The banking sector has outperformed the benchmark index comfortably in the past month, 2022 YTD, as well as the last one year. In the last 1 month, the Nifty Bank index has risen over 5 percent versus a 4 percent rise in Nifty. Meanwhile, on a 2022 YTD basis, the banking index is up a whopping 16 percent as against a 4 percent rise in Nifty. In the last 1 year as well, the banks jumped 4 percent as compared to a 1 percent gain in Nifty.

Midcap private banks sharply outperform benchmarks and bigger peers; here's why

TL;DR.

According to experts, banks are taking advantage of the Reserve Bank of India (RBI) raising the repo rate. RBI has raised the key rate by 190 bps since May to 5.9 percent and high inflation levels mean that more hikes are on the way.

According to experts, banks are taking advantage of the Reserve Bank of India (RBI) raising the repo rate. RBI has raised the key rate by 190 bps since May to 5.9 percent and high inflation levels mean that more hikes are on the way.

While the entire sector is on an uptrend, midcap private banks has outperformed their bigger peers.

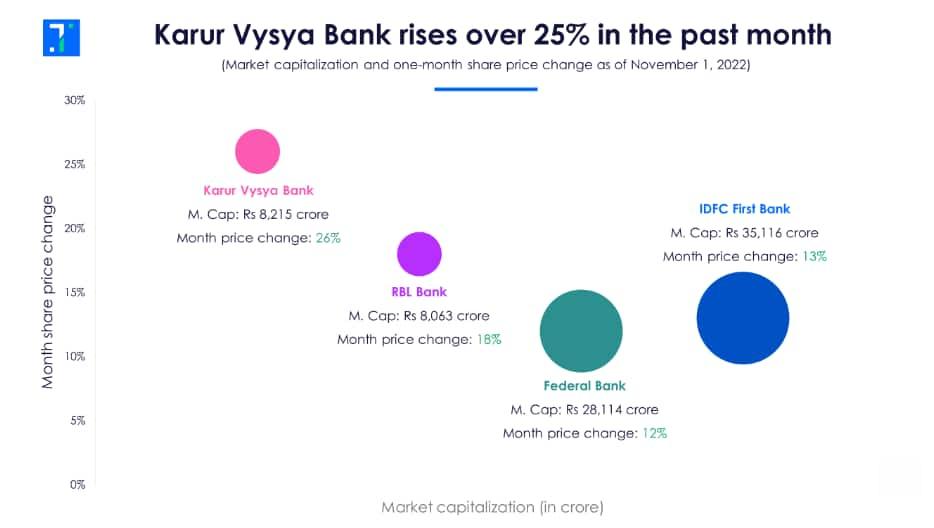

It noted that mid-cap banks’ share prices are sharply up on the back of improving net interest margins, strong loan growth, and asset quality. The banks in focus–IDFC First Bank, Federal Bank, Karur Vysya Bank, and RBL Bank–outperformed the Nifty 50 by at least 12 percent, with Karur Vysya Bank leading the pack.

Over the past quarter, the stock performance of these banks has been even more impressive. The rise in share price has come with strong results over the past three quarters. Q2FY23 results did not disappoint either. The revenue and net income of these banks rose sharply, explained the report.

Just in the last 1 month, Karur Vyasya Bank has rallied 26 percent whereas RBL Bank, Federal Bank, and IDFC First Bank have gained between 12-18 percent in this period. Meanwhile, its bigger peers like ICICI Bank, Kotak Bank, HDFC Bank rose between 2-4 percent in the past month. PSU lender SBI performed a little better, up 9 percent in the last 1 month.

Source: Trendlyne

Several tailwinds like rising repo rates and strong loan book growth from high retail consumption have helped banks post strong Q2 results, it noted, adding that housing and vehicle loans were the star segments for banks in Q2.

But is this demand in housing and vehicle loans sustainable? Trendlyne believes that housing and vehicle loans may become less attractive with rising interest rates and analysts predicting more hikes in the coming months. In addition, according to CMIE data, new investment proposals by the private sector have been falling since Q1FY23 and this could slow loan growth, it said.

