata Technologies (88 percent auto revenues), it cautioned. JPMorgan believes KPIT would need to win large deals every year in order to maintain growth of over 20 percent, which it sees as a challenge since the auto industry is cyclical. Hence it would be too optimistic to give KPIT the benefit of doubt, it added.

"The stock is trading at 50x 1 yr fwd PE and a reverse DCF implies a 24 percent revenue CAGR over the next decade which we believe is overly optimistic given that on a smaller base it is achieving 24 percent growth (FY23E). Our Rs520 PT is based on a 25x 1yr fwd P/E which we think is justified by the strong earnings growth, and implies a 14 percent revenue CAGR over the next 10 years on our DCF," it highlighted.

The brokerage further pointed out that the stock has been a multi-bagger over the last 3 years - up over 2000 percent since the lows of Mar’20. "This has been driven by consistent EPS upgrades over this period as the company kept on beating consensus expectations on margins and also has been consistently upgrading its revenue growth as well as margin guide during FY22 and FY23. Its Ebitda margin trajectory has been impressive over the last three years (18.8 percent in 9MFY23 vs 13.7 percent in FY20) helped by a combination of strong operating leverage benefits and improved offshoring," it explained.

However, for a stock flirting with 50x 1 yr fwd PE (most expensive in India IT and ERD sector), JPMorgan feels that the burden of the valuation is too high. The ask rate on revenue growth is 24 percent for the next 10 years based on reverse DCF and hence growth less than 20 percent beyond FY24 could drive a potential de-rating.

"We believe it is too optimistic to give the benefit of the doubt that the company can maintain >20 percent growth for the next 5-10 years given its dependence on a single vertical and high client concentration that always puts risks on the downside. On margins, the company has already mentioned that it aspires to reach a 20 percent Ebitda margin by FY25; consensus is already at 19.6 percent and hence we see no room for positive surprises on margins," it noted.

In the December quarter, the IT firm's consolidated net profit jumped 43.5 percent to ₹100.49 crore. Meanwhile, its revenue from operations rose 47.4 percent to ₹917 crore.

EBITDA stood at ₹169.87 crore in Q3 FY23, up 47.44 percent YoY. EBITDA margin was consistent at 18.5 percent in Q3 FY23. The IT company said that the margin was flattish post impact of deal-related and integration-related expenses during the quarter, said the firm.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.