Even as the year 2022 is ending on a positive note with the benchmarks ending 4.5 percent higher, it was riddled with turbulence and headwinds including the Russia-Ukraine war, rising inflation, rate hikes, concerns regarding global growth, etc. Going ahead, will 2023 be any different?

Global brokerage Nomura continues to see muted growth in the benchmarks in the upcoming year. The macros-growth-inflation dynamics remain uncertain and will likely continue to influence the market movement in 2023, it said.

The brokerage expects a flattish market return through 2023 on the back of earnings risks and elevated market valuations.

It has set a Nifty target of 19,030 for 2023, indicating an upside of just 3 percent.

"The global macros (inflation and growth dynamics) remain uncertain as economies adjust to a new equilibrium post the COVID-19 pandemic. Inflation has peaked but could remain sticky. This would likely keep Fed hawkish prioritizing inflation flight over growth slowdown. The tightening monetary policy could drive major economies into recession and India’s growth will likely be adversely impacted from the global spillover," it explained.

However, it expects Indian markets to be unstirred on any negative rate/inflation surprise but it is likely to be sensitive to the overall growth outlook.

It further pointed out that the current corporate earnings consensus estimates for FY24/25 factor in the improvement of profit margin across most sectors to multi-year highs. Thus, it expects the medium-term growth in earnings from a high-margin base to be largely dependent on broader economic growth.

"Strong corporate and bank balance sheet, policy support and not-so-tight monetary policy are growth enablers that our economics team expects to drive recovery in 2024F. However, during the slowdown phase the markets may be less sanguine of such a recovery and thus can overreact, particularly as current expectations are elevated," it stated.

Limited upside

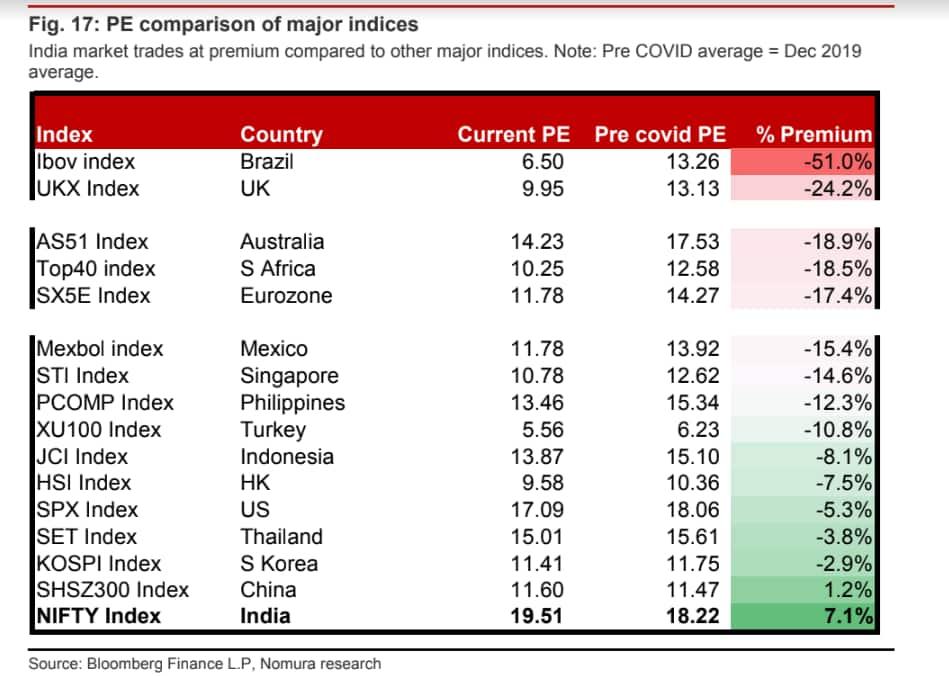

According to the brokerage, unlike most markets, Nifty 50 is trading at higher valuation multiples than pre-COVID levels. The valuation premium to EM is at 70 percent vs the historical average of 40 percent.

The brokerage believes that the market valuations reflect expectations of a strong earnings momentum and relatively stable macro. Assuming a 5 percent risk to Dec-24F consensus earnings estimates and 18.5x one-year forward PE, it has arrived at a Nifty target of 19,030.

