Global brokerage house Morgan Stanley has initiated coverage on four affordable housing finance companies. As per the brokerage, the space is niche, under-penetrated, has a secular growth outlook with pricing power, and is ESG (environment, social, and governance) positive.

The thesis is stronger now as asset quality has been tested by COVID, valuations have de-rated and peak rates are in sight, highlighted the brokerage.

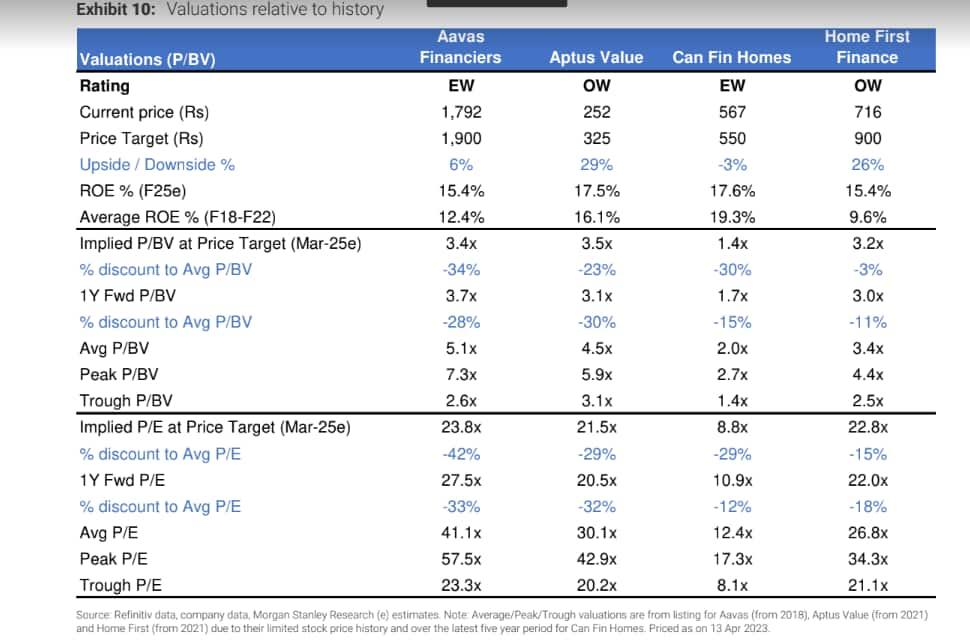

The brokerage is ‘equal-weight’ on Aavas Financiers and Can Fin Homes; and ‘overweight’ on Aptus Value and Home First Finance.

It sees 29 percent and 26 percent potential upsides in Aptus Value (TP: ₹325) and Home First Finance (TP: ₹900). Meanwhile, it sees a 6 percent upside in Aavas Financiers (TP: ₹1,900) and a 3 percent downside in Can Fin Homes (TP: ₹550).

What drives MS' stock preferences?

Valuations have become reasonable to attractive following trailing stock underperformance; as rates peak out, investor interest in these stocks should pick up along with other NBFCs, noted MS.

All these 4 stocks have given negative returns in 2022 with Aavas down the most, 29 percent, Aptus down 11 percent, and Can Fin Homes and Home First down 2 and 5 percent, respectively.

Meanwhile, in 2023 YTD, except Can Fin Homes, up 7 percent, the other 3 stocks have been in the red. Aptus shed the most, 20 percent followed by Aavas, down 8 percent and Home First, down 3 percent in this period.

The brokerage prefers Aptus and Home First given smaller balance sheets and hence higher loan growth potential, as well as better business risk-return profiles and valuations in the context of the same. It believes these stocks together offer a complementary combination of higher return potential and better risk profiles.

Meanwhile, it's equal weight on Aavas due to higher relative valuations and Can Fin on the back of a much larger size, vulnerability to bank competition, and uncertainty around promoter stake.

The brokerage notes that Aavas's track record and significant familiarity in the investor community are positives, while for Can Fin, its higher return on equity (ROE) profile stands out, it explained.

Why should you look at affordable housing finance companies (AHFCs) structurally?

As per the brokerage, there is a secular growth opportunity in a systemically important sector. Housing finance is under-penetrated in India and there is a significant skew by geography and income segments, i.e. the opportunity is significantly higher outside the top four states and in disbursements of ticket sizes less than ₹25 lakh.

"AHFCs are a secular play on this opportunity and stocks of AHFCs could offer strong long-term compounded returns. The economic multiplier of this sector and its role in financial inclusion (positive ESG) has meant that the government and regulators have been supportive and are likely to remain so," it said.

It further pointed out that unlike in the case of home loans to salaried prime category customers (large ticket and easy to underwrite), where profitability for HFCs is significantly challenged and volatile owing to intense competition from banks, this segment (small ticket, high touch, difficult to underwrite) requires a specialized approach and hence sees low interest from banks.

"Unlike large HFCs, AHFCs have pricing power. Large HFCs are typically vulnerable to rate cycles as they largely operate in the prime housing loan segments and are thus subject to intense competition from banks which have an inherent cost of funds advantage. However, AHFCs operate in a niche, difficult to assess customer segment and have significantly higher margins, enabling them to better navigate rate cycles and protect margins," it explained.

Why is now a good time?

Historically, key concerns regarding affordable housing finance firms for investors have been steep valuations and confidence around the quality of underwriting. But the brokerage believes COVID-19 has provided strong validation of the underwriting model. Valuations have significantly de-rated to reasonable/ attractive levels, it said. With interest rates close to peaking, it sees the narrative shifting in favour of the NBFC sector. Thus, these stocks could screen attractively for investors looking for structural stocks with a cyclical tailwind and attractive valuations, added MS.

Estimates

MS expects healthy loan growth, EPS growth and ROEs for the AHFCs over the next two years.

Aavas has a high mix of non-housing loans, self-employed customer loans, and new-to-credit customers, and 44 percent of loans are at fixed rates. MS forecasts an F23-25 AUM CAGR of 21 percent, an EPS CAGR of 22 percent, and an F25 ROE of 15.4 percent. Aavas has a proven track record and a sound business model, however, its higher loan base (double that of peers) means it is likely to grow more slowly than smaller peers. It is also undergoing an IT transformation project which could have an adverse effect on operating costs in the near term, MS noted.

For Aptus Value, the brokerage estimates an F23-25 AUM CAGR of 30 percent, EPS CAGR of 22 percent and F25 ROE of 17.5 percent. It believes there are upside risks to earnings and ROE estimates if Aptus Value is able to sustain current loan spreads.

Given Can Fin Homes' higher AUM base ( ₹30,000 crore) and more conventional business mix, MS predicts an F23-25 AUM CAGR of 20 percent, an EPS CAGR of 16 percent, and an F25 ROE of 17.6 percent. Higher ROEs are unlikely to sustain as they are largely driven by high leverage which will eventually have to be moderated, it said.

Given Home First Finance's low AUM base and diversification into non-housing loans against property (LAP, targeting 15 percent of AUM), MS forecast an F23-25 AUM CAGR of 30 percent, an EPS CAGR of 24 percent, and F25 ROE of 15.4 percent.