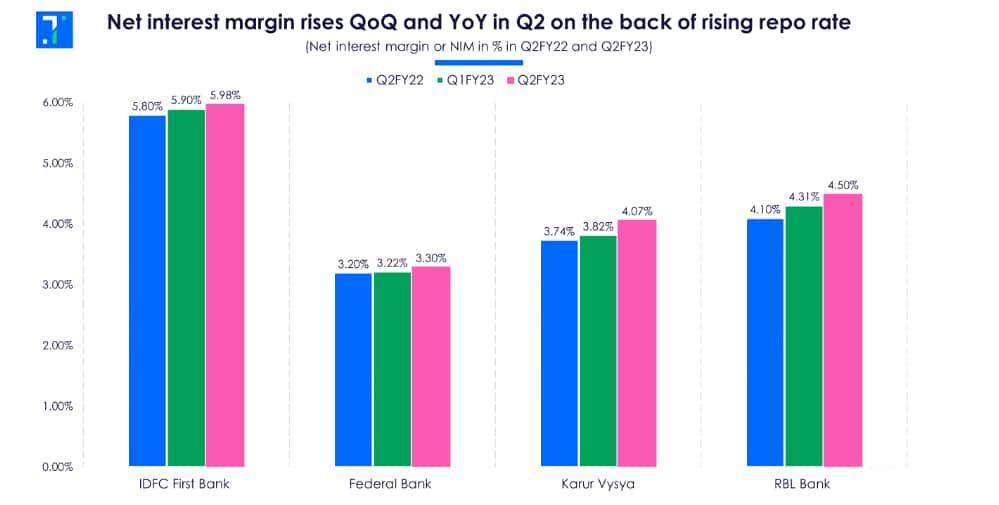

However, a key positive for these lenders is that their net interest margin (NIM) has been on the rise for all four over the past five quarters and accelerated in the last two quarters, thanks to the rising repo rate, pointed out Trendlyne.

NIM of the banks in focus rose both YoY and QoQ in Q2FY23. IDFC Bank enjoys the highest NIM among the four at 5.98 percent. Its management is confident about maintaining NIM at 6 percent in FY23, said the report.

Source: Trendlyne

Another positive factor for these banks is their improving CASA ratio. "The CASA ratio is the ratio of deposits in current and saving accounts to total deposits. The higher the CASA ratio, the better. A higher percentage indicates a lower cost of funds because banks do not usually give any interest on current account deposits, and the interest on saving accounts tends to be very low," noted the report.

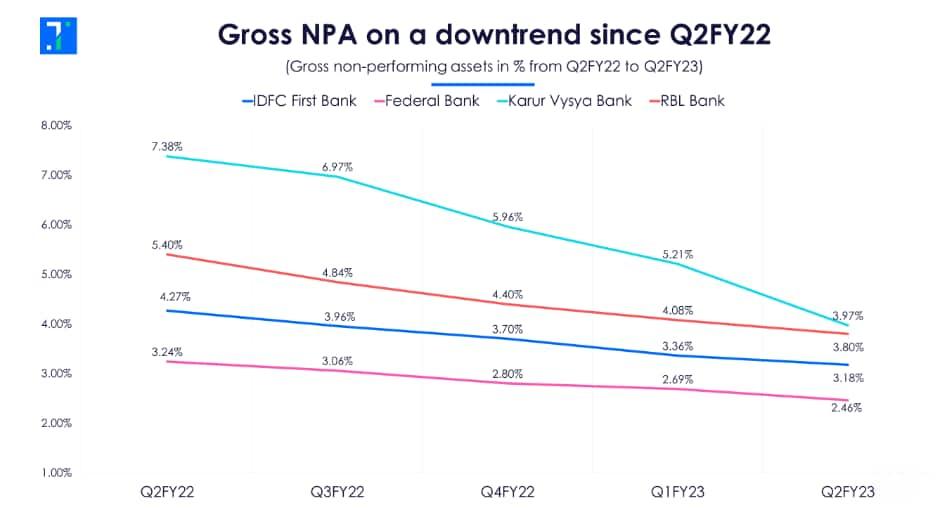

Banks also provide several health-check metrics to assess asset quality, risk levels, etc. One key ratio is the gross non-performing assets (GNPA), which helps us understand the level of non-performing assets relative to total advances. This ratio has been on the decline for the past five quarters for the banks in focus, indicating a significant improvement in asset quality.

