Brokerage firm HDFC Securities has initiated coverage on Mishra Dhatu Nigam (MIDHANI) stock with a 'buy' recommendation.

The brokerage firm has fixed a base case fair value (target price) of ₹242 and a bull case fair value of ₹260.5 for a two-quarter time horizon.

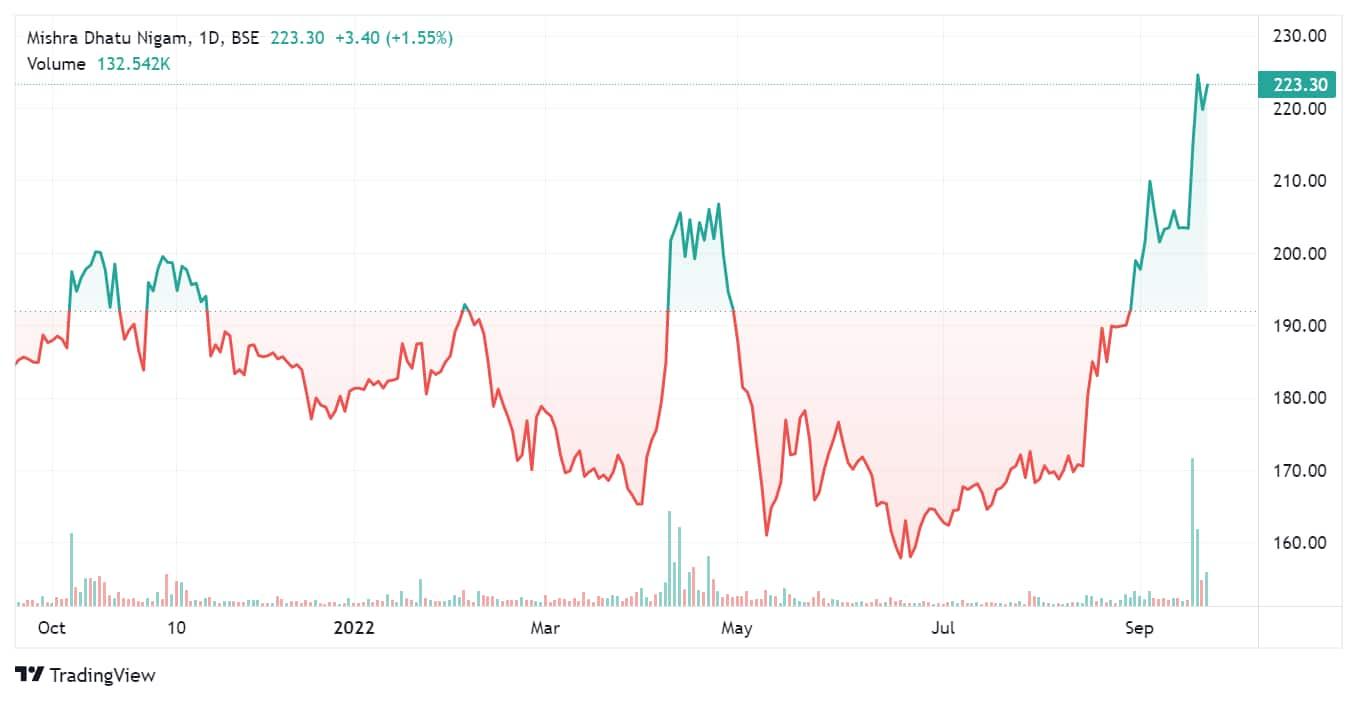

In the last one year, the stock has gained 21% on BSE while the benchmark Sensex is almost flat for the period.

HDFC Securities pointed out that MIDHANI is majorly owned by the government and manufactures a variety of superalloys, titanium and titanium alloys, special-purpose steels, controlled-expansion alloys, soft magnetic alloys, electrical-resistance alloys, molybdenum products, and other special products that are made according to customer specifications.

MIDHANI has established a market position in manufacturing superalloys with better operating efficiency; the company has a strong track record in signing and executing deals, the brokerage firm added.

Sizeable revenue growth and steady operating margin of 27-29%, ensure healthy cash accrual and liquidity and better working capital management despite high inventory. Its strong financial profile with healthy liquidity, negligible debt and attractive return ratio, on the back of good revenue visibility brings a positive view on the stock, HDFC Securities said.

However, the brokerage highlighted that susceptibility of profitability to volatility in raw material prices and foreign exchange (forex) rates, and large working capital requirements are some concern areas that need to be tracked.

"Considering the company’s strong financial profile, led by healthy profitability levels and return indicators and a comfortable capital structure, we have a positive view on the stock. Investors could buy in the ₹218- 222 band and add more on dips to ₹194 (16 times FY24E EPS)," HDFC Securities said.

"Base case fair value of the stock is ₹242 (20 times FY24E EPS) and the bull case fair value of the stock is ₹260.5 (21.5 times FY24E EPS) over the next two quarters. At the current market price of ₹219.7, the stock trades at 18.2 times FY24E EPS," the brokerage added

Disclaimer: The views and recommendations given in this article are those of the broking firm. These do not represent the views of MintGenie.