Even as the stock of fintech firm Paytm is down 50 percent on a year-to-date basis, global brokerage Goldman Sachs views Paytm as one of the most compelling growth stories at an attractive price.

The brokerage said that it believes Paytm's current share prices offer a compelling entry point into India’s largest and amongst the fastest-growing fintech platforms.

"While the Paytm stock is down 50 percent YTD on regulatory headwinds and valuation contraction for high growth companies, we see the business model as continuing to show strong traction, and within our internet coverage, view Paytm as one of the most compelling growth stories at an attractive price," said the brokerage.

Even as other experts remain skeptical about the stock, GS sees the stock rising 66 percent to ₹1,100 in 12 months. With a valuation at 3.6x FY24 EV/Sales, a 30 percent discount to India's internet peer group, the brokerage has reiterated its Buy rating on Paytm and has also added Paytm to its conviction list.

In the bull case scenario, the brokerage expects a massive 119 percent upside at ₹1,450, however, in a bear case scenario it sees the stock falling another 9 percent at ₹600.

It is important to note that the 12-month target price is still below Paytm's issue price of ₹2,150. The current stock price of Paytm is still down nearly 70 percent from its IPO price.

The brokerage expects Paytm to deliver 50 percent revenue growth for the next few quarters and continue its transition from an erstwhile payments-only business to one with a strong financial services portfolio. As a consequence, it sees the margins of the firm improving further.

Goldman’s analysis suggests the current share price is implying scenarios such as zero revenues from Paytm’s BNPL product and halving of take rates for other lending products, or adjusted EBITDA profitability not until FY27, or 0 percent revenue growth starting FY33, among other outcomes, which is seen as “unlikely and overdone”.

Even within India internet, Paytm’s growth outlook is similar vs peer group, but valuation is at the lower end,” it added.

Adverse impact on operations from any regulatory changes, rise in competitive intensity, potential disruption in partnerships, sub-optimal capital allocation are key risks to its upside, cautioned Goldman Sachs.

But what is driving the addition of the stock to GS' Conviction List?

Reducing regulatory overhangs: RBI’s recent guidelines on digital lending remove one key overhang for Paytm, and GS expects minimal impact on Paytm’s EBITDA from any potential change in payment charges.

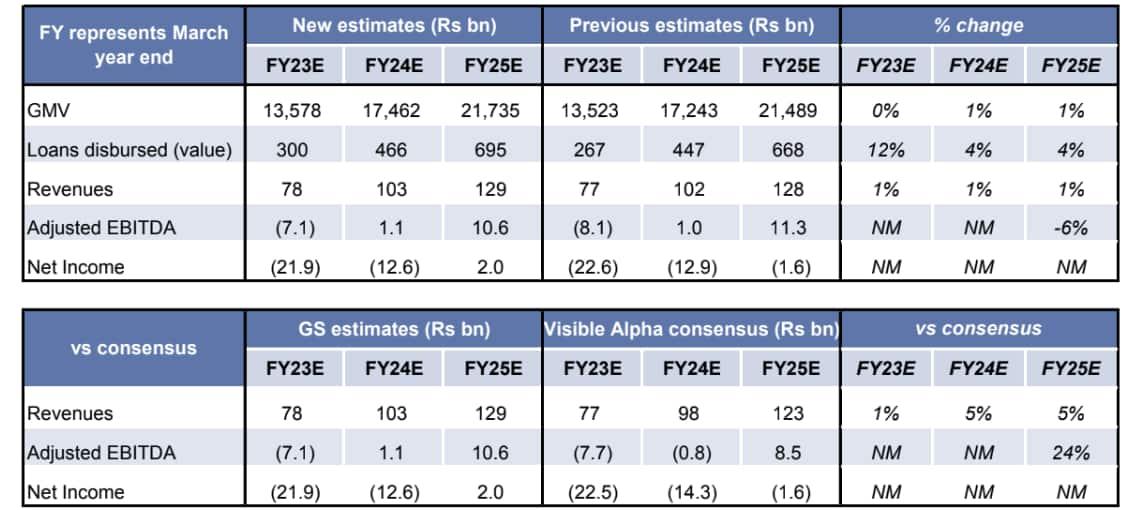

Strong lending growth: Through the course of CY22, the brokerage said that it has consistently raised its estimates for Paytm’s loan disbursals (FY23E disbursals 66 percent higher vs what we had estimated in Dec ‘21), and with this note, it further raises estimates by 4-12 percent given continued strong expansion in Paytm’s lending book.

Higher visibility on the path to profitability: Paytm’s consistently high topline growth (90 percent YoY revenue growth last 3 quarters) and good opex control give us more confidence in the company’s ability to be profitable in FY24 and we see this as one of the key catalysts for the stock, said the brokerage.

Improving payment take rates and spreads: Monetization of Paytm’s payments vertical has been improving, with take rates for non-UPI payments at 0.72 percent in June ‘22 vs 0.68 percent in FY21, noted GS. This has resulted in the margin profile for Paytm’s payments vertical resetting higher, aiding overall profitability, it added.

As mentioned earlier, the broekrage sees the stock more than doubling investor wealth in its bull case scenario.

Key assumptions by GS under its bull case: 1) Faster penetration of digital payments in India, 2) Higher market share for Paytm in payments, 3) Faster scale-up of financial services vertical, 4) No pressure on device rentals vs 10 percent cut in FY24 in the base case.

Meanwhile, in the bear case, the broekrage sees the stock cracking more to ₹600.

Key assumptions under bear case: (1) Higher mix of UPI in digital payments than our expectations; (2) Lower market share due to increase in competition in both payments and commerce; (3) Slower than expected scale-up of financial services vertical; (4) Caps on payment take rates; (5) 30 percent cut in device rentals in FY24.

"Investors we have spoken to in recent months remain skeptical about Paytm’s ability to be profitable, and we believe that as Paytm reports narrowing of EBITDA losses over the next few quarters and breakeven in FY24, the stock should re-rate higher," opined GS.

It notes that Paytm’s adjusted EBITDA margin has improved by 35 percentage points in the last five quarters to -16 percent in 1QFY23 and forecasts imply improvement over the next five quarters at half the pace of the recent quarters.

It estimates Paytm will reach adjusted EBITDA breakeven at about ₹2400 crore of quarterly revenues by September 2023, or 43 percent higher vs revenues reported in June 2022.

"We think such revenue growth is achievable; for context, Paytm’s topline has grown at 90 percent YoY for each of the last three quarters. Within Paytm’s revenue mix, we estimate a rising share of high margin revenue streams such as financial services and devices, which we expect to aid profitability," said the brokerage.