Portfolio

Nomura said that it is cautious at current market levels. The market valuations are stretched with strong earnings growth expectations by the Street over FY23-25F. It expects the impact of higher rates on India’s market valuations to be modest. However, valuations will likely be more sensitive to changes in growth expectations, it added. Its economics team is factoring in below-consensus GDP growth for India (2023F: 4.5 percent; consensus estimate: 5.8 percent), largely driven by the significant global slowdown (recessions in the US and Europe).

"During this slowdown phase, we think that market concerns on earnings growth may emerge. The corporate earnings growth in FY22-25 will likely be supported by margin expansion, with profit margins across most sectors projected at multi-year highs. Thus, with margin expansion already accounted for in Street estimates, broader economic growth will be key to sustain earnings growth (and thus valuation multiples) in the medium term," it said.

A strong corporate and bank balance sheet, policy support and not-so-tight monetary policy are growth enablers that are expected to drive recovery in 2024F, noted Nomura. The growth concern in early 2023 can potentially drive a correction. This could present a better entry point from medium-term perspective, it said.

Prefers domestic plays

Nomura prefers domestic sectors over exporters. Within domestics, it likes sectors/companies with low earnings sensitivity to economic slowdown.

The brokerage is Overweight (OW) on banks, consumer staples, infra/construction and telecom; and Underweight (UW) on consumer discretionary, capital goods, metals, and IT services.

It is Neutral on healthcare (prefer domestic exposure), oil & gas and utilities.

Top picks

Large-cap: SBI, Axis Bank, L&T, HUL, and RIL

Mid/small cap: KEC Int, Zydus Life, IGL, and Sansera Engg

Strong earnings recovery

Nomura also highlighted that the corporate earnings momentum improved significantly through the COVID-19 period. Over FY19-22, corporate earnings rebounded strongly, leading to an improvement in ROE (return on equity).

The NSE 100 universe recorded an earnings CAGR of 22.1 percent over FY19-22, vs mid to high single-digit growth recorded in FY15-20, it said.

For the NSE 100 universe, the Street expects earnings growth of 11 percent, 20 percent and 13 percent for FY23F, FY24F and FY25F, respectively, with growth relatively muted in FY23 due to lower earnings from the commodity sectors (metals, and oil and gas), it predicted. Excluding these sectors the earnings growth would be strong at 29 percent YoY in FY23, noted Nomura.

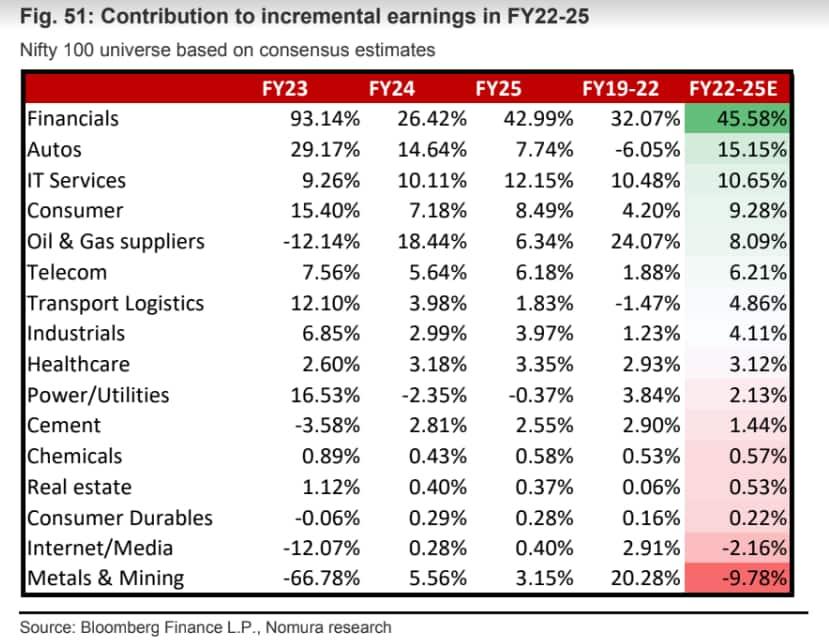

Based on current consensus estimates, over FY22-25F, financials will contribute the most (46 percent) to incremental earnings growth, similar to FY19-22. However, unlike the FY19-22 period, it is the commodity consuming sector (autos and consumer) that are the next largest contributor to the earnings rise, predicted the brokerage.

Key risks

As per the brokerage, stronger-than-estimated global growth and a weaker domestic growth outlook present risks to its portfolio. It said this can impact our calls, particularly on financials and IT services.