After a weak September, Indian markets rebounded to rise around 6 percent in the month of October. The rally was led by positive global cues like softening of crude prices, robust festival demand as well as an improvement in the overall economic situation.

Markets rise 6% in Oct after a weak September; What should be your strategy now

TL;DR.

As per Axis Securities, in the near term, the Indian market will continue to follow the Q2FY23 earnings, macroeconomic data, and the outcome of the central bank’s meeting, which is scheduled during the first week of November 2022.

Furthermore, on the last working day of October, the broader Nifty50 index also reclaimed its 18,000 mark. However, certain headwinds like the US Fed's hawkishness, neutral FII inflows, and fears of recession continued to hover around the domestic markets.

After the 75 basis points rate hike in September, the Fed now looks all set to hike rates by another 75 basis points in November 2022 and 50 basis points in December 2022.

Sectors

In October 2022, all sectoral indices closed on a positive note, except FMCG. The biggest recovery was seen in the Baking stocks, especially the PSU banks on account of their robust quarterly performance led by superior asset quality trend and the pickup in credit growth. Some recovery was also seen in the beaten-down IT sector which reported a robust set of numbers, driven by large deal wins and notable demand for digital transformation. However, pressure continued on the margin front on account of higher travel costs and wage hikes.

The Nifty PSU Bank index surged the most in Oct, up over 15 percent followed by Nifty Bank, which soared 7 percent and the IT index, which rallied 6.5 percent. Meanwhile, the private bank index advanced 6.3 percent, the oil and gas index gained 5.6 percent and the auto index added 5.4 percent for the month. Realty, metals and pharma sectors were also up between 1.8-3.5 percent for this period.

Only the FMCG index was in the green, down 0.2 percent.

Broader markets

Furthermore, in the last one month, largecaps outperformed the broader market by healthy margins, primarily due to the positive FII flows during the month. Nifty Midcap and Nifty Smallcap indices rose around 2.5 percent each versus a nearly 6 percent jump in Nifty50.

Q2 earnings

The month saw a number of September quarter earnings. Overall Q2FY23 earnings were in line with analyst expectations so far. While the expectation on the revenue front was largely met, earnings miss was seen in export and commodity themes.

"The Banking sector held the performance and accounted for most of the incremental growth in the corporate earnings while cyclical sectors including Metals, Cement, and Oil & Gas were the biggest laggards due to lower realization and higher Raw Material costs during

the quarter," said brokerage house Axis Securities in a note. On a positive note, corporate margins are likely to stabilize in H2FY23 and may undertake a path of moderation with cool-off seen in the majority of the commodity prices (including crude). In this context, H2FY23 is likely to be better than H1FY23, it added.

Foreign inflows

After withdrawing over ₹7,600 crore last month, foreign investors have slowed down the pace of equity selling in India in October so far, as they pulled out ₹1,586 crore from capital markets. So far this year, the total outflow by FPIs in equities has reached ₹1.70 lakh crore.

Analysts believe that the worst of the FIIs outflow is now behind us as the strong earnings growth and economic recovery will play out for the remaining months of 2022.

Global peers

Even as Indian markets have been resilient compared to global peers in the last few months, it underperformed US and European markets for the month of October in dollar terms. However, on a YTD basis, India still stands ahead of the US and European markets.

In October, the Dow Jones Industrial Average (Dow) gained 14.4 percent, the Euro Stoxx 50, DAX and CAC40 rose 9 percent each, and FTSE100 added 2.2 percent. By comparison, the Indian market gained less than 3 percent in US dollar terms.

However, on a YTD basis, the S&P BSE Sensex declined 7 percent. Whereas the Dow fell 9.6 percent, the Euro Stoxx 50 tanked 26 percent, FTSE100 lost 18 percent, CAC40 shed 23 percent and DAX crashed 27 percent in this time.

The gain in the US and Europe follows a sharp sell-off in September. According to analysts, the latest upmove in the developed markets is on optimism that the rate-hike cycle by the US Federal Reserve (Fed) will end sometime next year.

Outlook

As per Axis Securities, in the near term, the Indian market will continue to follow the Q2FY23 earnings, macroeconomic data, and the outcome of the central bank’s meeting, which is scheduled during the first week of November 2022.

While FII flows may remain volatile and the market witness higher volatility in the near term if pressure on the rupee continues, the Indian equity market is likely to outperform the global market over the medium to long term on account of its robust economic outlook, it explained.

Now the market is eyeing the FOMC meeting. Odds are in favour of a 75 bps rate hike on 2nd Nov’22 which is priced in. Hence, the market will set the direction based on the tone and the terminal rates. Any hawkish tone beyond the market expectations will create short-term volatility in the market. Additionally, the brokerage noted that the market will continue to be influenced by a) the direction of the dollar index; b) Bond yields; c) the direction of Inflation; d) Growth in the developed world, and e) the trend of commodity prices (including Oil).

Strategy

As per Axis, the cool-off in the key commodity prices coupled with the central bank's actions on front-loading the interest rates have changed the market style in the last two months. Growth as a theme has come back in the market in the last three-odd months, it noted.

