Laurus Labs reported a 23% fall in its consolidated net profit for the fourth quarter ended March 31, 2022, at ₹230 crore.

Laurus Labs Result Review: Expansion plans enough to lead future growth?

TL;DR.

Results were impacted by lower sales of ARV APIs and formulations due to stocking at channel partners and it’s expected to improve. However, Strong momentum in their CDMO business continued this quarter with over 60% growth and seen healthy rebound in API business (ex-ARV) with activity levels picking up.

Revenues rose just 1%, at ₹1,425 crore in the same period while profit after tax (PAT) fell 25% on the back of rise in expenses by 11%, the company said.

The company's PAT stood at ₹302 crore in the given quarter and expenses were at 1,124 crore.

Pure profits, or EBITDA, too, fell 17% and EBITA margins shrunk nearly 28%, it said.

The company operates in the segment of generic APIs & FDFs (formulations), custom synthesis and biotechnology. Major focus in APIs is on ARV, oncology, and other APIs.

The results of the current financial year so far reflects operational resilience overall with better mix and sustained profitability despite of lower revenue from ARV APIs and formulations. Results impacted by lower sales of ARV APIs and formulations due to stocking at channel partners and it’s expected to improve hereon. However, Strong momentum in their CDMO business continued this quarter with over 60% growth and seen healthy rebound in API business (ex-ARV) with activity levels picking up. Company continues to sharpen their execution as they focus on positioning their businesses for sustainable long-term growth.

• Company has 11 manufacturing units (six FDA approved sites) with 73 DMFs, 31 ANDAs filed (15 Para IV, 10 first to file) and 184 patents granted

• Laurus acquired Richore Life Sciences to diversify in area of recombinant animal origin free products, enzymes as well as building biologics CDMO

Key growth parameters

• Synthesis: Well-positioned to meet fast growing global demand for NCE drug substance and drug products. Setting- up dedicated R&D centre (operational FY23) & three greenfield manufacturing units (FY24, FY25)

• Formulations: Product launches in anti-diabetic (FY23) & CV portfolio (FY24) in US & Europe with market opportunity at ~ US$45 billion. Brownfield expansion (Unit-2) by Q1FY23 taking total capacity to 10 billion units

• API: Robust order-book in anti-diabetic, CV & PPI amid capacity expansion in high growth therapeutics with total reactor volume of +7000KL by FY23

• Biologics: Expanding the biologics CDMO at scale. Commercial scale-up of the new fermentation capacity (food proteins). Plans to add 1 million litre fermentation capacity in Phase 1

What is EBITDA

Financial snapshot

| FY22 (In ₹Crore) | FY21 (In ₹Crore) | Year-On-Year | |

| Revenues | 4,936 | 4,814 | 3% |

| Gross Margins | 55.6% | 55.2% | 40 basis points |

| EBITDA | 1,436 | 1,573 | -9% |

| % to Revenue | 29.1% | 32.7% | -360 basis points |

| Net Profit | 828 | 984 | -16% |

| Earning Per Share | 15.4 | 18.3 | -16% |

Revenues grew at moderate 3% but delivered strong mix improvement led by significant progress in non-ARV business, especially CDMO-Synthesis. Gross Margins: 55.6%, expanded 40 bps YoY based on better business mix. EBITDA: ₹ 1,436 Cr, decreased by 9% YoY resulted in Margins of 29.1% due to lower ARV API sales.

Increase in Research and Development expenses

| (in crore) | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 |

| R&D expenses | 8.53 | 13.38 | 11.35 | 16.59 | 16.02 | 18.4 | 20.2 |

| % of sales | 4.8% | 7.1% | 5.6% | 7.4% | 5.7% | 4% | 4% |

• Committed to invest 4% of the Topline. Product Specific Approach based on Complexity and Scale

• Future R&D pipeline Addressable market at US$ 45 billion+ ( more than 70% of opportunity in non-ARVs space).

• Total of 9 Filings made in Developed market (vs. 8 in FY21)

• Total of 73 DMFs were filed as on Mar-22 (vs. 61 in FY21)

• FY22 R&D spend +10% YoY to ₹ 202 cr (4% to Sales)

Laurus is evolving as a strong vertically integrated player with strong order book visibility and incremental traction from custom synthesis.

