A stellar run-up by PSU banks had all eyes glued toward them. Nifty PSU Bank is the best-performing index among all NSE indices in 2022. The index has surged over 60 percent during the year as against a 19 percent rise in Nifty Bank and an around 4 percent gain in benchmark Nifty. Despite the recent surge, domestic brokerage house ICICI Direct believes that the risk-reward still favour PSU Bank valuations and that the valuations remain reasonable for them.

The Nifty Bank index has gained 22 percent in the last 6 months while the Nifty PSU Bank has rallied 74 percent in this period.

"Post the phase of significantly higher gross non-performing assets (GNPA), treasury mark-to-market (MTM) losses, lower capital and sub-par growth, there has been a turnaround with comfort on asset quality; reversal of treasury losses, credit growth pick-up and just adequate capital position for most of them. Despite the decent rally, valuation still looks reasonable for PSU banks," explained the brokerage.

The PSU Bank index also hit new highs earlier this month but later consolidated. It is up 2 percent in December so far and 15 percent each in November and October on the back of strong earnings for the July-September quarter (Q2FY23). The public sector banks have posted strong earnings in Q2 due to the acceleration in credit growth, improvement in asset quality, rise in loan growth, and decrease in provisions.

All stocks in the Nifty PSU Bank index are also positive for the year. Of the 13 stocks in this index, 3 have given multibagger returns in 2022 - UCO Bank, Bank of Baroda and Indian Bank; while 3 have advanced over 70 percent each - Punjab & Sind Bank, Union Bank and Bank of India.

The brokerage analyses key factors leading to this rally. Let's take a look:

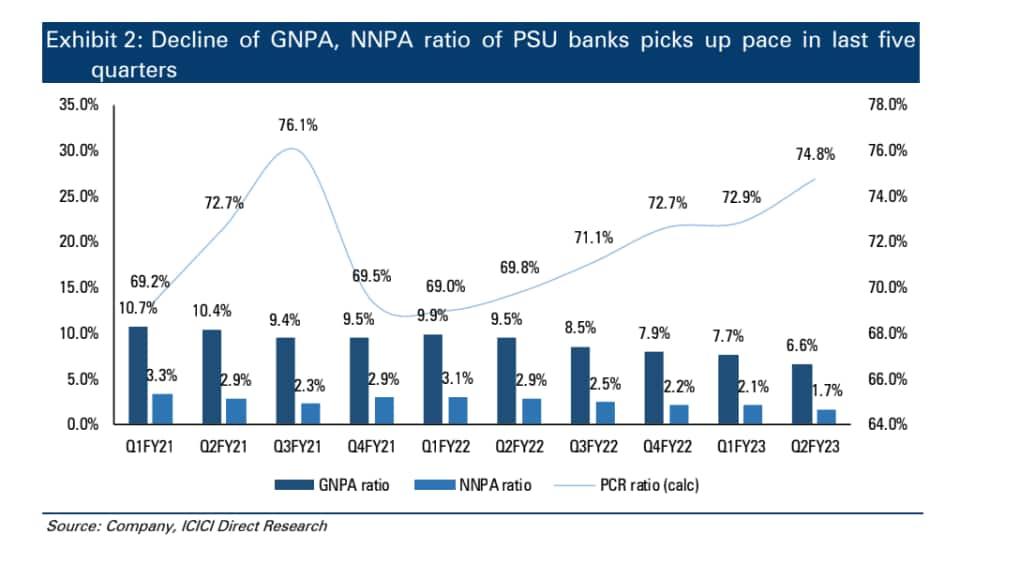

GNPA, NNPA ratio decline picks up pace in last five quarters: According to the brokerage, the asset quality trend continued to improve led by healthy recoveries and steady incremental slippages. Absolute GNPA and NNPA declined 16 percent and 30 percent YoY, respectively, in the second quarter of FY23 (Q2FY23) after a similar cut in the third quarter if FY21 (Q3FY21). GNPA and NNPA ratios for PSU banks have declined from 9.4 percent and 2.4 percent in Q3FY21 to 6.6 percent and 1.8 percent in Q2FY23, respectively, it added.

Management comments, a revival in the economy suggests an improvement in asset quality and lower credit cost ahead with Provisioning Coverage Ratio (PCR) currently around 75 percent, informed the report.