"Given the government’s domestic interest-first approach and India as a domestic consumption economy, local or domestic-oriented themes are likely to perform better in the near term. We continue to believe that profitability will shift from commodity producers to commodity consumers going forward. Keeping this in view, Banks, Automobiles, Hospitals, Discretionary Consumption, and Domestic Industrial themes look attractive in the near term over Export and Commodity sector themes. Additionally, the value is emerging in the PSU stocks which is likely to sustain in H2FY23," it predicted.

While the medium to long-term outlook for the overall market remains positive, Axis noted that some volatility can be seen in the short run with the market responding in either direction. In this context, the current setup is a ‘Buy on Dips’ market. It recommends investors maintain good liquidity (10 percent) to use such dips in a phased manner to build a position in quality companies (where the earnings visibility is very high) and with an investment horizon of 12-18 months.

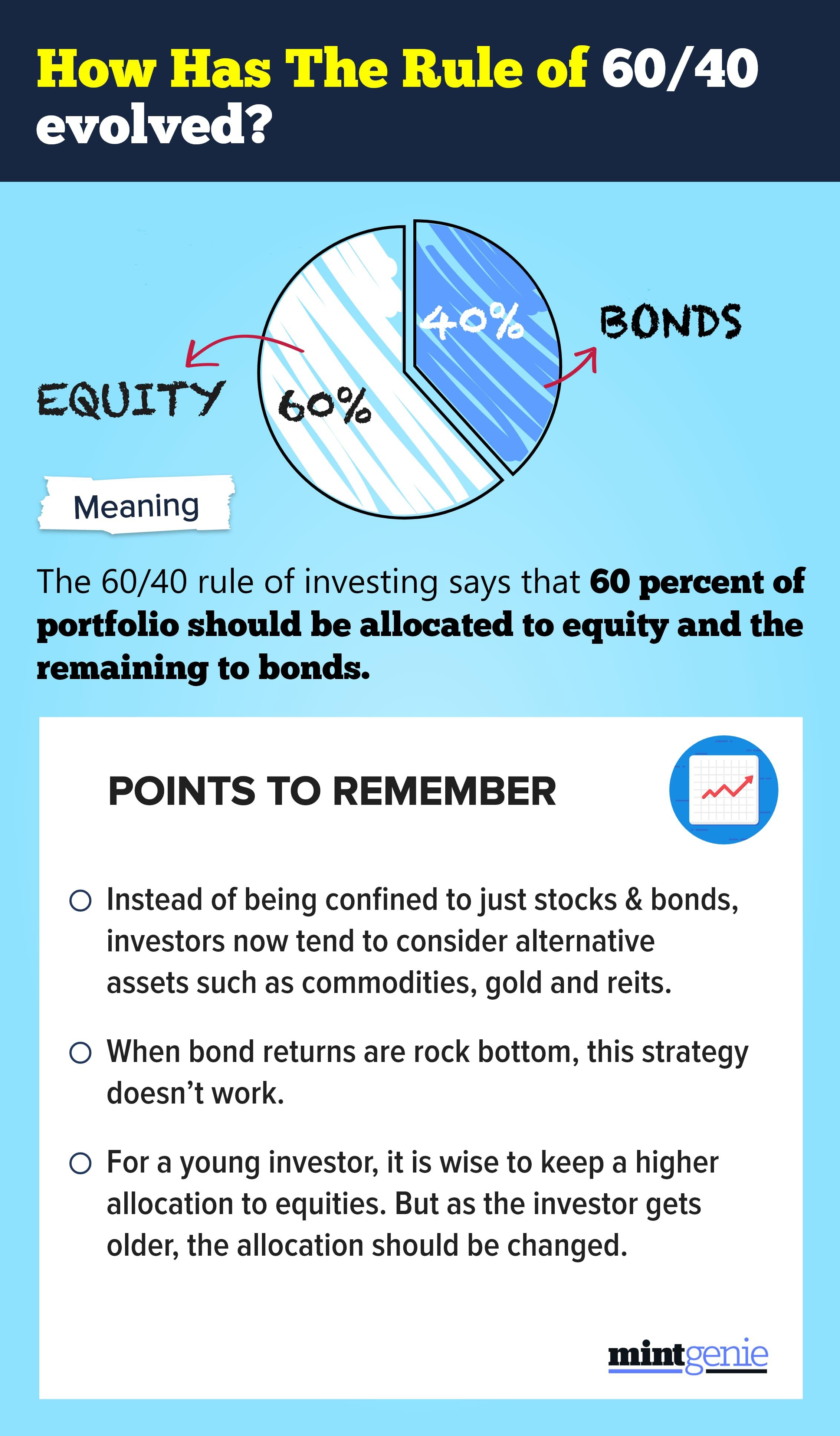

Usually the strategy of 60/40 doesn't work when the bond returns are rock bottom.

First Published: 03 Nov 2022, 11:28 AM IST