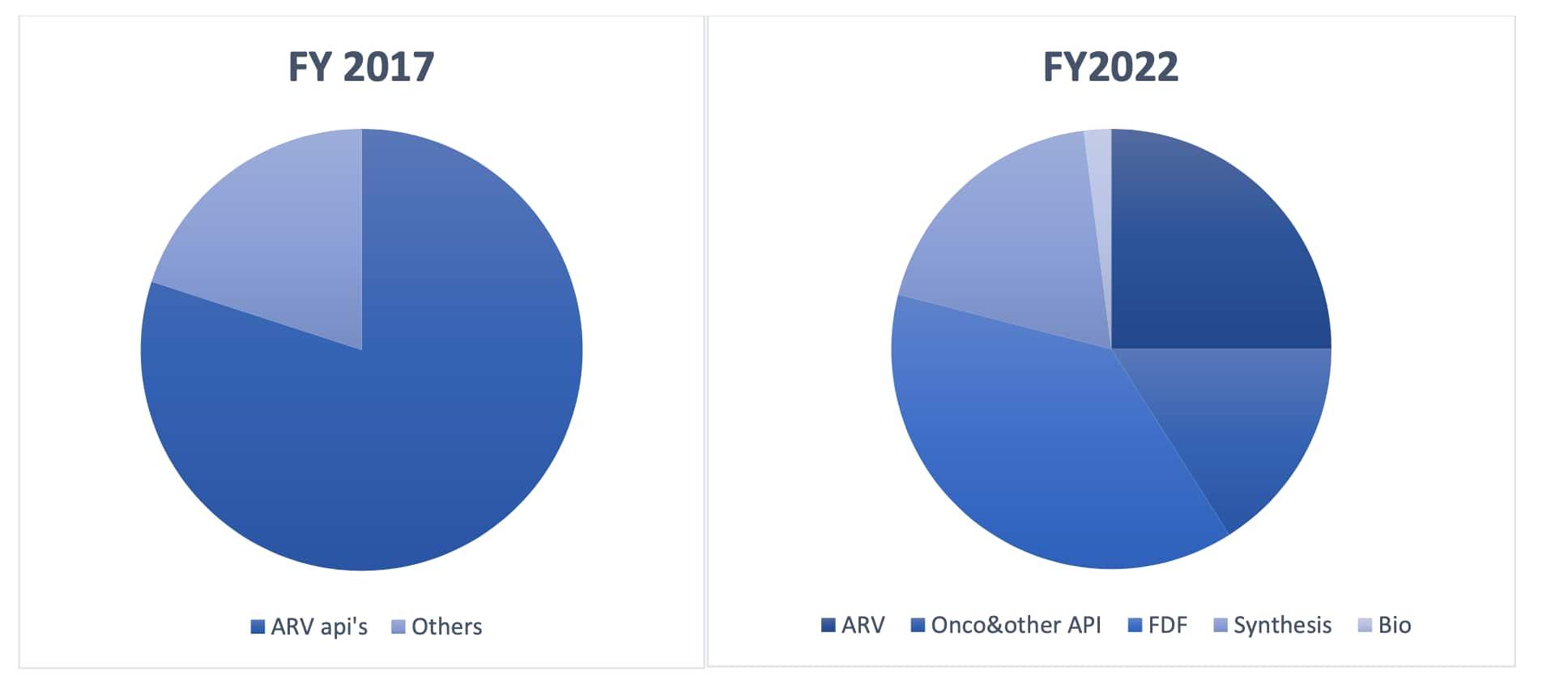

Segment-wise breakup

Laurus Labs' segment-wise breakup

Expansion plans to boost growth

Company plans to foray into new technologies such as

• Recombinant Proteins (FY21)

• CAR-T Cell therapy (FY22)

Continued Organic Investment in manufacturing asset, Integrated approach across portfolio, Strong quality, and

leadership team. One of their Key FY25/26 goal includes ~25% of revenues from CDMO synthesis.

New capacities are brought online. Company has Increased Reactor volumes to ~6 million Litre and expect FDF capacity to reach 10 billion units before June’22. Progress on future projects on Schedule for long-term success. Deepening multi-site manufacturing capabilities. Well-positioned to meet fast growing global demand for NCE drug substances and drug products.

Future backed by new project delivery, pipeline expansion and favourable market tailwinds in CRAMS has led to company targeting 25% revenues from Synthesis by FY25. Laurus has multiple planned capacity expansions in portfolio based on complexity and scale and has set an aspirational target of US$1 billion revenues in FY23.

Future plans at a glance

Formulations:

• Retain market share gains in ARV portfolio including few potential launches in 2L ART.

• Create niche product pipeline for the developed markets backed by in-house API strength.

• Strong pipeline (US, EU) >US$45bn mkt opportunity; Diabetic & CV portfolio monetization from FY23.

• Brownfield expansion – To be operational in coming months

API:

• Enhance positioning on HP APIs & Scaling up of Anti-diabetic, CV & PPI portfolio supported by demand-based capacity expansion.

• ARV APIs: Gradual recovery expected while maintain leadership position in current product line and increased developed market supplies.

Synthesis:

• Exciting outlook backed by new project delivery, Pipeline expansion & favorable market tailwinds.

• Leverage integrated capability in DS & DP to deepen existing relationship & Win new Clients.

• Building dedicated R&D center (operational FY23/FY24) & 3 Greenfield manufacturing unit (FY24/25).

• Strengthen presence in Nutraceutical & Cosmeceutical area

Biologics:

• Growth driven by new capacity which came on line in FY22/FY23 & improved Synergies with Parent.

• Future expansion on track to create 1 million liters fermentation capacity.

• Expand the biologics CDMO at scale in the long term

Shuchi Nahar is a Certified Research Analyst. She can be found on Twitter at @shuchi_nahar

First Published: 04 May 2022, 08:46 AM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

What is the CAGR? Is it a better index to assess the performance of your investment?

Vimal Joshi