The gross NPAs of all these banks have also been on a downward trend since Q2FY22.

Source: Trendlyne

Valuations

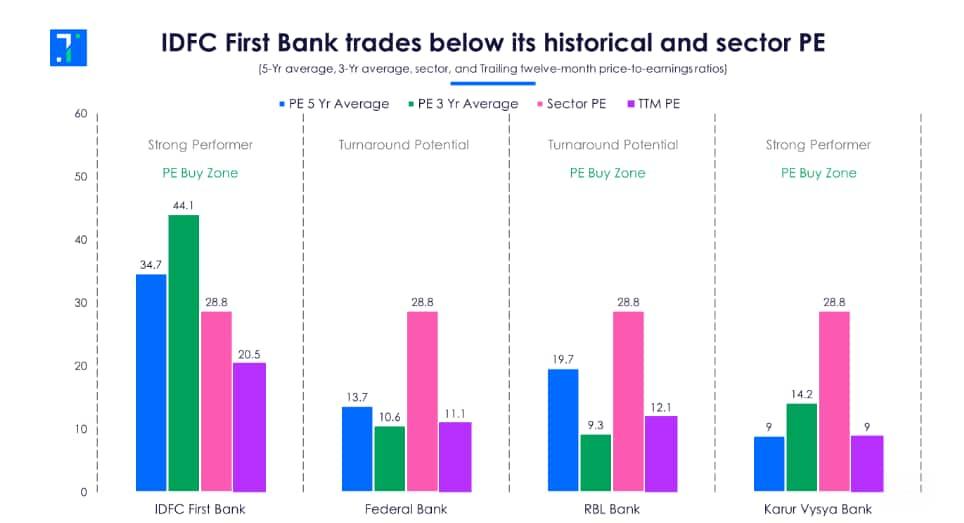

Despite a sharp run-up in share prices, three out of the four banks in focus are in the PE buy zone.

According to Trendlyne, IDFC First Bank and Karur Vysya Bank are strong performers and

Source: Trendlyne

are also in the PE buy zone – meaning that their PE ratios now are lower than historical levels.

So all these tailwinds make midcap private banks great buying opportunities? Let's first understand the relationship between banks and RBI rate hikes.

Trendylne explains: Banks want the best of both worlds - they are quick to hike interest rates on loans (which adds to their income) but are slow to hike deposit rates (which they pay to account holders). So rate hikes by the RBI help banks improve their net interest margin since they benefit from the difference between the bank’s interest income and the interest they pay to their lenders.

However, it is important to note that banks cannot benefit from this for too long, as they need to hike rates on deposits eventually. Higher interest rates also bring down loan growth, especially in retail sector lending, which is mainly consumption-driven, noted Trendlyne said in a report. Companies also postpone their spending plans when interest rates are high, as businesses have to shell out more money to service loans, it added.

So despite a sunny outlook by both analysts and banks, Trendlyne stated that it is cautious on the banking space. There are several factors that are potential roadblocks to rising net interest margins and strong loan growth, it noted.

While the outlook is strong for these banks, investors should keep in mind key risks going forward, advised the report. "Rising interest rates may slow down loan growth. Loan growth is also dependent on consumption-driven retail loans (especially in the housing sector), and rising mortgage rates could hurt demand in this sector," it said.

Corporate loan books could also get affected as private companies cut back on spending due to fears of an economic slowdown and rising interest rates, it further added.