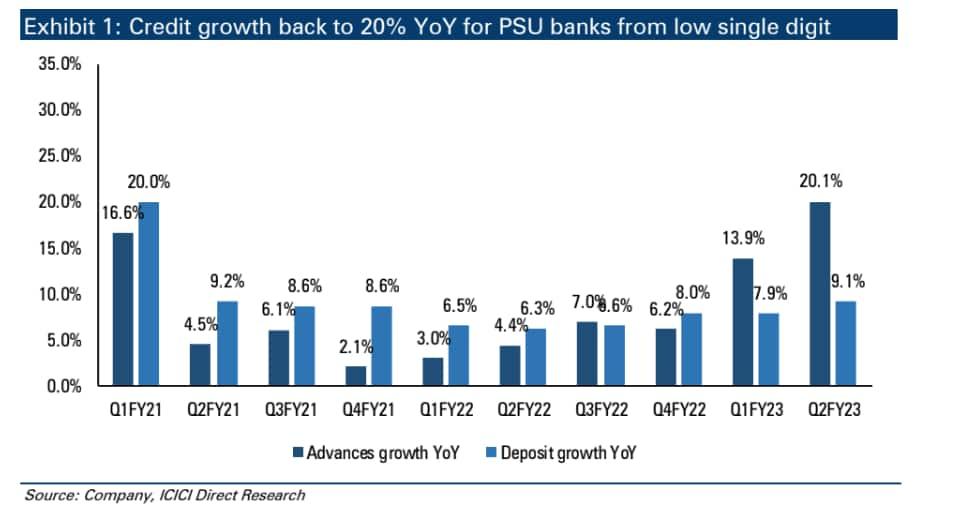

Credit growth back to 20 percent for PSU banks from low single digits: This is another key positive for public sector lenders. Loans recorded growth of 20.4 percent YoY, 4.8 percent QoQ to ₹120.4 lakh crore, noted ICICI. However, PSU banks saw growth surging to 20.1 percent in Q2FY23 (including international) from 3 percent in Q1FY22.

"Business momentum is healthy, attributable to robust demand in the retail & MSME segment. Corporate credit grew for most banks including PSU banks. Banking sectoral data (October 2022) shows the retail segment was up 20.2 percent YoY and Agri credit jumped 13.6 percent YoY. Large corporate credit, which had been a drag on overall banking credit growth, has started to enter the positive territory in the past few quarters. Management commentaries and data indicate a revival in utilisation of working capital (WC) limits. Thus, we believe bank credit growth should continue to remain at 15-16 percent with PSU banks at 12-15 percent," stated the report.

G-sec yields moderating, expect stabilisation: As per the brokerage, treasury losses amid a run-up in yields impacted the improvement in operational performance in Q1FY23. However, the recent decline in yields from 7.5 percent to 7.3 percent is expected to reverse these losses, which no longer seems an overhang for PSU banks, it added.

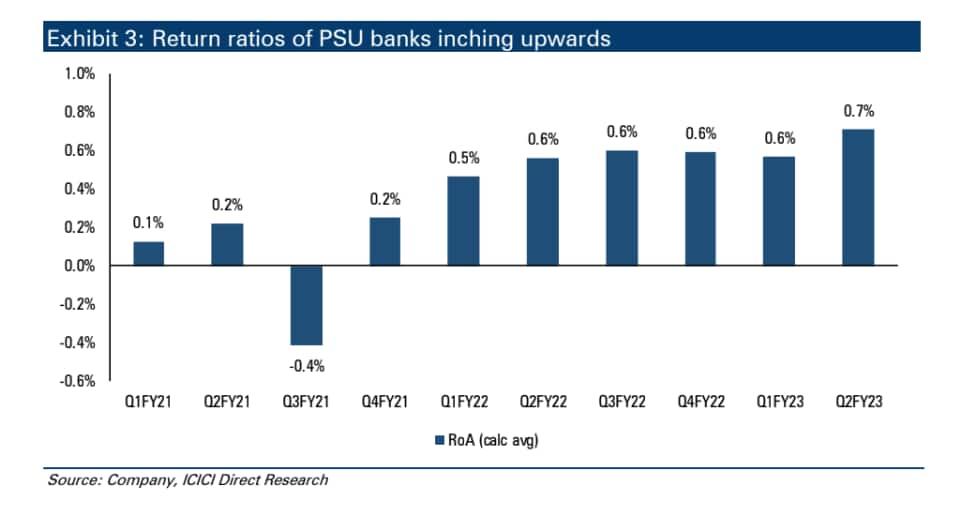

Margins, PAT, and return ratios going northwards: This is another important reason behind the rally in PSU Banks. The public sector lenders have reported a 20 percent YoY and 13.6 percent QoQ growth in their net interest income (NII), the highest in the last eight quarters.

Faster transmission of rate hikes on assets compared to liabilities and a healthy proportion of low-cost deposits led to a strong sequential rise in margins (10-40 bps QoQ), noted ICICI. Further, management commentary suggests margins will remain steady at the current level in H2FY23, it said. Led by a strong topline and lower credit cost, the net profit of PSBs grew 19 percent YoY and 70 percent QoQ to ₹26,021 crore for Q2FY23 depicting improving earnings, informed ICICI.

Hence, with the expected sustainability of earnings growth, return ratios are improving. Return on assets (RoA) has reached 0.6-0.8 percent in Q2FY23 similar to FY14-15 levels and ICICI expects further improvement in RoA though the return on equity (RoE) may take longer to surge, except for SBI, BoB, Indian Bank and Canara Bank where RoE has reached over 11 percent, it explained.

Valuations still reasonable

Going ahead, the RoA for large PSU banks is seen inching towards 0.8-1 percent gradually, predicted the brokerage.

"With a recovery in growth and stable asset quality, PSU banks are set for a further re-rating. Large PSU banks (SBI, BoB, Canara Bank) are trading at ~0.8-1x P/BV, which paves the way for a further re-rating as peak valuations remain at 1.2-1.5x in FY12-14. Mid-sized and small banks, currently trading at 0.5-0.7x P/BV, touched 1x then," it said.

ICICI remains positive on PSU banks, with upsides expected to continue in the medium-term horizon.