In the December quarter, smaller metal companies delivered relatively better performance than blue chips, noted domestic brokerage house ICICI Securities in an earnings review note.

The brokerage highlighted that among upstream steel players, only SAIL’s EBITDA was in line with consensus estimates, while others missed consensus estimates by 25-45 percent. Meanwhile, Jindal Stainless posted volume growth of 22 percent QoQ while other steel companies showed a decline, reported the brokerage. It further pointed out that APL Apollo’s EBITDA/te also declined the least among all steel players, adding that the performance of Tata Steel and Hindalco was also impacted by overseas subsidiaries- Tata Steel Europe (TSE) and Novelis; and finally, NALCO’s performance exceeded street estimates significantly while Hindalco’s was a miss mainly due to Novelis.

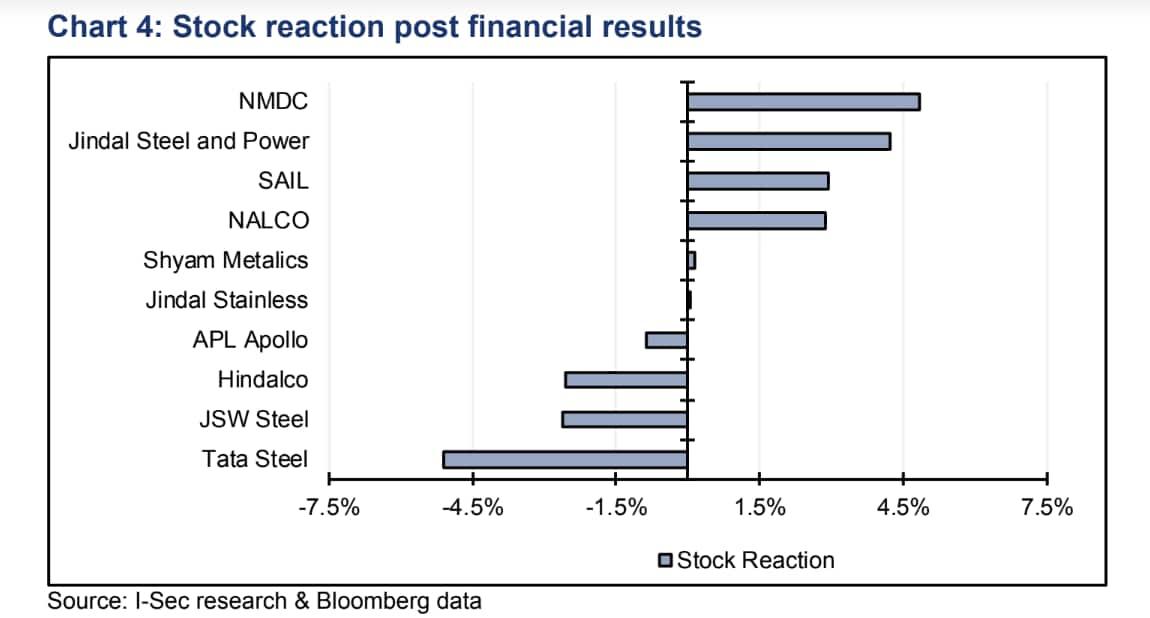

The brokerage also pointed out that the stock reaction post the result was most severe for big players such as Tata Steel, JSW Steel and Hindalco- down 3-5 percent while NMDC and JSPL were up 3-4 percent.

Going ahead, it expects EBITDA/te for steel companies to expand further QoQ due to higher export realisation though coking coal cost might play the spoilsport. The profitability of non-ferrous companies is also likely to get a leg up from higher LME prices and progressively lower coal costs, predicted ICICI.

Let's take a look at how different metal firms performed in Q3:

JSW Steel: EBITDA was in line with consensus estimates. Consolidated EBITDA surged 2.6x QoQ at ₹4,550 crore owing to lower cost at standalone operations. Performance of overseas subsidiaries, especially Italy, improved. Going ahead, the management expects the performance to improve further aided primarily by realisation, though the cost is expected, noted ICICI.

Tata Steel: EBITDA of ₹4,050 crore (down 75 percent YoY) was below street estimates though in line with ours. Lower coking coal prices offset the impact of lower steel realisations, which lifted domestic EBITDA/te. In our view, the worst is behind the stock as margins in both domestic and European operations are expected to improve from Q4FY23, said ICICI.

JSPL: Q3FY23 performance surpassed street estimates. EBITDA/te (adj.) was ₹11,381 (up 60.5 percent QoQ) on the positive price-cost spread. Shipments were impacted by rake/wheel shortages and lower export opportunities. Provision of ₹7,250 crore taken towards diminution in value of its investments in JSPML. Going ahead, ICICI expects JSPL to fare better than peers on longs prices faring better than flats.

SAIL: EBITDA was in line with consensus estimates. Sales volume growth was relatively muted. EBITDA/te (adjusted) rose ₹3,400/te QoQ on lower coking coal. Debt rose to ₹29,270 crore. Going ahead, management expects sales volume to improve; however, the recent uptick in coking coal prices might keep spreads under pressure, stated the brokerage.

Shyam Metalics: Q3FY23 performance met our estimates. The lower contribution from pellets and ferroalloys impacted profitability. Rolled product volume grew 49 percent YoY. Going ahead, we expect SMEL’s margins to improve as thermal coal cost has peaked off and the benefit of iron ore inventory at lower prices is likely to kick in, said ICICI.

Hindalco: Lower volumes and cost headwinds at Novelis led to 52 percent YoY plunge in Q3FY23 EBITDA, though it's India performance was in line with our estimates. Going ahead, it believes progressively lower costs are likely to aid India earnings, despite transient cost headwinds at Novelis, informed ICICI.