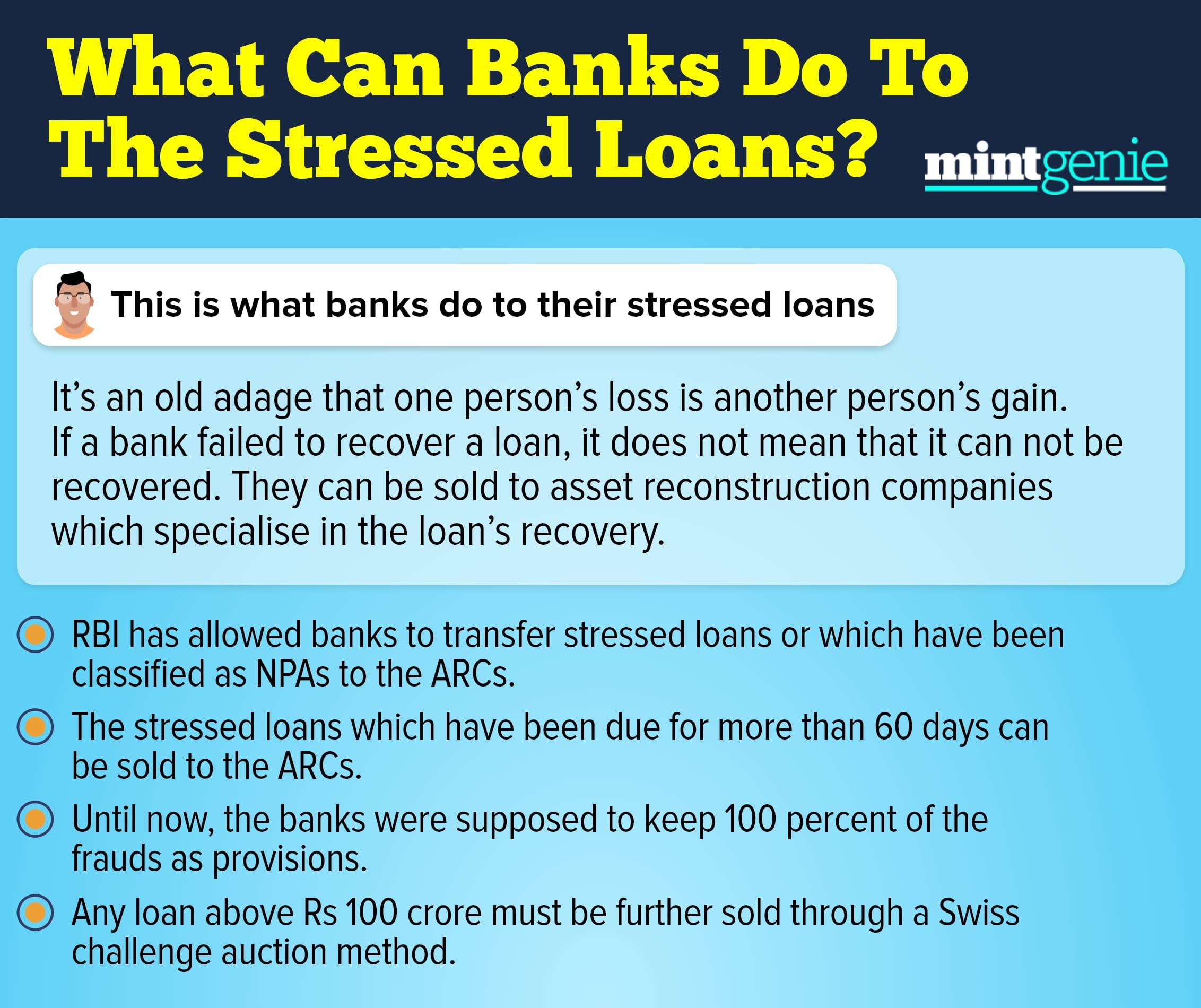

This is what banks can do to the stressed loans.

First Published: 04 Nov 2022, 12:17 PM IST

Related Stories

personal finance

Your Questions Answered: Financial planning, asset allocation and differences between savings and investments

International Money Matters