APL Apollo: EBITDA was ahead of the street and our estimates. Record sales volume of 605 kte (up 50 percent YoY) on higher shipments across segments. Blended EBITDA/te rose 17.1 percent QoQ to Rs4,510. Raipur plant (in Chhattisgarh) is now ramping up well- expected FY24 shipment at 600kt. Going ahead, management has targeted both volume growth and EBITDA/te improvement, highlighted the brokerage.

NALCO: EBITDA was significantly ahead of consensus due to lower-than-expected power and fuel costs. EBITDA margin at 14 percent rose 440bps QoQ. Profitability at Al division recovered sequentially owing to lower power and fuel costs. Going ahead, we expect Q4FY23 to be even better owing to higher LME Al price and progressively lower coal cost, said ICICI.

Valuations

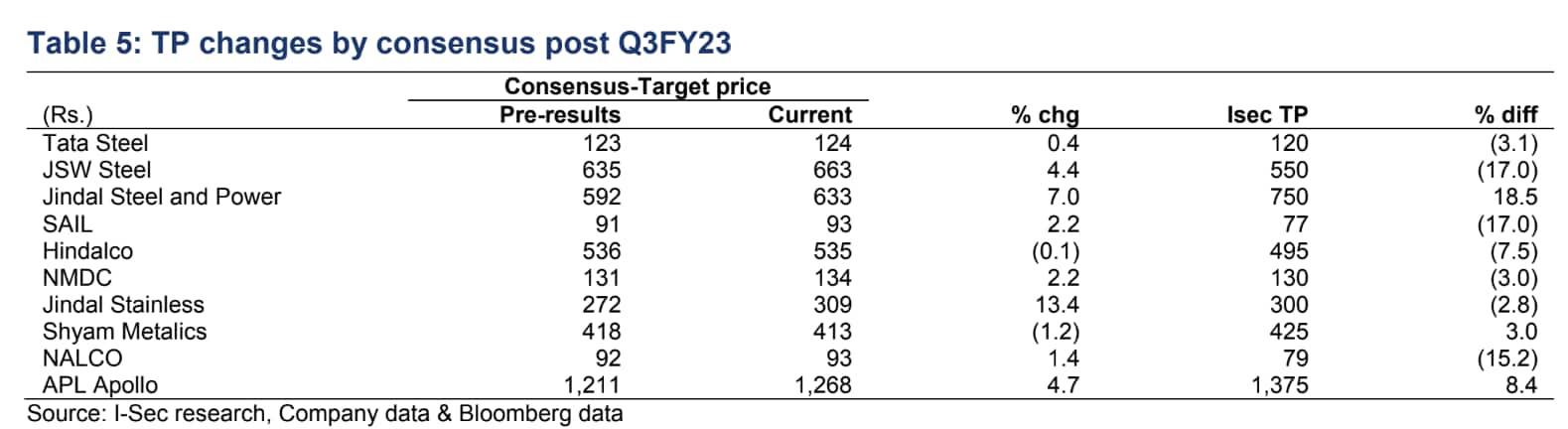

Post Q3FY23 earnings, the brokerage highlighted that Street has lowered FY23E/FY24E EBITDA estimates for almost all the companies under its coverage while raising target prices for most of them.

For instance, in the case of JSW Steel, FY23E/FY24E EBITDA has been lowered by 6.8/1.4 percent while the target price has been raised by 4.4 percent while in the case of JSPL, FY23E/FY24E EBITDA has been retained, while TP has been raised by 7.7 percent, noted the brokerage. Further, in the case of Jindal Stainless, the consensus target has been raised by 13.4 percent while the consensus FY24E EBITDA has been lowered by 6.8 percent, it added.

According to the brokerage, multiple expansion by the street indicates earnings have likely bottomed out.

"The ask-rate for Q4FY24 EBITDA is quite steep for Tata Steel (mainly due to losses narrowing at TSE) and JSW Steel (due to higher shipments), while it is quite low for JSPL. We believe there is scope for an upward revision in JSPL’s FY24E EBITDA for FY23 results due to volume growth and ensuing cost efficiencies," it said.

Outlook

Going ahead, the brokerage believes non-ferrous players

are likely to show relatively higher improvement in earnings mainly due to the twin benefits of higher LME price and lower coal cost. Among ferrous players, it said that Shyam Metalics is better placed as pellet contribution grows.

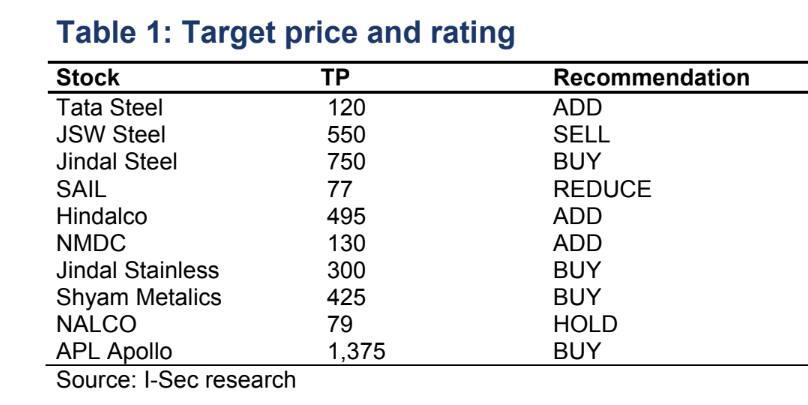

It maintains JSPL (TP: ₹750), Jindal Stainless (TP: Rs.300) and Shyam Metalics (TP: ₹425) as top picks in the space.